The Hartford 2011 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

97

Reinsurance for Terrorism

For the risk of terrorism, private sector catastrophe reinsurance capacity is generally limited and largely unavailable for terrorism losses

caused by nuclear, biological, chemical or radiological weapons attacks. As such, the Company’ s principal reinsurance protection

against large-scale terrorist attacks is the coverage currently provided through the TRIPRA. On December 26, 2007, the President

signed TRIPRA extending the Terrorism Risk Insurance Act of 2002 (“TRIA”) through the end of 2014. TRIPRA provides a backstop

for insurance-related losses resulting from any “act of terrorism” certified by the Secretary of the Treasury, in concurrence with the

Secretary of State and Attorney General, that result in industry losses in excess of $100. In addition, TRIPRA revised the TRIA

definition of a certified “act of terrorism” by removing the requirement that an act be committed “on behalf of any foreign person or

foreign interest”. As a result, domestic acts of terrorism can now be certified as “acts of terrorism” under the program, subject to the

other requirements of TRIPRA. Under the program, in any one calendar year, the federal government would pay 85% of covered losses

from a certified act of terrorism after an insurer’ s losses exceed 20% of the Company’ s eligible direct commercial earned premiums of

the prior calendar year, up to a combined annual aggregate limit for the federal government and all insurers of $100 billion. If an act of

terrorism or acts of terrorism result in covered losses exceeding the $100 billion annual industry aggregate limit, a future Congress

would be responsible for determining how additional losses in excess of $100 billion will be paid.

Among other items, TRIPRA required that the President’ s Working Group on Financial Markets (“PWG”) continue to perform an

analysis regarding the long-term availability and affordability of insurance for terrorism risk. Among the findings detailed in the

PWG’ s initial report, released October 2, 2006, were that the high level of uncertainty associated with predicting the frequency of

terrorist attacks, coupled with the unwillingness of some insurance policyholders to purchase insurance coverage, makes predicting

long-term development of the terrorism risk market difficult, and that there is likely little potential for future market development for

NBCR coverage. The January 2011 PWG report notes some improvements in capacity and modeling, but also noted that take-up rates

for terrorism coverage remained relatively flat over the past three years and that insurers remain uncertain about the ability of models to

predict the frequency and severity of terrorist attacks. With respect to NBCR coverage, a December 2008 study by the U.S.

Government Accountability Office (“GAO”) found that property and casualty insurers still generally seek to exclude NBCR coverage

from their commercial policies when permitted. However, while nuclear, pollution and contamination exclusions are contained in many

property and liability insurance policies, the GAO report concluded that such exclusions may be subject to challenges in court because

they were not specifically drafted to address terrorist attacks. Furthermore, workers’ compensation policies generally have no exclusion

or limitations. The GAO found that commercial property and casualty policyholders, including companies that own high-value

properties in large cities, generally reported that they could not obtain NBCR coverage. Commercial property and casualty insurers

generally remain unwilling to offer NBCR coverage because of uncertainties about the risk and the potential for catastrophic losses.

Reinsurance Recoverables

Reinsurance Security

To manage reinsurer credit risk, a security review committee evaluates the credit standing, financial performance, management and

operational quality of each potential reinsurer. Through this process, the Company maintains a centralized list of reinsurers approved

for participation in reinsurance transactions. Only reinsurers approved through this process are eligible to participate in new reinsurance

transactions. The Company’ s approval designations reflect the differing credit exposure associated with various classes of business.

Participation eligibility is categorized based upon the nature of the risk reinsured, including the expected liability payout duration. In

addition to defining participation eligibility, the Company regularly monitors credit risk exposure to each reinsurance counterparty and

has established limits tiered by counterparty credit rating. For further discussions on how the Company manages and mitigates third

party credit risk, refer to the Credit Risk section.

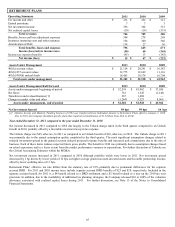

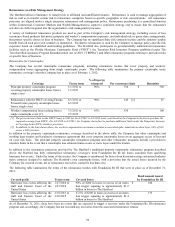

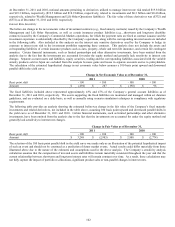

Property and Casualty Insurance Product Reinsurance Recoverable

Property and casualty insurance product reinsurance recoverables represent loss and loss adjustment expense recoverable from a number

of entities, including reinsurers and pools. The following table shows the components of the gross and net reinsurance recoverable as of

December 31, 2011 and 2010:

Reinsurance Recoverable

December 31, 2011

December 31, 2010

Paid loss and loss adjustment expenses

$

153

$

198

Unpaid loss and loss adjustment expenses

2,884

2,963

Gross reinsurance recoverable

3,037

3,161

Less: allowance for uncollectible reinsurance

(290)

(290)

Net reinsurance recoverable

$

2,747

$

2,871