The Hartford 2011 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

81

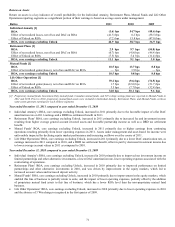

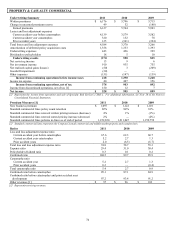

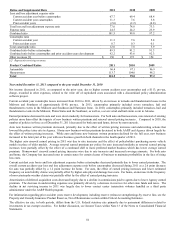

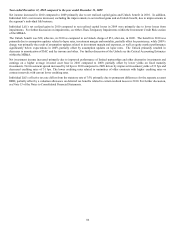

Ratios and Supplemental Data

2011

2010

2009

Loss and loss adjustment expense ratio

Current accident year before catastrophes

67.7

69.4

68.4

Current accident year catastrophes

11.3

7.6

5.8

Prior accident years

(2.0)

(2.2)

(0.8)

Total loss and loss adjustment expense ratio

77.0

74.8

73.3

Expense ratio

24.5

24.2

23.9

Combined ratio

101.5

99.0

97.2

Catastrophe ratio

Current accident year

11.3

7.6

5.8

Prior accident years

0.7

0.3

0.1

Total catastrophe ratio

12.0

7.8

5.9

Combined ratio before catastrophes

89.5

91.2

91.3

Combined ratio before catastrophes and prior accident years development

92.2

93.6

92.3

Other revenues [1]

$

156

$

172

$

154

[1] Represents servicing revenues.

Product Combined Ratios

2011

2010

2009

Automobile

96.4

97.1

96.9

Homeowners

113.7

104.0

98.2

Total

101.5

99.0

97.2

Year ended December 31, 2011 compared to the year ended December 31, 2010

Net income decreased in 2011, as compared to the prior year, due to higher current accident year catastrophes and a $113, pre-tax,

charge, recorded in other expenses, related to the write off of capitalized costs associated with a discontinued policy administration

software project.

Current accident year catastrophe losses increased from 2010 to 2011, driven by an increase in tornado and thunderstorm losses in the

Midwest and Southeast of approximately $140, pre-tax. In 2011, catastrophes primarily included severe tornadoes, hail and

thunderstorm events in the Midwest and Southeast and Hurricane Irene. In 2010, catastrophes primarily included tornadoes, hail and

thunderstorm events in the Midwest, Plains States and the Southeast, as well as, a severe wind and hail storm event in Arizona.

Earned premiums decreased in auto and were down modestly for homeowners. For both auto and homeowners, non-renewal of existing

policies more than offset the impacts of new business written premium and renewal earned pricing increases. Compared to 2010, the

number of policies in-force as of December 31, 2011 decreased for both auto and home, driven by non-renewals.

Auto new business written premium decreased, primarily due to the effect of written pricing increases and underwriting actions that

lowered the policy issue rate in Agency. Home new business written premium decreased in both AARP and Agency driven largely by

the effect of written pricing increases. While auto and home new business written premium declined for the full year, new business

increased in the latter part of the year with new business growth in both channels in the fourth quarter of 2011.

The higher auto renewal earned pricing in 2011 was due to rate increases and the effect of policyholders purchasing newer vehicle

models in place of older models. Average renewal earned premium per policy for auto increased modestly as renewal earned pricing

increases were partially offset by the effect of a continued shift to more preferred market business which has lower average earned

premium. Homeowners’ renewal earned pricing increases were due to rate increases and increased coverage amounts. For both auto

and home, the Company has increased rates in certain states for certain classes of business to maintain profitability in the face of rising

loss costs.

Current accident year losses and loss adjustment expenses before catastrophes decreased primarily due to lower earned premiums. The

overall current accident year loss and loss adjustment expense ratio before catastrophes decreased during 2011 as a 2.6 point decrease

for auto was partially offset by a 1.2 point increase for home. For auto, the effect of earned pricing increases and lower estimated

frequency on auto liability claims was partially offset by higher auto physical damage loss costs. For home, an increase in the frequency

of non-catastrophe weather claims was partially offset by the effect of earned pricing increases.

Amortization of deferred acquisition costs decreased largely due to a decline in commissions paid to agents due to lower Agency earned

premium. The decrease in underwriting expenses was primarily driven by a decrease in reserves for other state funds and taxes. The

decline in net servicing income in 2011 was largely due to lower contact center transaction volumes handled as a third party

administrator under the AARP Health program.

For information regarding prior accident years reserve development, including reserve (releases) strengthenings by reserve line, see the

Property and Casualty Insurance Product Reserves, Net of Reinsurance section within Critical Accounting Estimates.

The effective tax rate, in both periods, differs from the U.S. Federal statutory rate primarily due to permanent differences related to

investments in tax exempt securities. For further discussion, see Income Taxes within Note 13 of the Notes to Consolidated Financial

Statements.