ICICI Bank 2008 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2008 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

F87

Under US GAAP, larger balance, non-homogenous exposures representing significant individual credit exposures (both

funded and non-funded), are evaluated on the basis of borrower’s overall financial condition, resources and payment

record and the realisable value of any collateral. This estimate considers all available evidence including the present

value of the expected future cash flows discounted at the loan’s contractual effective rate and the fair value of collateral.

Allowances recognised on account of reductions of future interest rates as a part of troubled debt restructurings are

accreted as a credit to the provision for loan losses over the tenor of the restructured loan. Each portfolio of smaller-

balance, homogenous loans, including consumer mortgage, installment, revolving credit and most other consumer

loans is individually evaluated for impairment. The allowance for loan losses attributed to these loans is established

via a process that includes an estimate of probable losses inherent in the portfolio, based upon various statistical

analysis.

Under US GAAP, the allowance for loan losses for restructured loans is created by discounting expected cash flows

at contracted interest rates, unlike Indian GAAP, under which current interest rates are used.

Under US GAAP, the allowance on the performing portfolios are based on the estimated probable losses inherent in

the portfolio. The allowance on the performing portfolios are established after considering historical and projected

default rates and loss severities.

Under Indian GAAP, in respect of non-performing loan accounts subjected to restructuring, the account is upgraded

to standard category if the borrower demonstrates, over a minimum period of one year, the ability to repay the loan

in accordance with the contractual terms. However, the process of upgradation under US GAAP is not rule-based and

the timing of upgradation may differ across individual loans.

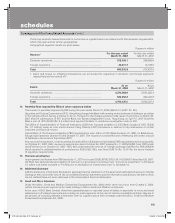

During fiscal years 2006, 2007 and 2008, the Group transferred certain impaired loans to borrower specific funds/

trusts managed by an asset reconstruction company against the issuance of security receipts by the funds/trusts. The

funds/trusts have been set up by the asset reconstruction company under enacted debt recovery legislation in India

and aim to improve the recoveries of banks from non-performing assets by aggregating lender interests and speeding

up enforcement of security interest by lenders. While under Indian GAAP the entire transfer was recognised as a sale,

under US GAAP these transfers are not recognised as a sale due to the following reasons:

• Certain transfers did not qualify for sale accounting under Statement No. 140 on “Accounting for Transfers and

Servicing of Financial Assets and Extinguishments of Liabilities”.

• Certain transfers qualified for sale accounting but were impacted by FASB Interpretation No. 46 on “Consolidation

of Variable Interests” (FIN 46)/FASB Interpretation No 46(R) (FIN 46(R)). The funds/trusts to which these loans

have been transferred are variable interest entities within the definition contained in FIN 46(R). As the Bank is the

‘Primary Beneficiary’ of certain funds/trusts, it is required under US GAAP to consolidate these entities.

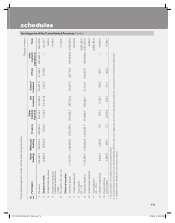

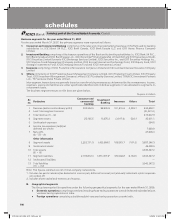

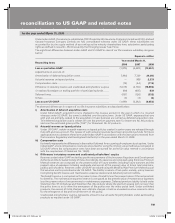

The difference in aggregate allowance for loan losses between Indian GAAP and US GAAP for the fiscal years 2006,

2007 and 2008 as attributable to the reconciling items is given in the table below.

Rupees in million

Reconciling items Year ended March 31,

2006 2007 2008

Differences due to provision on loans classified as troubled debt

restructuring under US GAAP (includes cases transferred to asset

reconstruction company) ......................................................................... (2,047.2) (547.6) 1,487.9

Differences due to provisions on loans classified as other impaired under

US GAAP .................................................................................................. (5,037.5) (4,462.1) (6,526.5)

Differences due to provisions created on performing assets ................. 1,870.0 5,310.0 633.9

Total difference in allowance for loan losses ....................................... (5,214.7) 300.3 (4,404.7)

b) Business combinations

The differences arising due to business combinations are primarily on account of:

i) Determination of the accounting acquirer.

ii) Accounting of intangible assets.

Under US GAAP, the amalgamation between ICICI Bank Limited and ICICI Limited was accounted for as a

reverse acquisition in fiscal 2003. This means that ICICI Limited was recognised as the accounting acquirer in the

amalgamation, although ICICI Bank was the legal acquirer. On the acquisition date, ICICI held a 46% ownership

interest in ICICI Bank. Accordingly, the acquisition of the balance 54% ownership interest has been accounted for as

a step-acquisition. Under Indian GAAP, ICICI Bank Limited was recognised as the legal and the accounting acquirer

and the assets and liabilities of ICICI Limited were incorporated in the books of ICICI Bank Limited in accordance

with the purchase method of accounting. Further, under US GAAP, the amalgamation resulted in goodwill and

intangible assets while the amalgamation under Indian GAAP resulted in a capital reserve (negative goodwill),

which was accounted for as Revenue and Other Reserves according to the scheme of amalgamation.

reconciliation to US GAAP and related notes

for the year ended March 31, 2008

ICICI_BK_AR_2008_(F47_F92).indd 87ICICI_BK_AR_2008_(F47_F92).indd 87 6/20/08 3:33:25 PM6/20/08 3:33:25 PM