PNC Bank 2001 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2001 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

78

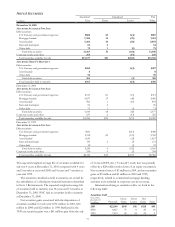

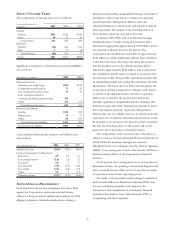

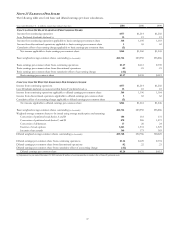

NOTE 14 SECURITIZATIONS

During 2001, the Corporation sold residential mortgage

loans, commercial mortgage loans and other loans totaling

$1.0 billion, $374 million, and $82 million, respectively, in

secondary market securitization transactions. These

securitization transactions resulted in pretax gains of $9.6

million, $1 million, and $2 million, respectively, for the year

ended December 31, 2001.

In addition to the sale of loans discussed above, in March

2001 PNC securitized $3.8 billion of residential mortgage

loans by selling the loans into a trust with PNC retaining

99% or $3.7 billion of the certificates. PNC also securitized

$175 million of commercial mortgage loans by selling the

loans into a trust with PNC retaining 99% or $173 million of

the certificates. In each case, the 1% interest in the trust was

purchased by a publicly-traded entity managed by a

subsidiary of PNC. A substantial portion of the entity’s

purchase price was financed by PNC. The reclassification of

these loans to securities increased the liquidity of the assets

and was consistent with PNC’s on-going balance sheet

restructuring. At the time of the residential mortgage

securitization, gains of $25.9 million were deferred and are

being recognized when principal payments are received or

the securities are sold to third parties. At December 31, 2001,

these securities had been reduced to $1.3 billion through

sales and principal payments and the remaining deferred

gains were $7.8 million. No gain was recognized at the time

of the commercial mortgage loan securitization and none of

the securities retained at the time of the securitization

remained on the balance sheet at December 31, 2001.

In addition to the securities discussed above, the

Corporation retained certain interest-only strips and servicing

rights that were created in the sale of certain loans.

Additional information on these items is contained below.

Key economic assumptions used in measuring the fair

value of the interest-only strips and servicing rights at the

date of the securitization resulting from securitizations

completed during the year and related information were as

follows:

Key Economic Assumptions

Dollars in millions

Fair

Value

Weighted-

average Life

(Years)

Prepayment

Speed

(CPR)(a)

Discount

Rate

During 2001

Residential

mortgage $38 1.2 – 1.7 36.0% 10.00%

Commercial

mortgage 5 9.4 10.0 10.00

Other 21.9 4.14

During 2000

Commercial

mortgage $7 9.6 10.0% 10.00%

(a) Constant Prepayment Rate (“CPR”).

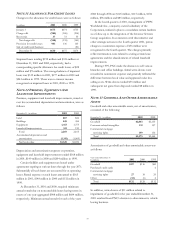

Quantitative information about managed securitized loan

portfolios in which the Corporation had interest-only strips

outstanding at December 31, 2001 and related delinquencies

follows:

Interest-Only Strips

Managed Delinquencies

December 31 - in millions 2001 2000 2001 2000

Residential loans $1,058 $178 $24 $2

Student loans 453 573 49 66

Total managed loans $1,511 $751 $73 $68

Certain cash flows received from and paid to securitization

trusts in which the Corporation had interest-only strips

outstanding during the period follows:

Securitization Cash Flows

Year ended December 31 – in millions 2001 2000

Proceeds from new securitizations $1,040 $877

Servicing revenue 87

Other cash flows received on retained

interests 16 22

Proceeds from new securitizations are limited to cash

proceeds received from third parties. It excludes the value of

securities generated as a result of the recharacterization of

loans to securities. During 2001 and 2000, there were no

purchases of delinquent or foreclosed assets, and servicing

advances and repayments of servicing advances were not

significant.

Changes in the Corporation’s commercial mortgage

servicing assets are as follows:

Commercial Mortgage Servicing Activity

In millions 2001 2000

Balance at January 1 $156 $125

Additions 70 49

Amortization (27) (18)

Balance at December 31 $199 $156

Assuming a prepayment speed of 10% and weighted average

life of 10.8 years discounted at 10%, the estimated fair value

of commercial mortgage servicing rights was $240 million at

December 31, 2001. A 10% and 20% adverse change in all

assumptions used to determine fair value at December 31,

2001, results in a $22 million and $44 million decrease in fair

value, respectively. No valuation allowance was necessary for

the years ended December 31, 2001 and December 31, 2000.