IBM 2003 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2003 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

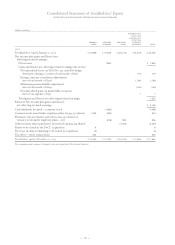

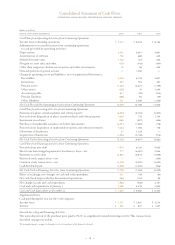

Services

The terms of services contracts generally range from less

than one year to ten years. Revenue from time and material

services contracts is recognized as the services are provided.

Revenue from data center or Business Transformation

Outsourcing (BTO) contracts in which IBM manages a client’s

data center or operates a client’s specific business process,

respectively, reflects the extent of actual services delivered in

the period, based upon objective measures of output in

accordance with the terms of the contract.

Revenue from Business Consulting Services (BCS) con-

tracts that require IBM to design, develop, manufacture or

modify complex information technology (IT) systems to a

buyer’s specifications, and to provide services related to the

performance of such contracts, is recognized using the

percentage of completion (POC) method of accounting. In

using the POC method, the company records revenue by

reference to the costs incurred to date and the estimated

costs remaining to fulfill the contracts.

Provisions for losses on services contracts are recognized

during the period in which the loss first becomes apparent.

Revenue from maintenance is recognized over the contrac-

tual period or as the services are performed.

In some of the company’s services contracts, the company

bills the client prior to performing the services. This situation

gives rise to deferred income of $3.3 billion and $2.6 billion at

December 31, 2003 and 2002, respectively, and is reported as

Deferred income in the Consolidated Statement of Financial

Position. In other services contracts, the company performs

the services prior to billing the client. This situation gives rise

to unbilled accounts receivable of $1.8 billion and $1.3 billion

at December 31, 2003 and 2002, respectively, and is recorded

as Notes and accounts receivable-trade in the Consolidated

Statement of Financial Position. In these circumstances,

billings usually occur shortly after the company performs the

services and can range up to six months later. Unbilled receiv-

ables are expected to be billed and collected generally within

four months, rarely exceeding nine months. The largest

driver of the increase in unbilled accounts receivable is the

favorable impacts from currency translation.

Hardware

Revenue from hardware sales or sales-type leases is recognized

when the product is shipped to the client and when there are

no unfulfilled company obligations that affect the client’s final

acceptance of the arrangement. Any cost of these obligations

is accrued when the corresponding revenue is recognized.

Revenue from rentals and operating leases is recognized on a

straight-line basis over the term of the rental or lease.

Software

Revenue from one-time charge licensed software is recognized

at the inception of the license term. Revenue from monthly

license charge arrangements is recognized on a subscription

basis over the period that the client is using the program.

Revenue from maintenance, unspecified upgrades and tech-

nical support is recognized over the period such items are

delivered. For multiple-element arrangement software con-

racts and multiple-element arrangement software contracts

that include non-software elements whereby the software is

essential to the functionality of the non-software elements

(collectively referred to as software multiple-element

arrangements), the company applies the following rules:

Asoftware multiple-element arrangement is separated

into more than one unit of accounting if all of the following

criteria are met:

•The functionality of the delivered element(s) is not

dependent on the undelivered element(s).

•There is vendor-specific objective evidence (VSOE) of fair

value of the undelivered element(s).

•Delivery of the delivered element(s) represents the culmi-

nation of the earnings process for those element(s).

If these criteria are not met, the revenue is deferred until

such criteria are met or until the period(s) over which the

last undelivered element is delivered. If there is VSOE for all

units of accounting in an arrangement, the arrangement con-

sideration is allocated to the separate units of accounting

based on each unit’s relative VSOE. There may be cases,

however, in which there is VSOE of the undelivered item(s)

but no such evidence for the delivered item(s). In these cases,

the residual method is used to allocate the arrangement

consideration. Under the residual method, the amount of

consideration allocated to the delivered item(s) equals the

total arrangement consideration less the aggregate VSOE of

the undelivered elements.

Financing

Finance income attributable to sales-type leases, direct

financing leases and loans is recognized at level rates of

return over the term of the leases or loans. Operating lease

income is recognized on a straight-line basis over the term of

the lease.

EXPENSE AND OTHER INCOME

Selling, General and Administrative

Selling, general and administrative (SG&A) expense is

charged to income as incurred. Expenses of promoting and

selling products and services are classified as selling expense

and include such items as advertising, sales commissions and

travel. General and administrative expense includes such

items as officers’ salaries, office supplies, non-income taxes,

insurance and office rental. In addition, general and adminis-

trative expense includes other operating items such as a

provision for doubtful accounts, workforce accruals for

contractually obligated payments to employees terminated

in the ongoing course of business, amortization of intangible

assets and environmental remediation costs. Certain special

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION AND SUBSIDIARY COMPANIES

81