The Hartford 2011 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

123

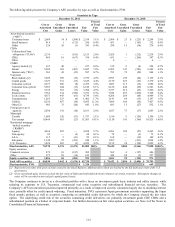

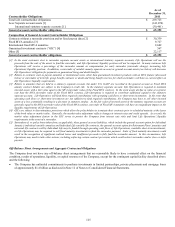

Commercial Paper and Revolving Credit Facility

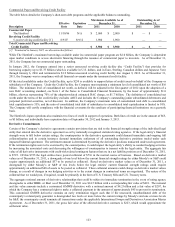

The table below details the Company’ s short-term debt programs and the applicable balances outstanding.

Maximum Available As of

Outstanding As of

Effective

Expiration

December 31,

December 31,

Description

Date

Date

2011

2010

2011

2010

Commercial Paper

The Hartford

11/10/86

N/A

$

2,000

$

2,000

$

—

$

—

Revolving Credit Facility

5-year revolving credit facility [1]

8/9/07

8/9/12

1,900

1,900

—

—

Total Commercial Paper and Revolving

Credit Facility

$

3,900

$

3,900

$

—

$

—

[1] Terminated in January 2012, see discussion that follows.

While The Hartford’ s maximum borrowings available under its commercial paper program are $2.0 billion, the Company is dependent

upon market conditions to access short-term financing through the issuance of commercial paper to investors. As of December 31,

2011, the Company has no commercial paper outstanding.

In January 2012, the Company entered into a senior unsecured revolving credit facility (the “Credit Facility”) that provides for

borrowing capacity up to $1.75 billion (which is available in U.S. dollars, and in Euro, Sterling, Canadian dollars and Japanese Yen)

through January 6, 2016 and terminated its $1.9 billion unsecured revolving credit facility due August 9, 2012. As of December 31,

2011, the Company was in compliance with all financial covenants under the terminated credit facility.

Of the total availability under the Credit Facility, up to $250 is available to support letters of credit issued on behalf of the Company or

subsidiaries of the Company. Under the Credit Facility, the Company must maintain a minimum level of consolidated net worth of $16

billion. The minimum level of consolidated net worth, as defined, will be adjusted in the first quarter of 2012 upon the adoption of a

new DAC accounting standard, see Note 1 of the Notes to Consolidated Financial Statements, by the lesser of approximately $1.0

billion, after-tax representing 70% of the adoption-related estimated DAC charge, or $1.7 billion. The definition of consolidated net

worth under the terms of the credit facility excludes AOCI and includes the Company’ s outstanding junior subordinated debentures and

perpetual preferred securities, net of discount. In addition, the Company’ s maximum ratio of consolidated total debt to consolidated

total capitalization is 35%, and the ratio of consolidated total debt of subsidiaries to consolidated total capitalization is limited to 10%.

The Company will certify compliance with the financial covenants for the syndicate of participating financial institutions on a quarterly

basis.

The Hartford’ s Japan operations also maintain two lines of credit in support of operations. Both lines of credit are in the amount of $65,

or ¥5 billion, and individually have expiration dates of September 30, 2012 and January 3, 2013.

Derivative Commitments

Certain of the Company’ s derivative agreements contain provisions that are tied to the financial strength ratings of the individual legal

entity that entered into the derivative agreement as set by nationally recognized statistical rating agencies. If the legal entity’ s financial

strength were to fall below certain ratings, the counterparties to the derivative agreements could demand immediate and ongoing full

collateralization and in certain instances demand immediate settlement of all outstanding derivative positions traded under each

impacted bilateral agreement. The settlement amount is determined by netting the derivative positions transacted under each agreement.

If the termination rights were to be exercised by the counterparties, it could impact the legal entity’ s ability to conduct hedging activities

by increasing the associated costs and decreasing the willingness of counterparties to transact with the legal entity. The aggregate fair

value of all derivative instruments with credit-risk-related contingent features that are in a net liability position as of December 31, 2011,

is $725. Of this $725 the legal entities have posted collateral of $716 in the normal course of business. Based on derivative market

values as of December 31, 2011, a downgrade of one level below the current financial strength ratings by either Moody’ s or S&P could

require approximately an additional $37 to be posted as collateral. Based on derivative market values as of December 31, 2011, a

downgrade by either Moody’ s or S&P of two levels below the legal entities’ current financial strength ratings could require

approximately an additional $48 of assets to be posted as collateral. These collateral amounts could change as derivative market values

change, as a result of changes in our hedging activities or to the extent changes in contractual terms are negotiated. The nature of the

collateral that we would post, if required, would be primarily in the form of U.S. Treasury bills and U.S. Treasury notes.

The aggregate notional amount of derivative relationships that could be subject to immediate termination in the event of rating agency

downgrades to either BBB+ or Baa1 as of December 31, 2011 was $14.5 billion with a corresponding fair value of $418. The notional

and fair value amounts include a customized GMWB derivative with a notional amount of $4.2 billion and a fair value of $207, for

which the Company has a contractual right to make a collateral payment in the amount of approximately $45 to prevent its termination.

This customized GMWB derivative contains an early termination trigger such that if the unsecured, unsubordinated debt of the

counterparty’ s related party guarantor is downgraded two levels or more below the current ratings by Moody’ s and one or more levels

by S&P, the counterparty could terminate all transactions under the applicable International Swaps and Derivatives Association Master

Agreement. As of December 31, 2011, the gross fair value of the affected derivative contracts is $223, which would approximate the

settlement value.