Cisco 2012 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2012 Cisco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

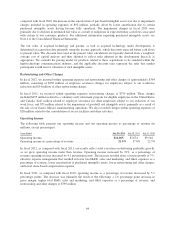

The gross margin percentage for a particular segment may fluctuate, and period-to-period changes in such

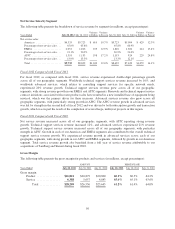

percentages may or may not be indicative of a trend for that segment. Our product and service gross margins may

be impacted by economic downturns or uncertain economic conditions as well as our movement into new market

opportunities, and could decline if any of the factors that impact our gross margins are adversely affected in

future periods.

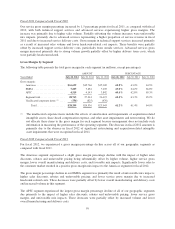

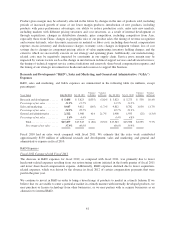

Fiscal 2011 Compared with Fiscal 2010

For fiscal 2011, as compared with fiscal 2010, the gross margin percentage across all geographic segments

declined primarily due to higher sales discounts, rebates, and unfavorable pricing, as well as due to a product mix

shift. These declines were partially offset by the impacts from increased shipment volume and lower overall

manufacturing costs across all geographic segments.

Factors That May Impact Net Sales and Gross Margin

Net product sales may continue to be affected by factors, including global economic downturns and related

market uncertainty, that have resulted in reduced IT-related capital spending in our enterprise, service provider,

public sector, and commercial markets; changes in the geopolitical environment and global economic conditions;

competition, including price-focused competitors from Asia, especially from China; new product introductions;

sales cycles and product implementation cycles; changes in the mix of our customers between service provider

and enterprise markets; changes in the mix of direct sales and indirect sales; variations in sales channels; and

final acceptance criteria of the product, system, or solution as specified by the customer. Sales to the service

provider market have been and may be in the future characterized by large and sporadic purchases, especially

relating to our router sales and sales of certain products within our Collaboration and Data Center product

categories. In addition, service provider customers typically have longer implementation cycles; require a

broader range of services, including network design services; and often have acceptance provisions that can lead

to a delay in revenue recognition. Certain of our customers in certain emerging countries also tend to make large

and sporadic purchases, and the net sales related to these transactions may similarly be affected by the timing of

revenue recognition. As we focus on new market opportunities, customers may require greater levels of financing

arrangements, service, and support, especially in certain emerging countries, which in turn may result in a delay

in the timing of revenue recognition. To improve customer satisfaction, we continue to focus on managing our

manufacturing lead-time performance, which may result in corresponding reductions in order backlog. A decline

in backlog levels could result in more variability and less predictability in our quarter-to-quarter net sales and

operating results.

Net product sales may also be adversely affected by fluctuations in demand for our products, especially with

respect to telecommunications service providers and Internet businesses, whether or not driven by any slowdown

in capital expenditures in the service provider market; price and product competition in the communications and

information technology industry; introduction and market acceptance of new technologies and products; adoption

of new networking standards; and financial difficulties experienced by our customers. We may, from time to

time, experience manufacturing issues that create a delay in our suppliers’ ability to provide specific components,

resulting in delayed shipments. To the extent that manufacturing issues and any related component shortages

result in delayed shipments in the future, and particularly in periods when we and our suppliers are operating at

higher levels of capacity, it is possible that revenue for a quarter could be adversely affected if such matters are

not remediated within the same quarter. For additional factors that may impact net product sales, see “Part I,

Item 1A. Risk Factors.”

Our distributors and retail partners participate in various cooperative marketing and other programs. Increased

sales to our distributors and retail partners generally result in greater difficulty in forecasting the mix of our

products and, to a certain degree, the timing of orders from our customers. We recognize revenue for sales to our

distributors and retail partners generally based on a sell-through method using information provided by them, and

we maintain estimated accruals and allowances for all cooperative marketing and other programs.

60