Nokia 2003 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2003 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

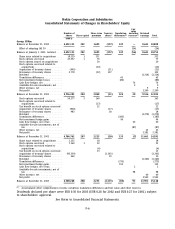

|

|

Notes to the Consolidated Financial Statements (Continued)

1. Accounting principles (Continued)

changes are calculated using a weighted average purchase price method. An impairment is

recorded when the carrying amount of an available for sale investment is greater than the

estimated fair value and there is objective evidence that the asset is impaired. The cumulative net

loss relating to that investment is removed from equity and recognized in the profit and loss

account for the period. If, in a subsequent period, the fair value of the investment increases and

the increase can be objectively related to an event occurring after the loss was recognized, the loss

is reversed, with the amount of the reversal included in the profit and loss account.

The fair values of other financial assets and financial liabilities are assumed to approximate their

carrying values, either because of their short maturities, or where their fair values cannot be

measured reliably.

Derivatives

Fair values of forward rate agreements, interest rate options and futures contracts are calculated

based on quoted market rates at the balance sheet date. Interest rate and currency swaps are

valued by using discounted cash flow analyses. The changes in the fair values of these contracts

are reported in the profit and loss account.

Fair values of cash settled equity derivatives are calculated by revaluing the contract at year-end

quoted market rates. Changes in the fair value are reported in the profit and loss account.

Forward foreign exchange contracts are valued with the forward exchange rate. Changes in fair

value are calculated by comparing this with the original amount calculated by using the contract

forward rate prevailing at the beginning of the contract. Currency options are valued at the

balance sheet date by using the Garman & Kohlhagen option valuation model. Changes in the fair

value on these instruments are reported in the profit and loss account except to the extent they

qualify for hedge accounting.

Embedded derivatives are identified and monitored in the Group and fair valued at the balance

sheet date. In assessing the fair value of embedded derivatives the Group uses a variety of

methods, such as option pricing models and discounted cash flow analysis, and makes

assumptions that are based on market conditions existing at each balance sheet date. The fair

value changes are reported in the profit and loss account.

Hedge accounting

Hedging of anticipated foreign currency denominated sales and purchases

The Group applies hedge accounting for ‘‘Qualifying hedges’’. Qualifying hedges are those properly

documented cash flow hedges of the foreign exchange rate risk of future anticipated foreign

currency denominated sales and purchases that meet the requirements set out in IAS 39. The cash

flow being hedged must be ‘‘highly probable’’ and must ultimately impact the profit and loss

account. The hedge must be highly effective both prospectively and retrospectively.

The Group claims hedge accounting in respect of certain forward foreign exchange contracts and

options, or option strategies, which have zero net premium or a net premium paid, and where the

critical terms of the bought and sold options within a collar or zero premium structure are the

same and where the nominal amount of the sold option component is no greater than that of the

bought option.

F-9