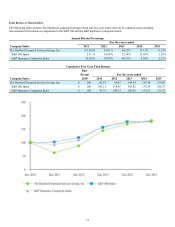

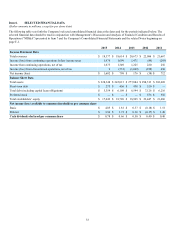

The Hartford 2015 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2015 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

|

|

25

Changes in federal or state tax laws could adversely affect our business, financial condition, results of operations and liquidity.

Changes in federal or state tax laws could have a material adverse effect on our profitability and financial condition, and could result in

our incurring materially higher corporate taxes. Higher tax rates may cause the small businesses we insure to hire fewer workers and

decrease investment in their businesses, including purchasing vehicles, property and equipment, which could adversely affect our

business, financial condition, results of operations and liquidity. Conversely, if income tax rates decline it could adversely affect the

Company's ability to realize the benefits of its deferred tax assets.

In addition, the Company’s tax return reflects certain items, including but not limited to, tax-exempt bond interest, dividends received

deductions, tax credits (such as foreign tax credits), and insurance reserve deductions. There is an increasing risk that, in the context of

deficit reduction or overall tax reform, federal and/or state tax legislation could modify or eliminate these items, impacting the Company,

its investments, investment strategies, and/or its policyholders. Although the specific form of any such legislation is uncertain, changes

to the taxation of municipal bond interest could materially and adversely impact the value of those bonds, limit our investment choices

and depress portfolio yield. Elimination of the dividends received deduction or changes to the taxation of reserving methodologies for

P&C companies could increase the Company’s actual tax rate, thereby reducing earnings. Moreover, many of the products that the

Company previously sold benefit from one or more forms of tax-favored status under current federal and state income tax regimes. For

example, the Company previously sold annuity contracts that allowed policyholders to defer the recognition of taxable income earned

within the contract. Because the Company no longer sells these products, changes in the future taxation of life insurance and/or annuity

contracts will not adversely impact future sales. If, however, the treatment of earnings accrued inside an annuity contract was changed

prospectively, and the tax-favored status of existing contracts was grandfathered, holders of existing contracts would be less likely to

surrender, which would make running off our existing annuity business more difficult.

Regulatory requirements could delay, deter or prevent a takeover attempt that shareholders might consider in their best interests.

Before a person can acquire control of a U.S. insurance company, prior written approval must be obtained from the insurance

commissioner of the state where the domestic insurer is domiciled. Prior to granting approval of an application to acquire control of a

domestic insurer, the state insurance commissioner will consider such factors as the financial strength of the applicant, the acquirer's

plans for the future operations of the domestic insurer, and any such additional information as the insurance commissioner may deem

necessary or appropriate for the protection of policyholders or in the public interest. Generally, state statutes provide that control over a

domestic insurer is presumed to exist if any person, directly or indirectly, owns, controls, holds with the power to vote, or holds proxies

representing 10 percent or more of the voting securities of the domestic insurer or its parent company. Because a person acquiring 10

percent or more of our common stock would indirectly control the same percentage of the stock of our U.S. insurance subsidiaries, the

insurance change of control laws of various U.S. jurisdictions would likely apply to such a transaction. Other laws or required approvals

pertaining to one or more of our existing subsidiaries, or a future subsidiary, may contain similar or additional restrictions on the

acquisition of control of the Company. These laws may discourage potential acquisition proposals and may delay, deter, or prevent a

change of control, including transactions that our Board of Directors and some or all of our shareholders might consider to be desirable.

Changes in accounting principles and financial reporting requirements could result in material changes to our reported results of

operations and financial condition.

U.S. GAAP and related financial reporting requirements are complex, continually evolving and may be subject to varied interpretation

by the relevant authoritative bodies. Such varied interpretations could result from differing views related to specific facts and

circumstances. Changes in U.S. GAAP and financial reporting requirements, or in the interpretation of U.S. GAAP or those

requirements, could result in material changes to our reported results and financial condition.

Other Strategic and Operational Risks

As our Talcott Resolution business continues to runoff, the Company is exposed to a number of risks related to the runoff business

that could adversely affect our financial condition and results of operations.

Despite being in runoff, Talcott Resolution represents a meaningful share of the Company’s earnings. Talcott Resolution’s revenues and

earnings will decline over time as variable and fixed annuity policies lapse. While the Company has been reducing expenses associated

with the Talcott Resolution business as the revenues from that business decline, going forward it may become more difficult to reduce

expenses, particularly corporate and other enterprise shared services costs, and this could adversely affect the Company’s results of

operations going forward. In addition, dividends and distributions from the Company’s life insurance subsidiaries have helped fund a

significant portion of share repurchases and pay downs of debt under the Company’s announced capital management program. As the

Talcott Resolution earnings decline, there will be less retained earnings in the Company’s Talcott Resolution insurance subsidiaries

available to fund capital management actions.