Vodafone 2016 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2016 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

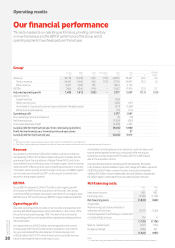

Italy

Service revenue declined 0.8%* for the year, but returned to growth

in Q4 (Q3: -0.3%*; Q4: 1.3%*), aided by the leap-year benet. The mobile

business is on a steady recovery path, while xed line performance

continues to be positive despite increased competition in recent months.

Mobile service revenue declined 1.1%*, as a recovery in ARPU supported

by prepaid price increases only partially offset the year-on-year decline

in the customer base. Mobile number portability in the market has

reduced in recent quarters and the customer base decline stabilised

during the year, aided by market-leading NPS scores in mobile following

our Project Spring investments. Consumer trends improved faster

than Enterprise, where competitive intensity has increased in H2.

As of 31 March 2016 we have 95% population coverage on our 4G

network and 6.5 million 4G customers (September 2015: 4.0 million).

Fixed service revenue was up 1.2%*, driven by sustained commercial

momentum. We added 168,000 broadband customers during the

year, a strong performance, and in Q4 50% of our gross adds have

taken a bre-based service. Of our base of 2.0 million broadband

customers, 297,000 are bre customers. We have now built out our

own bre network to over 16,000 cabinets, enabling us to reach

3.6 million households. Our high speed broadband rollout in Italy will

be enhanced by our commercial agreement with Enel, which plans

to roll out Fibre-To-The-Home (FTTH) to 224 cities nationwide, providing

access on competitive commercial terms. In these areas Enel will be our

exclusive bre partner going forward.

EBITDA was up 3.1%*, as we successfully offset the decline in service

revenue with savings in commercial costs and operating expenses.

The EBITDA margin was stable year-on-year due principally to higher

handset revenues.

UK

Service revenue declined 0.3%* for the year (Q3: -0.7%*; Q4: -0.1%*),

with improving trends in xed line offset by a slowdown in mobile,

reecting operational challenges following a billing system migration.

Q4 growth beneted from strong carrier services activity; excluding

this, underlying trends were stable. The organic growth rate for the year

excludes one-off settlements with other network operators in Q2.

Mobile service revenue declined 0.7%*. Contract customer growth

slowed in Q4, impacted partly by higher churn in relation to the

billing system migration. Revenue trends were also impacted by the

pricing and usage of 08XX numbers following the introduction

of Non-Geographic Call Services regulation, and a focus on giving

customers more control of their out-of-bundle data spend. As a result,

in-bundle revenue and demand for data add-ons continued to grow.

Enterprise mobile trends remained relatively stable despite increased

competition. National 4G coverage reached 91% (based on the OFCOM

denition), and 99.5% in London; based on our estimations, 4G coverage

was 84%, and despite some delays the pace of 4G coverage expansion

in conjunction with our network sharing partner is now accelerating.

We achieved signicant growth in 4G customers, with 7.0 million at the

period end (September 2015: 5.3 million).

Fixed service revenue grew 1.1%*. Excluding carrier services, xed

service revenue grew 2.4%* in the second half of the year including

an improving performance in Enterprise. After regional trials during

the summer, we began to offer our consumer broadband service

to 24 million premises across the UK (98% of BT’s bre footprint)

in October, securing 38,000 customers by 31 March 2016. Our new

TV service is in eld trials with plans to launch later in the current

calendar year.

EBITDA grew 1.2%*, with a 0.2* percentage point increase in the EBITDA

margin driven by continued operational efciencies. Reported EBITDA

beneted from one-off settlements with other network operators in the

rst half of the year.

Spain

Service revenue declined 3.5%* (Q3: -3.1%*; Q4: -3.2%*), with

mobile revenue recovering steadily despite the negative effect

of handset nancing, and continued positive momentum in xed.

Excluding handset nancing effects, service revenues declined

by0.3%* in the year.

Mobile service revenue fell 8.0%*. The contract customer base

continued to grow in a more stable market, despite increased

promotional activity around the start of the new football season. We are

seeing signs that ARPU is beginning to stabilise, aided by our market-

leading NPS scores in mobile and our ‘more-for-more’ pricing strategy,

in which customers receive higher data allowances and additional

features (e.g. free European roaming) together with an increase in the

monthly tariff. Our 4G population coverage reached 91% at 31 March

2016 and we have 5.4 million 4G customers.

Fixed service revenue rose 7.8%*, supported by consistent growth

in broadband net additions. The integration of Ono has proceeded

successfully and we have already achieved 100% of the original

€240 million of cost and capex synergies targeted. We now expect

to be able to deliver €300 million of annualised run-rate savings over the

original timeframe. In part this reects the very successful launch in May

of Vodafone One, our fully integrated cable, mobile and TV service,

which has already reached 1.5 million customers. Including our joint

bre network build with Orange, we now reach 8.5 million premises

with cable or bre. Our recent agreement with Mediapro together with

the wholesale obligations imposed on the incumbent provide us with

access to a full range of premium TV channels for the coming years,

albeit at an increased cost.

EBITDA increased 4.2%* year-on-year with a 1.3* percentage point

increase in the EBITDA margin, as strong cost control, the benet

to margin from handset nancing and the cost synergies from the Ono

acquisition more than offset rising TV costs.

Other Europe

Service revenue rose 1.5%* (Q3: 1.6%*; Q4: 2.1%*), with all markets

except Greece achieving growth during the year. In Q4, Romania (7.7%*),

Portugal (3.5%*) and the Czech Republic enjoyed an improvement

in top-line growth.

Overview Strategy review Performance Governance Financials Additional information

Vodafone Group Plc

Annual Report 2016

33