Vodafone 2016 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2016 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

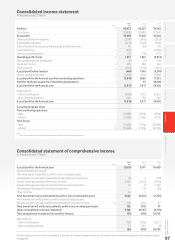

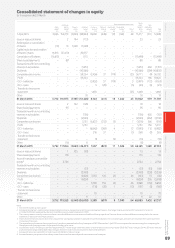

Overview Strategy review Performance Governance Financials Additional information

Vodafone Group Plc

Annual Report 2016

81

Area of focus How our audit addressed the area of focus

Carrying value of goodwill

Vodafone Group Plc has goodwill of £22,789 million

contained within 22 cash generating units (‘CGUs’).

Impairment charges to goodwill have been

recognised in prior periods. With challenging trading

conditions continuing in certain territories, the Group’s

performance and prospects could be impacted

increasing the risk that goodwill is impaired.

For the CGUs that contain goodwill, the determination

of recoverable amount, being the higher of fair value

less costs to sell and value-in-use, requires judgement

on the part of management in both identifying and

then valuing the relevant CGUs. Recoverable amounts

are based on management’s view of variables such as

future average revenue per user, average customer

numbers and customer churn, timing and approval of

future capital, spectrum and operating expenditure and

the most appropriate discount rate.

In the year ended 31 March 2016, a pre-tax impairment

charge of £450 million was recognised related to

goodwill in Romania.

Refer to the Audit and Risk Committee Report, note1

– Critical accounting judgements and key sources of

estimation uncertainty, note 4 – Impairment losses and

note 10 – Intangible assets.

We evaluated the appropriateness of management’s identication of the Group’s CGUs

and the continued satisfactory operation of the Group’s controls over the impairment

assessment process.

Our procedures included challenging management on the suitability of the impairment

model and reasonableness of the assumptions, with particular attention paid to the

European businesses, through performing the following:

a benchmarking Vodafone’s key market-related assumptions in management’s valuation

models with industry comparators and with assumptions made in the prior years

including revenue and margin trends, capital expenditure on network assets and

spectrum, market share and customer churn, foreign exchange rates and discount

rates, against external data where available, using our valuation expertise;

a testing the mathematical accuracy of the cash ow models and agreeing relevant data

to Board approved Long-Range Plans; and

a assessing the reliability of management’s forecast through a review of actual

performance against previous forecasts.

We validated the appropriateness of the related disclosures in note 4 and note 10 of the

nancial statements, including the sensitivities provided with respect to Germany, Spain,

and Romania.

Based on our procedures, we noted no exceptions and consider management’s key

assumptions to be within a reasonable range.

Provisions and contingent liabilities

There are a number of threatened and actual legal,

regulatory and tax cases against the Group. There is a

high level of judgement required in estimating the level

of provisioning required.

Refer to the Audit and Risk Committee Report, note1

– Critical accounting judgements and key sources

of estimation uncertainty, note 17 – Provisions and

note30 – Contingent liabilities and legal proceedings.

Our procedures included the following:

a testing key controls surrounding litigation, regulatory and tax procedures;

a where relevant, reading external legal opinions obtained by management;

a meeting with regional and local management and reading subsequent

Group correspondence;

a discussing open matters with the Group general counsel, Group litigation, regulatory,

general counsel and tax teams;

a assessing and challenging management’s conclusions through understanding

precedents set in similar cases; and

a circularising where appropriate relevant third party legal representatives and direct

discussion with them regarding certain material cases.

Based on the evidence obtained, while noting the inherent uncertainty with such legal,

regulatory and tax matters, we determined the level of provisioning at 31 March 2016

tobe appropriate and at a level consistent with previous periods.

We validated the completeness and appropriateness of the related disclosures through

assessing that the disclosure of the uncertainties in note 17 and note 30 of the nancial

statements was sufcient.