Nokia 2009 Annual Report Download - page 183

Download and view the complete annual report

Please find page 183 of the 2009 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

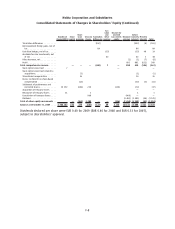

|

|

Notes to the Consolidated Financial Statements

1. Accounting principles

Basis of presentation

The consolidated financial statements of Nokia Corporation (“Nokia” or “the Group”), a Finnish public

limited liability company with domicile in Helsinki, in the Republic of Finland, are prepared in

accordance with International Financial Reporting Standards as issued by the International Accounting

Standards Board (“IASB”) and in conformity with IFRS as adopted by the European Union (“IFRS”). The

consolidated financial statements are presented in millions of euros (“EURm”), except as noted, and

are prepared under the historical cost convention, except as disclosed in the accounting policies

below. The notes to the consolidated financial statements also conform to Finnish Accounting

legislation. On March 11, 2010, Nokia’s Board of Directors authorized the financial statements for

2009 for issuance and filing.

The Group completed the acquisition of all of the outstanding equity of NAVTEQ on July 10, 2008 and

a transaction to form Nokia Siemens Networks on April 1, 2007. The NAVTEQ and the Nokia Siemens

Networks business combinations have had a material impact on the consolidated financial statements

and associated notes. See Note 8.

Adoption of pronouncements under IFRS

In the current year, the Group has adopted all of the new and revised standards, amendments and

interpretations to existing standards issued by the IASB that are relevant to its operations and

effective for accounting periods commencing on or after January 1, 2009.

• IAS 1 (Revised), Presentation of financial statements, prompts entities to aggregate

information in the financial statements on the basis of shared characteristics. All nonowner

changes in equity (i.e. comprehensive income) should be presented either in one statement of

comprehensive income or in a separate income statement and statement of comprehensive

income.

• Amendments to IFRS 7 require entities to provide additional disclosures about the fair value

measurements. The amendments clarify the existing requirements for the disclosure of

liquidity risk.

• Amendment to IFRS 2, Sharebased payment, Group and Treasury Share Transactions, clarifies

the definition of different vesting conditions, treatment of all nonvesting conditions and

provides further guidance on the accounting treatment of cancellations by parties other than

the entity.

• Amendment to IAS 20, Accounting for government grants and disclosure of government

assistance, requires that the benefit of a belowmarket rate government loan is measured as

the difference between the carrying amount in accordance with IAS 39 and the proceeds

received, with the benefit accounted for in accordance with IAS 20.

• Amendment to IAS 23, Borrowing costs, changes the treatment of borrowing costs that are

directly attributable to an acquisition, construction or production of a qualifying asset. These

costs will consequently form part of the cost of that asset. Other borrowing costs are

recognized as an expense.

• Under the amended IAS 32 Financial Instruments: Presentation, the Group must classify

puttable financial instruments or instruments or components thereof that impose an obligation

to deliver to another party, a prorata share of net assets of the entity only on liquidation, as

equity. Previously, these instruments would have been classified as financial liabilities.

• Amendments to IFRIC 9 and IAS 39 clarify the accounting treatment of embedded derivatives

when reclassifying financial instruments.

F9