PNC Bank 2001 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2001 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

44

STRATEGIC REPOSITIONING

The Corporation took several actions in 2001 to accelerate

the strategic repositioning of its lending business that began

in 1998. These actions entail a degree of risk pending

completion.

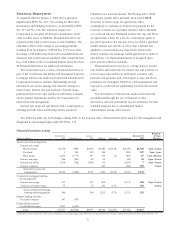

At December 31, 2001, $5.0 billion of institutional

lending credit exposure including $2.6 billion of outstandings

were classified as held for sale. A total of $169 million of

these loans was included in nonperforming assets at that

date. The loans are carried at the lower of cost or estimated

fair market value. The estimation of fair market values

involves a number of judgments, and is inherently uncertain.

In addition, the value of loan assets is affected by a variety of

company, industry, economic and other factors, and can be

volatile. If the value of loans held for sale deteriorates prior

to disposition, valuation adjustments will be made through

charges to earnings. Moreover, deterioration in the condition

of the borrowers could lead to additional loans being placed

on nonperforming status. See Critical Accounting Policies

and Judgments for additional information.

During the fourth quarter of 2001, the Corporation

decided to discontinue its vehicle leasing business and

recorded charges of $135 million related to exit costs and

additions to reserves related to insured residual value

exposures. At December 31, 2001, approximately $1.9 billion

of vehicle leases remained on the Corporation’s books.

These leases are expected to mature over a period of

approximately five years. During this period, the Corporation

will continue to be subject to risks inherent in the vehicle

leasing business, including credit risk and the risk that

vehicles returned during or at the conclusion of the lease

term cannot be disposed of at a price at least as great as the

Corporation’s remaining investment in the vehicles after

application of any available residual value insurance or

related reserves.

In January 2001, PNC sold its residential mortgage

banking business. Certain closing date purchase price

adjustments aggregating approximately $300 million pretax

are currently in dispute between the parties. The Corporation

has established a receivable of approximately $140 million to

reflect additional purchase price it believes is due from the

buyer. The buyer has taken the position that the purchase

price it has already paid should be reduced by approximately

$160 million. The Corporation has established specific

reserves related to a portion of its recorded receivable. The

purchase agreement requires that an independent public

accounting firm determine the final adjustments. The buyer

also has filed a lawsuit against the Corporation seeking

compensatory damages with respect to certain of the

disputed matters that the Corporation believes are covered

by the process provided in the purchase agreement,

unquantified punitive damages and declaratory and other

relief. Management intends to assert the Corporation’s

positions vigorously. Management believes that, net of

available reserves, an adverse outcome, expected to be

recorded in discontinued operations, could be material to net

income in the period in which recorded, but that the final

disposition of this matter will not be material to the

Corporation’s financial position.

CRITICAL ACCOUNTING POLICIES AND

JUDGMENTS

The Corporation’s consolidated financial statements are

prepared based on the application of certain accounting

policies, the most significant of which are described in

Note 1 Accounting Policies. Certain of these policies require

numerous estimates and strategic or economic assumptions

that may prove inaccurate or subject to variations and may

significantly affect PNC’s reported results and financial

position for the period or in future periods. Changes in

underlying factors, assumptions, or estimates in any of these

areas could have a material impact on PNC’s future financial

condition and results of operations.

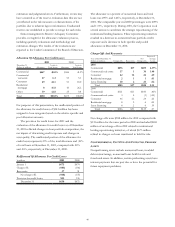

Allowance For Credit Losses

The allowance for credit losses is calculated with the

objective of maintaining a reserve level believed by

management to be sufficient to absorb estimated probable

credit losses. Management’s determination of the adequacy

of the allowance is based on periodic evaluations of the

credit portfolio and other relevant factors. However, this

evaluation is inherently subjective as it requires material

estimates, including, among others, expected default

probabilities, loss given default, expected commitment usage,

the amounts and timing of expected future cash flows on

impaired loans, value of collateral, estimated losses on

consumer loans and residential mortgages, and general

amounts for historical loss experience. The process also

considers economic conditions, uncertainties in estimating

losses and inherent risks in the various credit portfolios. All

of these factors may be susceptible to significant change.

Also, the allocation of the allowance to specific loan pools is

based on historical loss trends and management’s judgment

concerning those trends. Commercial loans are the largest

category of credits and are the most sensitive to changes in

assumptions and judgments underlying the determination of

the allowance. As such, approximately $467 million or 74%

of the total allowance at December 31, 2001 has been

allocated to the commercial loan category. This allocation

also considers other relevant factors such as actual versus

estimated losses, regional and national economic conditions,

business segment and portfolio concentrations, industry

competition and consolidation, the impact of government

regulations, and risk of potential estimation or judgmental

errors. To the extent actual outcomes differ from

management estimates, additional provision for credit losses

may be required that would adversely impact earnings in

future periods.