BMW 2012 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2012 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

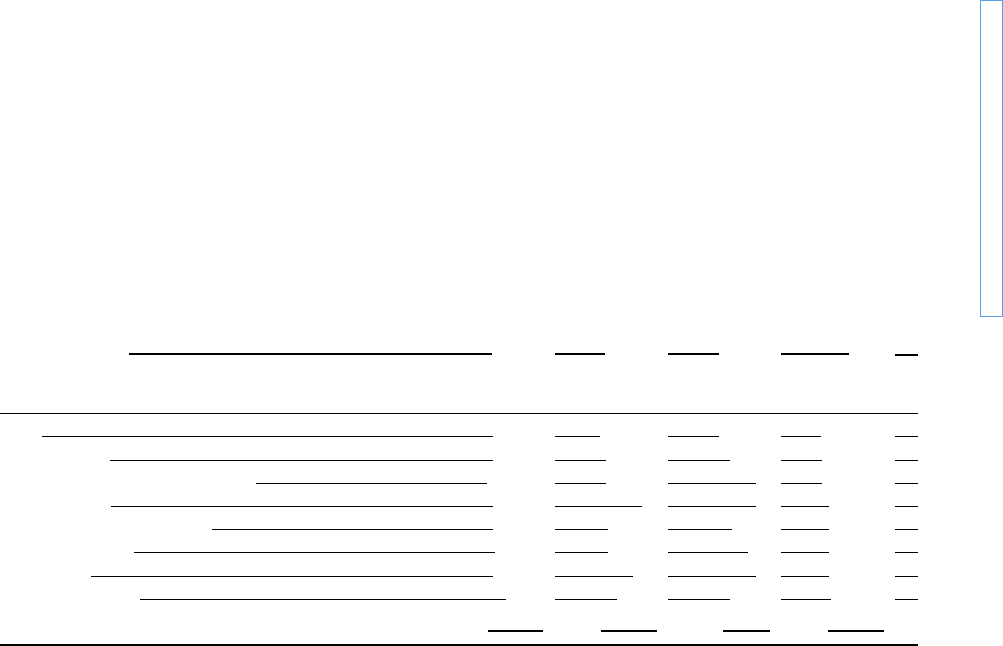

137 GROUP FINANCIAL STATEMENTS

31 December 2012 Maturity Maturity Maturity Total

in € million within between one later than

one year and five years five years

Bonds – 8,482 – 18,375 – 5,071 – 31,928

Liabilities to banks – 4,866 – 4,469 – 678 – 10,013

Liabilities from customer deposits (banking) – 10,139 – 3,028 – – 13,167

Commercial paper – 4,578 – – – 4,578

Asset backed financing transactions – 2,170 – 7,346 – 137 – 9,653

Derivative instruments – 1,146 – 1,085 – 1 – 2,232

Trade payables – 6,424 – 9 – – 6,433

Other financial liabilities – 787 – 249 – 424 – 1,460

Total – 38,592 – 34,561 – 6,311 – 79,464

€ 1,031 million). The equivalent figure for dealer financ-

ing is € 18,157 million (2011: € 16,699 million).

In the case of performance relationships underlying

non-derivative financial instruments, collateral will

be required, information on the credit-standing of

the counterparty obtained or historical data based on

the existing business relationship (i.e. payment pat-

terns to date) reviewed in order to minimise the credit

risk, all depending on the nature and amount of the

exposure that the BMW Group is proposing to enter

into.

Within the financial services business, the financed

items (e. g. vehicles, equipment and property) in the

retail customer and dealer lines of business serve as

first-ranking collateral with a recoverable value. Secu-

rity is also put up by customers in the form of collat-

eral asset pledges, asset assignment and first-ranking

mortgages, supplemented where appropriate by war-

ranties and guarantees. If an item previously accepted

as collateral is acquired, it undergoes a multi-stage

process of repossession and disposal in accordance

with the legal situation prevailing in the relevant mar-

ket. The assets involved are generally vehicles which

can be converted into cash at any time via the dealer

organisation.

Impairment losses are recorded as soon as credit risks

are identified on individual financial assets, using a

methodology specifically designed by the BMW Group.

More detailed information regarding this methodology

is

provided in note 5 in the section on accounting policies.

Creditworthiness testing is an important aspect of the

BMW Group’s credit risk management. Every borrower’s

creditworthiness is tested for all credit financing and

lease contracts entered into by the BMW Group. In the

case of retail customers, creditworthiness is assessed

using validated scoring systems integrated into the pur-

chasing process. In the area of dealer financing, credit-

worthiness is assessed by means of ongoing credit moni-

toring and an internal rating system that takes account

not only of the tangible situation of the borrower but

also of qualitative factors such as past reliability in busi-

ness relations.

The credit risk relating to derivative financial instruments

is minimised by the fact that the Group only enters into

such contracts with parties of first-class credit standing.

The general credit risk on derivative financial instru-

ments utilised by the BMW Group is therefore not con-

sidered to be significant.

A concentration of credit risk with particular borrowers

or groups of borrowers has not been identified in con-

junction with financial instruments.

Further disclosures relating to credit risk – in particular

with regard to the amounts of impairment losses recog-

nised – are provided in the explanatory notes to the

relevant categories of receivables in notes 25, 26 and 30.

Liquidity risk

The following table shows the maturity structure of ex-

pected contractual cash flows (undiscounted) for finan-

cial liabilities: