Starwood 2012 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2012 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

|

|

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

NOTES TO FINANCIAL STATEMENTS

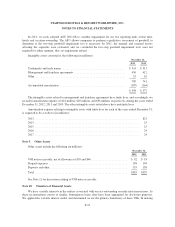

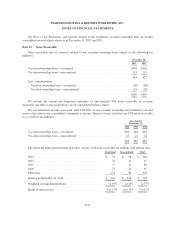

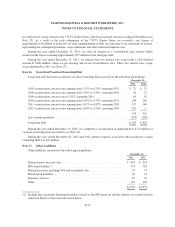

For the vacation ownership and residential segment, we record an estimate of expected uncollectibility on

our VOI notes receivable as a reduction of revenue at the time we recognize profit on a timeshare sale. We hold

large amounts of homogeneous VOI notes receivable and therefore, assess uncollectibility based on pools of

receivables. In estimating loss reserves, we use a technique referred to as static pool analysis, which tracks

uncollectible notes for each year’s sales over the life of the respective notes and projects an estimated default rate

that is used in the determination of our loan loss reserve requirements. As of December 31, 2012, the average

estimated default rate for our pools of receivables was 9.7%.

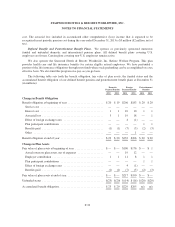

The activity and balances for our loan loss reserve are as follows (in millions):

Securitized Unsecuritized Total

Balance at December 31, 2009 ............................ $— $94 $ 94

Provisions for loan losses .............................. 14 32 46

Write-offs .......................................... — (52) (52)

Adoption of ASU No. 2009-17 .......................... 77 (4) 73

Other .............................................. (9) 9 —

Balance at December 31, 2010 ............................ 82 79 161

Provisions for loan losses .............................. 2 27 29

Write-offs .......................................... — (54) (54)

Other .............................................. (4) 4 —

Balance at December 31, 2011 ............................ 80 56 136

Provisions for loan losses .............................. — 26 26

Write-offs .......................................... — (41) (41)

Other .............................................. (7) 7 —

Balance at December 31, 2012 ............................ $73 $48 $121

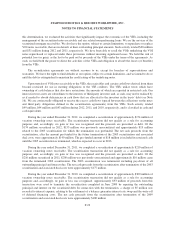

We use the origination of the notes by brand (Sheraton, Westin, and Other) as the primary credit quality

indicator to calculate the loan loss reserve for the vacation ownership notes, as we believe there is a relationship

between the default behavior of borrowers and the brand associated with the vacation ownership property they

have acquired. In addition to quantitatively calculating the loan loss reserve based on our static pool analysis, we

supplement the process by evaluating certain qualitative data, including the aging of the respective receivables,

current default trends by brand and origination year, and the FICO scores of the buyers.

Given the significance of our pools of VOI notes receivable, a change in the projected default rate can have

a significant impact to our loan loss reserve requirements, with a 0.1% change estimated to have an impact of

approximately $4 million.

We consider a VOI note receivable delinquent when it is more than 30 days outstanding. All delinquent

loans are placed on nonaccrual status, and we do not resume interest accrual until payment is made. We consider

loans to be in default upon reaching 120 days outstanding, at which point, we generally commence the

repossession process. Uncollectible VOI notes receivable are charged off when title to the unit is returned to us.

We generally do not modify vacation ownership notes that become delinquent or upon default.

F-24