Starwood 2012 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2012 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

|

|

STARWOOD HOTELS & RESORTS WORLDWIDE, INC.

NOTES TO FINANCIAL STATEMENTS

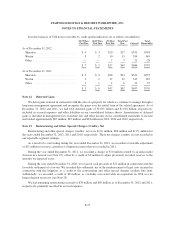

this determination, we evaluated the activities that significantly impact the economics of the VIEs, including the

management of the securitized notes receivable and any related non-performing loans. We are the servicer of the

securitized mortgage receivables. We also have the option, subject to certain limitations, to repurchase or replace

VOI notes receivable, that are in default, at their outstanding principal amounts. Such activity totaled $28 million

and $31 million during 2012 and 2011, respectively. We have been able to resell the VOIs underlying the VOI

notes repurchased or replaced under these provisions without incurring significant losses. We hold the risk of

potential loss (or gain), as the last to be paid out by proceeds of the VIEs under the terms of the agreements. As

such, we hold both the power to direct the activities of the VIEs and obligation to absorb the losses (or benefits)

from the VIEs.

The securitization agreements are without recourse to us, except for breaches of representations and

warranties. We have the right to fund defaults at our option, subject to certain limitations, and we intend to do so

until the debt is extinguished to maintain the credit rating of the underlying notes.

Upon transfer of VOI notes receivable to the VIEs, the receivables and certain cash flows derived from them

become restricted for use in meeting obligations to the VIE creditors. The VIEs utilize trusts which have

ownership of cash balances that also have restrictions, the amounts of which are reported in restricted cash. Our

interest in trust assets are subordinate to the interests of third-party investors and, as such, may not be realized by

us if needed to absorb deficiencies in cash flows that are allocated to the investors in the trusts’ debt (see Note

16). We are contractually obligated to receive the excess cash flows (spread between the collections on the notes

and third party obligations defined in the securitization agreements) from the VIEs. Such activity totaled

$49 million, $44 million and $43 million during 2012, 2011, and 2010, respectively, and is classified in cash and

cash equivalents.

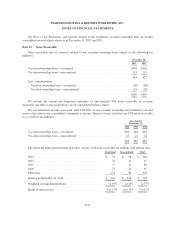

During the year ended December 31, 2012, we completed a securitization of approximately $174 million of

vacation ownership notes receivable. The securitization transaction did not qualify as a sale for accounting

purposes and, accordingly, no gain or loss was recognized and the proceeds are presented as debt. Of the

$174 million securitized in 2012, $155 million was previously unsecuritized and approximately $19 million

related to the 2005 securitization for which the termination was prefunded. The net cash proceeds from the

securitization, after the amount pre-funded for the future termination of the 2005 securitization and associated

deal costs, were approximately $140 million. The pre-funded amount of $18 million is included in restricted cash

until the 2005 securitization is terminated, which is expected to occur in 2013.

During the year ended December 31, 2011, we completed a securitization of approximately $210 million of

vacation ownership notes receivable. The securitization transaction did not qualify as a sale for accounting

purposes and, accordingly, no gain or loss was recognized and the proceeds are presented as debt. Of the

$210 million securitized in 2011, $200 million was previously unsecuritized and approximately $10 million came

from the terminated 2003 securitization. The 2003 securitization was terminated, including pay-down of all

outstanding principal and interest due. The net cash proceeds from the securitization after termination of the 2003

securitization and associated deal costs were approximately $177 million.

During the year ended December 31, 2010, we completed a securitization of approximately $300 million of

vacation ownership notes receivable. The securitization transaction did not qualify as a sale for accounting

purposes and, accordingly, no gain or loss was recognized. Approximately $93 million of proceeds from this

transaction were used to terminate the securitization completed in June 2009 by repaying the outstanding

principal and interest on the securitized debt. In connection with the termination, a charge of $5 million was

recorded to interest expense, relating to the settlement of a balance guarantee interest rate swap and the write-off

of deferred financing costs. The net cash proceeds from the securitization after termination of the 2009

securitization and associated deal costs were approximately $180 million

F-22