The Hartford 2015 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2015 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

|

|

96

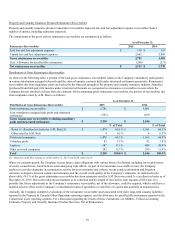

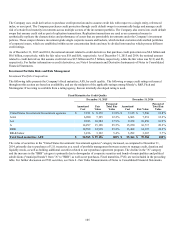

Fixed Maturity Investments

The Company’s investment portfolios primarily consist of investment grade fixed maturity securities. The fair value of fixed maturity

investments was $59.7 billion and $59.9 billion at December 31, 2015 and 2014, respectively. The fair value of these and other invested

assets fluctuate depending on the interest rate environment and other general economic conditions. The weighted average duration of the

portfolio, including fixed maturities, commercial mortgage loans, certain derivatives, and cash equivalents, was approximately 5.5 years

and 5.3 years as of December 31, 2015 and 2014, respectively.

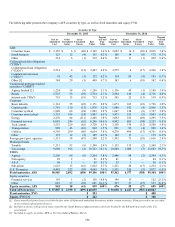

Liabilities

The Company’s issued investment contracts and certain insurance product liabilities, other than non-guaranteed separate accounts,

include asset accumulation vehicles such as fixed annuities, guaranteed investment contracts, other investment and universal life-type

contracts and certain insurance products such as long-term disability.

Asset accumulation vehicles primarily require a fixed rate payment, often for a specified period of time, such as fixed rate annuities with

a market value adjustment feature. The term to maturity of these contracts generally range from less than one year to ten years. A fixed

interest rate is specified in the contract based upon the term selected. These contracts contain surrender values that are based upon a

market value adjustment formula if held for shorter periods. The formula typically is based on current interest crediting rates being

offered for new market value annuity purchases at the time of contract issuance with terms equal to the remaining term to maturity. The

market value adjustment may be positive or negative, depending upon market interest rates at surrender. In addition, certain products

such as corporate owned life insurance contracts and the general account portion of Talcott Resolution's variable annuity products credit

interest to policyholders subject to market conditions and minimum interest rate guarantees. The term to maturity of the asset portfolio

supporting these products may range from short to intermediate.

While interest rate risk associated with many of these products has been reduced through the use of market value adjustment features and

surrender charges, the primary risk associated with these products is that the spread between investment return and credited rate may not

be sufficient to earn targeted returns.

The Company also manages the risk of certain insurance liabilities similarly to investment type products due to the relative predictability

of the aggregate cash flow payment streams. Products in this category may contain significant reliance upon actuarial pricing

assumptions (including mortality and morbidity) and do have some element of cash flow uncertainty. Product examples include

structured settlement contracts, on-benefit annuities (i.e., the annuitant is currently receiving benefits thereon) and short-term and long-

term disability contracts. The cash outflows associated with these policy liabilities are not interest rate sensitive but do vary based on the

timing and amount of benefit payments. The primary risks associated with these products are that the benefits will exceed expected

actuarial pricing and/or that the actual timing of the cash flows will differ from those anticipated, or interest rate levels earned on the

investment portfolio may deviate from those assumed in product pricing, ultimately resulting in an investment return lower than that

assumed in pricing. The average duration of the liability cash flow payments can range from less than one year to in excess of fifteen

years.

Derivatives

The Company utilizes a variety of derivative instruments to mitigate interest rate risk associated with its investment portfolio or hedge

liabilities. Interest rate swaps are primarily used to convert interest receipts or payments to a fixed or variable rate. The use of such

swaps enable the Company to customize contract terms and conditions to desired objectives and manage the duration profile within

established tolerances. Interest rate swaps are also used to hedge the variability in the cash flow of a forecasted purchase or sale of fixed

rate securities due to changes in interest rates. Interest rate caps, floors, swaps, swaptions, and futures may be used to manage portfolio

duration.

As of December 31, 2015 and 2014, notional amounts pertaining to derivatives utilized to manage interest rate risk, including offsetting

positions, totaled $17.8 billion and $19.3 billion, respectively ($17.7 billion and $19.2 billion, respectively, related to investments and

$0.1 billion and $0.1 billion, respectively, related to Talcott Resolution liabilities). The fair value of these derivatives was $(796) and

$(468) as of December 31, 2015 and 2014, respectively. These amounts do not include derivatives associated with the Variable Annuity

Hedging Program.