The Hartford 2011 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

111

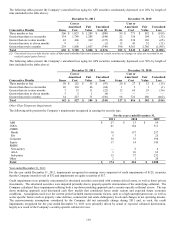

Derivative Instruments

The Company utilizes a variety of over-the-counter and exchange traded derivative instruments as a part of its overall risk management

strategy, as well as to enter into replication transactions. Derivative instruments are used to manage risk associated with interest rate,

equity market, credit spread, issuer default, price, and currency exchange rate risk or volatility. Replication transactions are used as an

economical means to synthetically replicate the characteristics and performance of assets that would otherwise be permissible

investments under the Company’ s investment policies. For further information on the Company’ s use of derivatives, see Note 5 of the

Notes to Consolidated Financial Statements.

Derivative activities are monitored and evaluated by the Company’ s compliance and risk management teams and reviewed by senior

management. In addition, the Company monitors counterparty credit exposure on a monthly basis to ensure compliance with Company

policies and statutory limitations. The notional amounts of derivative contracts represent the basis upon which pay or receive amounts

are calculated and are not reflective of credit risk. Downgrades to the credit ratings of The Hartford’ s insurance operating companies

may have adverse implications for its use of derivatives including those used to hedge benefit guarantees of variable annuities. In some

cases, downgrades may give derivative counterparties the unilateral contractual right to cancel and settle outstanding derivative trades or

require additional collateral to be posted. In addition, downgrades may result in counterparties becoming unwilling to engage in

additional over-the-counter (“OTC”) derivatives or may require collateralization before entering into any new trades. This will restrict

the supply of derivative instruments commonly used to hedge variable annuity guarantees, particularly long-dated equity derivatives and

interest rate swaps. Under these circumstances, the Company’ s operating subsidiaries could conduct hedging activity using a

combination of cash and exchange-traded instruments, in addition to using the available OTC derivatives.

The Company uses various derivative counterparties in executing its derivative transactions. The use of counterparties creates credit

risk that the counterparty may not perform in accordance with the terms of the derivative transaction. The Company has developed a

derivative counterparty exposure policy which limits the Company’ s exposure to credit risk. The derivative counterparty exposure

policy establishes market-based credit limits, favors long-term financial stability and creditworthiness of the counterparty and typically

requires credit enhancement/credit risk reducing agreements. The Company minimizes the credit risk of derivative instruments by

entering into transactions with high quality counterparties primarily rated A or better, which are monitored and evaluated by the

Company’ s risk management team and reviewed by senior management. In addition, the Company monitors counterparty credit

exposure on a monthly basis to ensure compliance with Company policies and statutory limitations. The Company also generally

requires that derivative contracts, other than exchange traded contracts, certain forward contracts, and certain embedded and reinsurance

derivatives, be governed by an International Swaps and Derivatives Association Master Agreement, which is structured by legal entity

and by counterparty and permits right of offset.

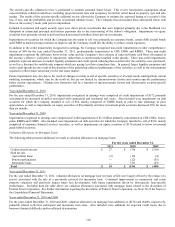

The Company has developed credit exposure thresholds which are based upon counterparty ratings. Credit exposures are measured

using the market value of the derivatives, resulting in amounts owed to the Company by its counterparties or potential payment

obligations from the Company to its counterparties. Credit exposures are generally quantified daily based on the prior business day’ s

market value and collateral is pledged to and held by, or on behalf of, the Company to the extent the current value of the derivatives

exceed the contractual thresholds. In accordance with industry standard and the contractual agreements, collateral is typically settled on

the next business day. The Company has exposure to credit risk for amounts below the exposure thresholds which are uncollateralized,

as well as for market fluctuations that may occur between contractual settlement periods of collateral movements.

For the company’ s domestic derivative programs, the maximum uncollateralized threshold for a derivative counterparty for a single

legal entity is $10. The Company currently transacts OTC derivatives in five legal entities that have a threshold greater than zero and

therefore the maximum combined threshold for a single counterparty across all legal entities that use derivatives is $50. In addition, the

Company may have exposure to multiple counterparties in a single corporate family due to a common credit support provider. As of

December 31, 2011, for the company’ s domestic derivative programs, the maximum combined threshold for all counterparties under a

single credit support provider across all legal entities that use derivatives is $100. Based on the contractual terms of the collateral

agreements, these thresholds may be immediately reduced due to a downgrade in either party’ s credit rating. Beginning in the fourth

quarter of 2011, the Company began hedging its Japan exposures within the legal entity HLIKK. The counterparty credit exposures at

HLIKK generally follow the maximum uncollateralized threshold of the domestic program; however, for two counterparties,

collateralization requirements are currently not in place. These two counterparties maintain credit ratings of A or better, and the

Company actively monitors their credit standing. For further discussion, see the Derivative Commitments section of Note 12 of the

Notes to Consolidated Financial Statements.

For the year ended December 31, 2011, the Company has incurred no losses on derivative instruments due to counterparty default.

In addition to counterparty credit risk, the Company may also introduce credit risk through the use of credit default swaps that are

entered into to manage credit exposure. Credit default swaps involve a transfer of credit risk of one or many referenced entities from

one party to another in exchange for periodic payments. The party that purchases credit protection will make periodic payments based

on an agreed upon rate and notional amount, and for certain transactions there will also be an upfront premium payment. The second

party, who assumes credit risk, will typically only make a payment if there is a credit event as defined in the contract and such payment

will be typically equal to the notional value of the swap contract less the value of the referenced security issuer’ s debt obligation. A

credit event is generally defined as default on contractually obligated interest or principal payments or bankruptcy of the referenced

entity.