ADT 2009 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2009 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

|

|

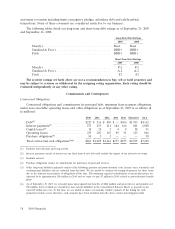

proves to be less than the recorded amounts, the reversal of the liabilities would result in tax benefits

being recognized in the period when we determine the liabilities are no longer necessary.

Goodwill and Indefinite-Lived Intangible Asset Impairments—Goodwill and indefinite-lived intangible

assets are assessed for impairment annually and more frequently if triggering events occur. In

performing these assessments, management relies on various factors, including operating results,

business plans, economic projections, anticipated future cash flows, comparable transactions and other

market data. There are inherent uncertainties related to these factors which require judgment in

applying them to the analysis of goodwill and indefinite-lived intangible assets for impairment. Since

judgment is involved in performing fair value measurements used in goodwill and indefinite-lived

intangible assets impairment analyses, there is risk that the carrying values of our goodwill or

indefinite-lived intangible assets may be overstated.

We elected to make the first day of the fourth quarter the annual impairment assessment date for

all goodwill and indefinite-lived intangible assets. In the first step of the goodwill impairment test, the

Company compares the fair value of a reporting unit with its carrying amount. Fair value for the

goodwill impairment test is determined utilizing a discounted cash flow analysis based on the

Company’s future budgets discounted using the market participants’ weighted-average cost of capital

and market indicators of terminal year cash flows. Other valuation methods are used to corroborate the

discounted cash flow method. If the carrying amount of a reporting unit exceeds its fair value, goodwill

is considered potentially impaired and further tests are performed to measure the amount of

impairment loss. In the second step of the goodwill impairment test, the Company compares the

implied fair value of reporting unit goodwill with the carrying amount of the reporting unit’s goodwill.

If the carrying amount of a reporting unit’s goodwill exceeds the implied fair value of that goodwill, an

impairment loss is recognized in an amount equal to the excess of the carrying amount of goodwill over

its implied fair value. The implied fair value of goodwill is determined in the same manner that the

amount of goodwill recognized in a business combination is determined. The Company allocates the

fair value of a reporting unit to all of the assets and liabilities of that unit, including intangible assets,

as if the reporting unit had been acquired in a business combination. Any excess of the fair value of a

reporting unit over the amounts assigned to its assets and liabilities represents the implied fair value of

goodwill.

Long-Lived Assets—Assets held and used by the Company, including property, plant and

equipment and amortizable intangible assets, are reviewed for impairment whenever events or changes

in business circumstances indicate that the carrying amount of the asset may not be fully recoverable.

Tyco performs undiscounted operating cash flow analyses to determine if impairment exists. For

purposes of recognition and measurement of an impairment for assets held for use, Tyco groups assets

and liabilities at the lowest level for which cash flows are separately identified. If an impairment is

determined to exist, any related impairment loss is calculated based on fair value. Impairments to

long-lived assets to be disposed of are recorded based upon the fair value less cost to sell of the

applicable assets. The calculation of the fair value of long-lived assets is based on assumptions

concerning the amount and timing of estimated future cash flows and assumed discount rates, reflecting

varying degrees of perceived risk. Since judgment is involved in determining the fair value and useful

lives of long-lived assets, there is a risk that the carrying value of our long-lived assets may be

overstated or understated.

Pension and Postretirement Benefits—Our pension expense and obligations are developed from

actuarial valuations. Two critical assumptions in determining pension expense and obligations are the

discount rate and expected long-term return on plan assets. We evaluate these assumptions at least

annually. Other assumptions reflect demographic factors such as retirement, mortality and turnover and

are evaluated periodically and updated to reflect our actual experience. Actual results may differ from

actuarial assumptions. The discount rate represents the market rate for high-quality fixed income

investments and is used to calculate the present value of the expected future cash flows for benefit

obligations under our pension plans. A decrease in the discount rate increases the present value of

2009 Financials 53