The Hartford 2015 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2015 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

|

|

103

Credit Risk

Credit risk is defined as the risk to earnings or capital due to uncertainty of an obligor’s or counterparty’s ability or willingness to meet

its obligations in accordance with contractually agreed upon terms. The majority of the Company’s credit risk is concentrated in its

investment holdings but is also present in reinsurance and insurance portfolios. Credit risk is comprised of three major factors: the risk of

change in credit quality, or credit migration risk; the risk of default; and the risk of a change in value due to changes in credit spread. A

decline in creditworthiness is typically associated with an increase in an investment’s credit spread, potentially resulting in an increase in

other-than-temporary impairments and an increased probability of a realized loss upon sale.

The objective of the Company’s enterprise credit risk management strategy is to identify, quantify, and manage credit risk on an

aggregate portfolio basis and to limit potential losses in accordance with an established credit risk management policy. The Company

manages to its credit risk appetite by primarily holding a diversified mix of investment grade issuers and counterparties across its

investment, reinsurance, and insurance portfolios. Potential losses are also limited within portfolios by diversifying across geographic

regions, asset types, and sectors.

The Company manages credit risk exposure from its inception to its maturity or sale. Both the investment and reinsurance areas have

formulated procedures for counterparty approvals and authorizations. Although approval processes may vary by area and type of credit

risk, approval processes establish minimum levels of creditworthiness and financial stability. Credits considered for investment are

subjected to underwriting reviews. Within the investment portfolio, private securities are subject to committee review for approval.

Credit risks are managed on an on-going basis through the use of various processes and analyses. At the investment, reinsurance, and

insurance product levels, fundamental credit analyses are performed at the issuer/counterparty level on a regular basis. To provide a

holistic review within the investment portfolio, fundamental analyses are supported by credit ratings, assigned by nationally recognized

rating agencies or internally assigned, and by quantitative credit analyses. The Company utilizes various risk tools, such as credit value

at risk ("VaR") to measure spread, migration, and default risk on a monthly basis. Issuer and security level risk measures are also

utilized. In the event of deterioration in credit quality, the Company maintains watch lists of problem counterparties within the

investment and reinsurance portfolios. The watch lists are updated based on regular credit examinations and management reviews. The

Company also performs quarterly assessments of probable expected losses in the investment portfolio. The process is conducted on a

sector basis and is intended to promptly assess and identify potential problems in the portfolio and to recognize necessary impairments.

Credit risk policies at the enterprise and operation level ensure comprehensive and consistent approaches to quantifying, evaluating, and

managing credit risk under expected and stressed conditions. These policies define the scope of the risk, authorities, accountabilities,

terms, and limits, and are regularly reviewed and approved by senior management. Aggregate counterparty credit quality and exposure is

monitored on a daily basis utilizing an enterprise-wide credit exposure information system that contains data on issuers, ratings,

exposures, and credit limits. Exposures are tracked on a current and potential basis. Credit exposures are reported regularly to the

Company's Asset Liability Committee ("ALCO") and the ERCC. Exposures are aggregated by ultimate parent across investments,

reinsurance receivables, insurance products with credit risk, and derivative counterparties.

The Company exercises various methods to mitigate its credit risk exposure within its investment and reinsurance portfolios. Some of

the reasons for mitigating credit risk include financial instability or poor credit, avoidance of arbitration or litigation, future uncertainty

of the counterparty, and exposure in excess of risk tolerances. Credit risk within the investment portfolio is most commonly mitigated

through asset sales or the use of derivative instruments. Counterparty credit risk is mitigated through the practice of entering into

contracts only with strong creditworthy institutions and through the practice of holding and posting of collateral. In addition, transactions

cleared through a central clearing house reduce risk due to their ability to require daily variation margin, monitor the Company's ability to

request additional collateral in the event of a counterparty downgrade, and be an independent valuation source. Systemic credit risk is

mitigated through the construction of high-quality, diverse portfolios that are subject to regular underwriting of credit risks. For further

discussion of the Company’s investment and derivative instruments, see MD&A - Enterprise Risk Management, Portfolio Risks and

Risk Management and Note 6 - Investments and Derivative Instruments of Notes to Consolidated Financial Statements. For further

discussion on managing and mitigating credit risk from the use of reinsurance via an enterprise security review process, see MD&A -

Enterprise Risk Management, Insurance Risk Management, Reinsurance as a Risk Management Strategy.

As of December 31, 2015, the Company had no investment exposure to any credit concentration risk of a single issuer or counterparty

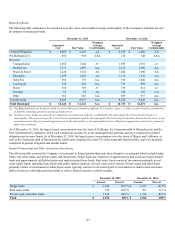

greater than 10% of the Company's stockholders' equity, other than the U.S. government and certain U.S. government securities. For

further discussion of concentration of credit risk in the investment portfolio, see the Concentration of Credit Risk section in Note 6 -

Investments and Derivative Instruments of Notes to Consolidated Financial Statements.