Vodafone 2016 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2016 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

Vodafone Group Plc

Annual Report 2016

134

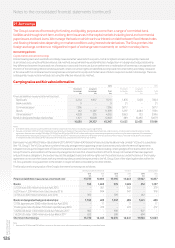

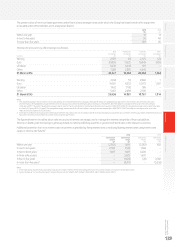

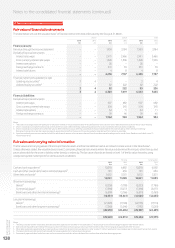

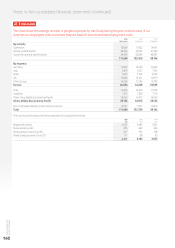

Notes to the consolidated nancial statements (continued)

23. Capital and nancial risk management

This note details our treasury management and nancial risk management objectives and policies, as well as

theexposure and sensitivity of the Group to credit, liquidity, interest and foreign exchange risk, and the policies

inplace to monitor and manage these risks.

Accounting policies

Financial instruments

Financial assets and nancial liabilities, in respect of nancial instruments, are recognised on the Group’s statement of nancial position when the

Group becomes a party to the contractual provisions of the instrument.

Financial liabilities and equity instruments

Financial liabilities and equity instruments issued by the Group are classied according to the substance of the contractual arrangements entered

into and the denitions of a nancial liability and an equity instrument. An equity instrument is any contract that provides a residual interest in the

assets of the Group after deducting all of its liabilities and includes no obligation to deliver cash or other nancial assets. The accounting policies

adopted for specic nancial liabilities and equity instruments are set out below.

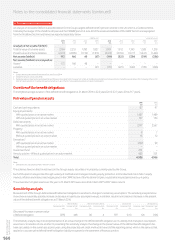

Put option arrangements over non-controlling interest

The potential cash payments related to put options issued by the Group over the equity of subsidiary companies are accounted for as nancial

liabilities when such options may only be settled by exchange of a xed amount of cash or another nancial asset for a xed number of shares

in the subsidiary.

The amount that may become payable under the option on exercise is initially recognised at present value within borrowings with a corresponding

charge directly to equity. The charge to equity is recognised separately as written put options over non-controlling interests, adjacent

to non-controlling interests in the net assets of consolidated subsidiaries. The Group recognises the cost of writing such put options, determined

as the excess of the present value of the option over any consideration received, as a nancing cost.

Such options are subsequently measured at amortised cost, using the effective interest rate method, in order to accrete the liability up to the

amount payable under the option at the date at which it rst becomes exercisable; the charge arising is recorded as a nancing cost. In the event that

the option expires unexercised, the liability is derecognised with a corresponding adjustment to equity.

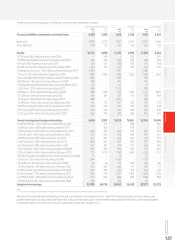

Derivative nancial instruments and hedge accounting

The Group’s activities expose it to the nancial risks of changes in foreign exchange rates and interest rates which it manages using derivative

nancial instruments.

The use of nancial derivatives is governed by the Group’s policies approved by the Board of Directors, which provide written principles on the use

of nancial derivatives consistent with the Group’s risk management strategy. Changes in values of all derivatives of a nancing nature are included

within investment income and nancing costs in the income statement unless designated in an effective cash ow hedge relationship or a hedge

of a net investment in foreign operations when changes in value are deferred to other comprehensive income or equity respectively. The Group

does not use derivative nancial instruments for speculative purposes.

Derivative nancial instruments are initially measured at fair value on the contract date and are subsequently remeasured to fair value at each

reporting date. The Group designates certain derivatives as:

a hedges of the change of fair value of recognised assets and liabilities (“fair value hedges”); or

a hedges of highly probable forecast transactions or hedges of foreign currency or interest rate risks of rm commitments (“cash ow hedges”); or

a hedges of net investments in foreign operations.

Hedge accounting is discontinued when the hedging instrument expires or is sold, terminated or exercised, or no longer qualies for hedge

accounting, or if the Company chooses to end the hedging relationship.

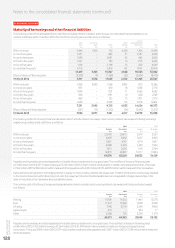

Fair value hedges

The Group’s policy is to use derivative instruments (primarily interest rate swaps) to convert a proportion of its xed rate debt to oating rates in order

to hedge the interest rate risk arising, principally, from capital market borrowings. The Group designates these as fair value hedges of interest rate risk

with changes in fair value of the hedging instrument recognised in the income statement for the period together with the changes in the fair value

of the hedged item arising from the hedged risk, to the extent the hedge is effective. Gains or losses relating to any ineffective portion are recognised

immediately in the income statement.

Cash ow hedges

Cash ow hedging is used by the Group to hedge certain exposures to variability in future cash ows. The portion of gains or losses relating

to changes in the fair value of derivatives that are designated and qualify as effective cash ow hedges is recognised in other comprehensive income;

gains or losses relating to any ineffective portion are recognised immediately in the income statement.

When the hedged item is recognised in the income statement, amounts previously recognised in other comprehensive income and accumulated

in equity for the hedging instrument are reclassied to the income statement. However, when the hedged transaction results in the recognition

of a non-nancial asset or a non-nancial liability, the gains and losses previously recognised in other comprehensive income and accumulated

in equity are transferred from equity and included in the initial measurement of the cost of the non-nancial asset or non-nancial liability.

When hedge accounting is discontinued, any gain or loss recognised in other comprehensive income at that time remains in equity and

is recognised in the income statement when the hedged transaction is ultimately recognised in the income statement. If a forecast transaction

is no longer expected to occur, the gain or loss accumulated in equity is recognised immediately in the income statement.