Cisco 2012 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2012 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

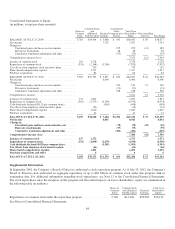

|

|

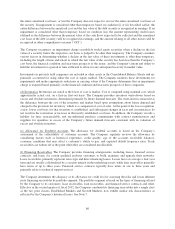

the entire amortized cost basis, or (iii) the Company does not expect to recover the entire amortized cost basis of

the security. If impairment is considered other than temporary based on condition (i) or (ii) described earlier, the

entire difference between the amortized cost and the fair value of the debt security is recognized in earnings. If an

impairment is considered other than temporary based on condition (iii), the amount representing credit losses

(defined as the difference between the present value of the cash flows expected to be collected and the amortized

cost basis of the debt security) will be recognized in earnings, and the amount relating to all other factors will be

recognized in other comprehensive income (“OCI”).

The Company recognizes an impairment charge on publicly traded equity securities when a decline in the fair

value of a security below the respective cost basis is judged to be other than temporary. The Company considers

various factors in determining whether a decline in the fair value of these investments is other than temporary,

including the length of time and extent to which the fair value of the security has been less than the Company’s

cost basis, the financial condition and near-term prospects of the issuer, and the Company’s intent and ability to

hold the investment for a period of time sufficient to allow for any anticipated recovery in market value.

Investments in privately held companies are included in other assets in the Consolidated Balance Sheets and are

primarily accounted for using either the cost or equity method. The Company monitors these investments for

impairments and makes appropriate reductions in carrying values if the Company determines that an impairment

charge is required based primarily on the financial condition and near-term prospects of these companies.

(d) Inventories Inventories are stated at the lower of cost or market. Cost is computed using standard cost, which

approximates actual cost, on a first-in, first-out basis. The Company provides inventory write-downs based on

excess and obsolete inventories determined primarily by future demand forecasts. The write-down is measured as

the difference between the cost of the inventory and market based upon assumptions about future demand and

charged to the provision for inventory, which is a component of cost of sales. At the point of the loss recognition,

a new, lower cost basis for that inventory is established, and subsequent changes in facts and circumstances do

not result in the restoration or increase in that newly established cost basis. In addition, the Company records a

liability for firm, noncancelable, and unconditional purchase commitments with contract manufacturers and

suppliers for quantities in excess of the Company’s future demand forecasts consistent with its valuation of

excess and obsolete inventory.

(e) Allowance for Doubtful Accounts The allowance for doubtful accounts is based on the Company’s

assessment of the collectibility of customer accounts. The Company regularly reviews the allowance by

considering factors such as historical experience, credit quality, age of the accounts receivable balances,

economic conditions that may affect a customer’s ability to pay, and expected default frequency rates. Trade

receivables are written off at the point when they are considered uncollectible.

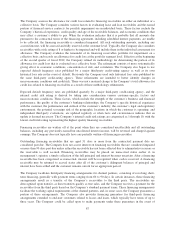

(f) Financing Receivables The Company provides financing arrangements, including leases, financed service

contracts, and loans, for certain qualified end-user customers to build, maintain, and upgrade their networks.

Lease receivables primarily represent sales-type and direct-financing leases. Leases have on average a four-year

term and are usually collateralized by a security interest in the underlying assets, while loan receivables generally

have terms of up to three years. Financed service contracts typically have terms of one to three years and

primarily relate to technical support services.

The Company determines the adequacy of its allowance for credit loss by assessing the risks and losses inherent

in its financing receivables by portfolio segment. The portfolio segment is based on the types of financing offered

by the Company to its customers: lease receivables, loan receivables, and financed service contracts and other.

Effective in the second quarter of fiscal 2012, the Company combined its financing receivables into a single class

as the two prior classes, Established Markets and Growth Markets, now exhibit similar risk characteristics as

reflected by the Company’s historical losses. See Note 7.

86