Nokia 2009 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2009 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

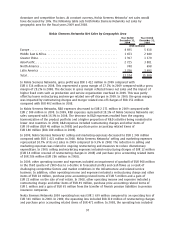

the following discussion are based on our definition of the industry mobile device market used in

2008 and 2007.

Year Ended

December 31,

2008

Change (%)

2007 to 2008

Year Ended

December 31,

2007

(Units in millions, except percentage data)

Europe .......................................... 281 (1)% 284

Middle East & Africa ................................ 149 18% 126

Greater China ..................................... 183 6% 173

AsiaPacific. . ..................................... 284 12% 254

North America .................................... 178 4% 170

Latin America..................................... 139 7% 130

Total ............................................ 1213 7% 1137

According to our estimates, in 2008 industry mobile device volumes grew by 7% to 1.21 billion units,

compared with an estimated 1.14 billion units in 2007. This growth was driven primarily by the

strong growth in both replacement sales and sales from new subscribers in emerging markets,

particularly Middle East & Africa and AsiaPacific. Developed market device volumes were driven

primarily by replacement sales. We estimated that Europe market volumes were down in 2008.

We estimated that emerging markets accounted for approximately 63% of industry device volumes in

2008, compared with approximately 59% in 2007. The entrylevel device market (devices priced at 50

euro or under) continued to be one of the fastest growing segments for the market. This was

particularly the case in 2008 where we estimated this part of the market represented approximately

44% of the total industry volumes and grew almost 30% in volumes compared to 2007. We

estimated the converged device (smartphones) market was approximately 161 million units globally

in 2008, growing strongly from approximately 117 million units in 2007.

Despite this overall yearonyear growth, the mobile device market deteriorated significantly in the

second half of 2008, with a pronounced weakening in the fourth quarter of 2008. The negative

impact of the rapidly deteriorating global economic conditions, including weaker consumer and

corporate spending, severely constrained credit availability and unprecedented currency market

volatility, was apparent in varying degrees across all geographic markets and product ranges.

At the end of 2008, we estimated that there were approximately 3.9 billion mobile subscriptions

globally, representing approximately 58% global penetration. This is compared to approximately

3.3 billion mobile subscribers in 2007 and approximately 43% penetration.

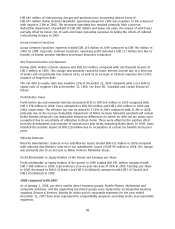

The following table sets forth our mobile device volumes and yearonyear growth rate by geographic

area for the fiscal years 2008 and 2007. The estimates of Nokia’s volume market share in the

following discussion are based on our definition of the industry mobile device market used in 2008

and 2007.

Year Ended

December 31,

2008

Change (%)

2007 to 2008

Year Ended

December 31,

2007

(Units in millions, except percentage data)

Europe .......................................... 114.9 (2.0)% 117.2

Middle East & Africa ................................ 81.0 7.1% 75.6

Greater China ..................................... 71.3 0.8% 70.7

AsiaPacific. . ..................................... 134.0 18.7% 112.9

North America .................................... 15.7 (19.1)% 19.4

Latin America..................................... 51.5 24.7% 41.3

Total ............................................ 468.4 7.2% 437.1

101