The Hartford 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

128

Equity Markets

For a discussion of the potential impact of the equity markets on capital and liquidity, see the Financial Risk on Statutory Capital and

Liquidity Risk section in this MD&A.

Ratings

Ratings impact the Company’ s cost of borrowing and its ability to access financing and are an important factor in establishing

competitive position in the insurance and financial services marketplace. There can be no assurance that the Company’ s ratings will

continue for any given period of time or that they will not be changed. In the event the Company's ratings are downgraded, the

Company’ s cost of borrowing and ability to access financing, as well as the level of revenues or the persistency of its business may be

adversely impacted.

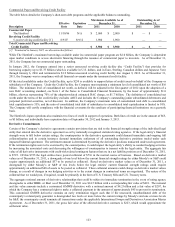

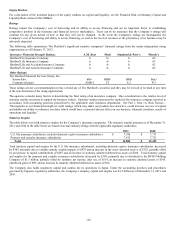

The following table summarizes The Hartford’ s significant member companies’ financial ratings from the major independent rating

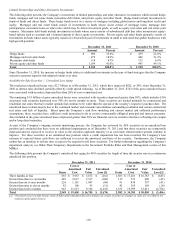

organizations as of February 17, 2012.

Insurance Financial Strength Ratings:

A.M. Best

Fitch

Standard & Poor’s

Moody’s

Hartford Fire Insurance Company

A

A+

A

A2

Hartford Life Insurance Company

A

A-

A

A3

Hartford Life and Accident Insurance Company

A

A-

A

A3

Hartford Life and Annuity Insurance Company

A

A-

A

A3

Other Ratings:

The Hartford Financial Services Group, Inc.:

Senior debt

Commercial paper

bbb+

AMB-2

BBB-

F2

BBB

A-2

Baa3

P-3

These ratings are not a recommendation to buy or hold any of The Hartford’ s securities and they may be revised or revoked at any time

at the sole discretion of the rating organization.

The agencies consider many factors in determining the final rating of an insurance company. One consideration is the relative level of

statutory surplus necessary to support the business written. Statutory surplus represents the capital of the insurance company reported in

accordance with accounting practices prescribed by the applicable state insurance department. See Part I, Item 1A. Risk Factors –

“Downgrades in our financial strength or credit ratings, which may make our products less attractive, could increase our cost of capital

and inhibit our ability to refinance our debt, which would have a material adverse effect on our business, financial condition, results of

operations and liquidity.”

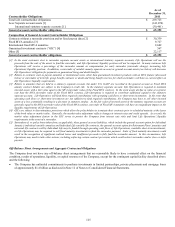

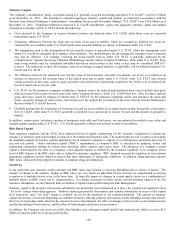

Statutory Surplus

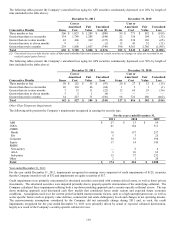

The table below sets forth statutory surplus for the Company’ s insurance companies. The statutory surplus amounts as of December 31,

2011 and 2010 in the table below are based on actual statutory filings with the applicable regulatory authorities.

2011

2010

U.S. life insurance subsidiaries, includes domestic captive insurance subsidiaries

$

7,388

$

7,731

Property and casualty insurance subsidiaries

7,412

7,721

Total

$

14,800

$

15,452

Total statutory capital and surplus for the U.S. life insurance subsidiaries, including domestic captive insurance subsidiaries, decreased

by $343, primarily due to variable annuity surplus impacts of $470 and an increase in the asset valuation reserve of $323, partially offset

by an increase in capital contributions of $287 and an increase in statutory admitted deferred tax assets of $268. Total statutory capital

and surplus for the property and casualty insurance subsidiaries decreased by $309, primarily due to dividends to the HFSG Holding

Company of $1.1 billion, partially offset by statutory net income, after tax, of $514, an increase in statutory admitted assets of $145,

unrealized gains of $90, and an increase in statutory admitted deferred tax assets of $26.

The Company also holds regulatory capital and surplus for its operations in Japan. Under the accounting practices and procedures

governed by Japanese regulatory authorities, the Company’ s statutory capital and surplus was $1.3 billion as of December 31, 2011 and

2010.