The Hartford 2011 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

122

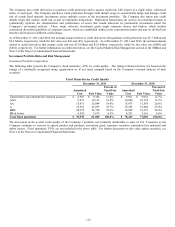

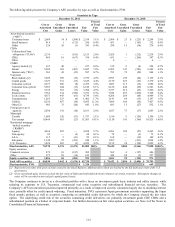

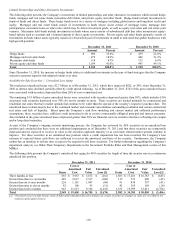

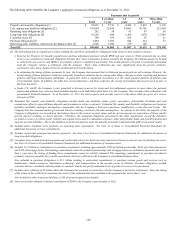

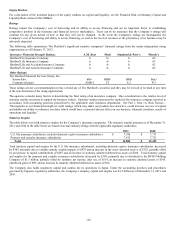

Dividends from Insurance Subsidiaries

Dividends to the HFSG Holding Company from its insurance subsidiaries are restricted. The payment of dividends by Connecticut-

domiciled insurers is limited under the insurance holding company laws of Connecticut. These laws require notice to and approval by

the state insurance commissioner for the declaration or payment of any dividend, which, together with other dividends or distributions

made within the preceding twelve months, exceeds the greater of (i) 10% of the insurer’ s policyholder surplus as of December 31 of the

preceding year or (ii) net income (or net gain from operations, if such company is a life insurance company) for the twelve-month period

ending on the thirty-first day of December last preceding, in each case determined under statutory insurance accounting principles. In

addition, if any dividend of a Connecticut-domiciled insurer exceeds the insurer’ s earned surplus, it requires the prior approval of the

Connecticut Insurance Commissioner. The insurance holding company laws of the other jurisdictions in which The Hartford’ s

insurance subsidiaries are incorporated (or deemed commercially domiciled) generally contain similar (although in certain instances

somewhat more restrictive) limitations on the payment of dividends. Dividends paid to HFSG Holding Company by its life insurance

subsidiaries are further dependent on cash requirements of HLI and other factors. The Company’ s property-casualty insurance

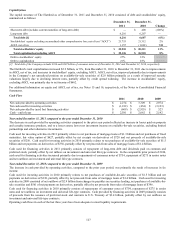

subsidiaries are permitted to pay up to a maximum of approximately $1.4 billion in dividends to HFSG Holding Company in 2012

without prior approval from the applicable insurance commissioner. The Company’ s life insurance subsidiaries are permitted to pay up

to a maximum of approximately $625 in dividends to HLI in 2012 without prior approval from the applicable insurance commissioner.

The aggregate of these amounts is the maximum the insurance subsidiaries could pay to HFSG Holding Company in 2012 without prior

approval from the applicable insurance commissioner. In addition to statutory limitations on paying dividends, the Company also takes

other items into consideration when determining dividends from subsidiaries. These considerations include, but are not limited to

expected earnings and capitalization of the subsidiary, regulatory capital requirements and liquidity requirements of the individual

operating company. In 2012, HFSG Holding Company anticipates receiving $800 in dividends from its property-casualty insurance

subsidiaries, net of dividends to fund interest payments on an intercompany note between Hartford Holdings, Inc. and Hartford Fire

Insurance Company, and no dividends from the life insurance subsidiaries. In 2011, HFSG Holding Company and HLI received $80 in

dividends from the life insurance subsidiaries, and HFSG Holding Company received $1.1 billion in dividends from its property-

casualty insurance subsidiaries, including $150 reflecting the net realized capital gain on the sale of SRS, $160 related to funding

interest payments on an intercompany note between Hartford Holdings Inc. and Hartford Fire Insurance Company and $800 used in

conjunction with other resources at the HFSG Holding Company principally to fund dividends, interest, capital contributions to

subsidiaries and debt maturities.

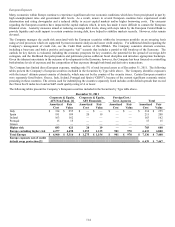

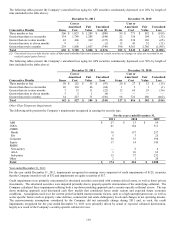

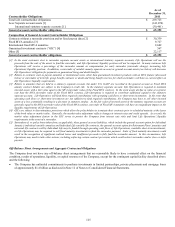

Other Sources of Capital for the HFSG Holding Company

The Hartford endeavors to maintain a capital structure that provides financial and operational flexibility to its insurance subsidiaries,

ratings that support its competitive position in the financial services marketplace (see the “Ratings” section below for further

discussion), and shareholder returns. As a result, the Company may from time to time raise capital from the issuance of equity, equity-

related debt or other capital securities and is continuously evaluating strategic opportunities. The issuance of common equity, equity-

related debt or other capital securities could result in the dilution of shareholder interests or reduced net income due to additional interest

expense.

Shelf Registrations

On August 4, 2010, The Hartford filed with the Securities and Exchange Commission (the “SEC”) an automatic shelf registration

statement (Registration No. 333-168532) for the potential offering and sale of debt and equity securities. The registration statement

allows for the following types of securities to be offered: debt securities, junior subordinated debt securities, preferred stock, common

stock, depositary shares, warrants, stock purchase contracts, and stock purchase units. In that The Hartford is a well-known seasoned

issuer, as defined in Rule 405 under the Securities Act of 1933, the registration statement went effective immediately upon filing and

The Hartford may offer and sell an unlimited amount of securities under the registration statement during the three-year life of the

registration statement.

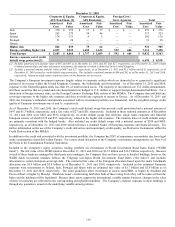

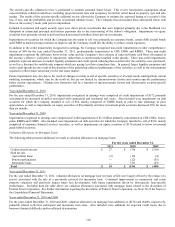

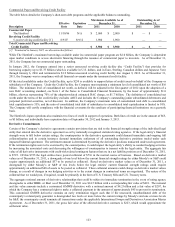

Contingent Capital Facility

The Hartford is party to a put option agreement that provides The Hartford with the right to require the Glen Meadow ABC Trust, a

Delaware statutory trust, at any time and from time to time, to purchase The Hartford’ s junior subordinated notes in a maximum

aggregate principal amount not to exceed $500. Under the Put Option Agreement, The Hartford will pay the Glen Meadow ABC Trust

premiums on a periodic basis, calculated with respect to the aggregate principal amount of Notes that The Hartford had the right to put

to the Glen Meadow ABC Trust for such period. The Hartford has agreed to reimburse the Glen Meadow ABC Trust for certain fees

and ordinary expenses. The Company holds a variable interest in the Glen Meadow ABC Trust where the Company is not the primary

beneficiary. As a result, the Company did not consolidate the Glen Meadow ABC Trust. As of December 31, 2011, The Hartford has

not exercised its right to require Glen Meadow ABC Trust to purchase the Notes. As a result, the Notes remain a source of capital for

the HFSG Holding Company.