Vodafone 2011 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2011 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

Vodafone Group Plc Annual Report 2011 41

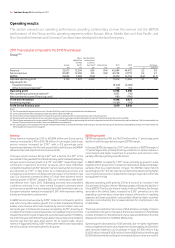

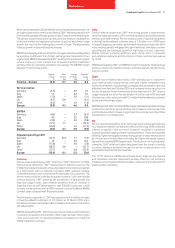

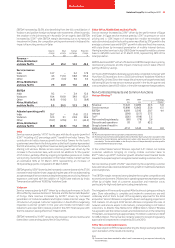

Performance

Italy

Service revenue growth was 1.9%(*) with strong growth in data revenue,

driven by higher penetration of PC connectivity devices and mobile internet

services, and fixed revenue. The continued success of dual branding led to

a closing fixed broadband customer base of 1.3 million on a 100% basis.

Increased regulatory, economic and competitive pressures led to the fall in

voice revenue partially mitigated through initiatives to stimulate customer

spending and the continued growth in high value contract customers.

Mobile contract customer additions were strong both in consumer

and enterprise segments and the closing contract customer base was up

by 14.5%.

EBITDA increased by 4.3%(*) and EBITDA margin increased by 1.0 percentage

point as a result of increased revenue, continued operational efficiencies

and cost control.

Spain

Full year service revenue declined by 7.0%(*) primarily due to a decline in

voice revenue which was driven by continued intense competition and

economic weakness, including high unemployment, termination rate cuts

effective from April and October 2009 and increased involuntary churn. In

the fourth quarter the service revenue decline improved to 6.2%(*) as voice

usage increased due to further penetration of our flat rate tariffs and fixed

line revenue continued to grow with 0.6 million fixed broadband customers

by the end of the financial year.

EBITDA declined 9.9%(*) and the EBITDA margin decreased by 0.8 percentage

points as the decline in service revenue, the increase in commercial costs

and the dilutive effect of lower margin fixed line services more than offset

the reduction in overhead costs.

UK

Service revenue declined by 4.7%(*) with lower voice revenue primarily due

to a mobile termination rate reduction effective from July 2009, continued

intense competition and economic pressures resulting in customers

optimising bundle usage and lower roaming revenue. These were partially

offset by higher messaging revenue, strong growth in data revenue driven

by the success of mobile internet bundles and higher wholesale revenue

derived from existing MVNO agreements. The decline in the fourth quarter

slowed to 2.6%(*) driven by higher data growth and the impact of mobile

customer additions achieved through the launch of new products and

expanded indirect distribution channels.

The 17.7%(*) decline in EBITDA was primarily due to lower service revenue

and increased customer investment partially offset by cost efficiency

initiatives, including streamlined processes, outsourcing and reductions in

publicity and consultancy.

Revenue increased by 0.2% benefiting from exchange rate movements. On

an organic basis service revenue declined by 3.8%(*) reflecting reductions in

most markets partially offset by growth in Italy, Turkey and the Netherlands.

The decline was primarily driven by reduced voice revenue resulting from

continued market and regulatory pressure on pricing and slower usage

growth as a result of the challenging economic climate. This was partially

offset by growth in data and fixed line revenue.

EBITDA decreased by 3.9% resulting from an organic decline partially offset

by a positive contribution from foreign exchange rate movements. On an

organic basis, EBITDA decreased by 8.9%(*) resulting from a decline in organic

service revenue in most markets and increased customer investment

partially offset by operating and direct cost savings. The EBITDA margin

declined 1.5 percentage points.

Organic M&A Foreign Reported

change activity exchange change

% pps pps %

Revenue – Europe (4.5) 0.1 4.6 0.2

Service revenue

Germany (3.5) – 6.0 2.5

Italy 1.9 – 6.2 8.1

Spain (7.0) – 5.9 (1.1)

UK (4.7) 0.6 – (4.1)

Other (6.0) – 4.4 (1.6)

Europe (3.8) 0.1 4.6 0.9

EBITDA

Germany (8.9) – 5.7 (3.2)

Italy 4.3 – 6.5 10.8

Spain (9.9) – 6.1 (3.8)

UK (17.7) 1.1 – (16.6)

Other (16.0) – 4.4 (11.6)

Europe (8.9) 0.1 4.9 (3.9)

Adjusted operating profit

Germany (13.2) (0.1) 5.7 (7.6)

Italy 7.8 – 6.8 14.6

Spain (13.8) – 6.0 (7.8)

UK (58.3) 5.6 – (52.7)

Other (27.7) – 4.8 (22.9)

Europe (12.6) 0.1 5.5 (7.0)

Germany

Service revenue declined by 3.5%(*) driven by a 5.0%(*) reduction in mobile

revenue partly offset by a 1.3%(*) improvement in fixed line revenue. The

mobile revenue decline was driven by a decrease in voice revenue impacted

by a termination rate cut effective from April 2009, reduced roaming,

competitive pressure and continued tariff optimisation by customers. The

service revenue decline in the fourth quarter slowed to 1.6%(*) with mobile

revenue declining 1.8%(*) driven by the acceleration in data growth and

improved usage trends. Data revenue benefited from an increase in

Superflat Internet tariff penetration to over 500,000 customers, a 46%

increase in smartphones and an 85% increase in active Vodafone Mobile

Connect cards compared with the previous year.

Fixed line revenue growth of 1.3%(*) was supported by a 0.4 million increase

in fixed broadband customers to 3.5 million at 31 March 2010 and a

0.2 million increase in wholesale fixed broadband customers to 0.4 million

at 31 March 2010.

EBITDA declined by 8.9%(*) driven by lower service revenue and investment

in customer acquisition and retention offset in part by lower interconnect

costs and a reduction of operating expenses principally from fixed and

mobile integration synergies.