MetLife 2002 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94

|

|

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

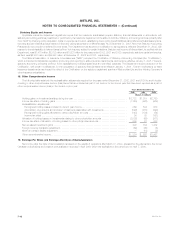

Statutory Equity and Income

Applicable insurance department regulations require that the insurance subsidiaries prepare statutory financial statements in accordance with

statutory accounting practices prescribed or permitted by the insurance department of the state of domicile. Statutory accounting practices primarily differ

from GAAP by charging policy acquisition costs to expense as incurred, establishing future policy benefit liabilities using different actuarial assumptions,

reporting surplus notes as surplus instead of debt and valuing securities on a different basis. As of December 31, 2001, New York Statutory Accounting

Practices did not provide for deferred income taxes. The Department has adopted a modification to its regulations, effective December 31, 2002, with

respect to the admissibility of deferred taxes by New York insurers, subject to certain limitations. Statutory net income of Metropolitan Life, as filed with the

Department, was $1,478 million, $2,782 million and $1,027 million for the years ended 2002, 2001 and 2000, respectively; statutory capital and surplus,

as filed, was $6,986 million and $5,358 million at December 31, 2002 and 2001, respectively.

The National Association of Insurance Commissioners (‘‘NAIC’’) adopted the Codification of Statutory Accounting Principles (the ‘‘Codification’’),

which is intended to standardize regulatory accounting and reporting to state insurance departments, and became effective January 1, 2001. However,

statutory accounting principles continue to be established by individual state laws and permitted practices. The Department required adoption of the

Codification, with certain modifications, for the preparation of statutory financial statements effective January 1, 2001. Further modifications by state

insurance departments may impact the effect of the Codification on the statutory capital and surplus of Metropolitan Life and the Holding Company’s

other insurance subsidiaries.

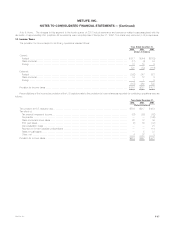

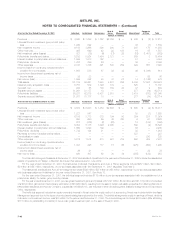

18. Other Comprehensive Income

The following table sets forth the reclassification adjustments required for the years ended December 31, 2002, 2001 and 2000 to avoid double-

counting in other comprehensive income (loss) items that are included as part of net income for the current year that have been reported as a part of

other comprehensive income (loss) in the current or prior year:

Years Ended December 31,

2002 2001 2000

(Dollars in millions)

Holding gains on investments arising during the year ********************************************** $ 3,722 $1,319 $2,789

Income tax effect of holding gains ************************************************************** (1,169) (520) (969)

Reclassification adjustments:

Recognized holding losses included in current year income *************************************** 369 534 989

Amortization of premiums and accretion of discounts associated with investments ******************** (526) (488) (499)

Recognized holding gains allocated to other policyholder amounts ********************************* (145) (134) (54)

Income tax effect ************************************************************************** 95 35 (151)

Allocation of holding losses on investments relating to other policyholder amounts ********************** (2,832) (69) (971)

Income tax effect of allocation of holding losses to other policyholder amounts************************* 889 27 338

Net unrealized investment gains **************************************************************** 403 704 1,472

Foreign currency translation adjustment********************************************************** (69) (60) (6)

Minimum pension liability adjustment ************************************************************ — (18) (9)

Other comprehensive income ****************************************************************** $ 334 $ 626 $1,457

19. Earnings Per Share and Earnings After Date of Demutualization

Net income after the date of demutualization is based on the results of operations after March 31, 2000, adjusted for the payments to the former

Canadian policyholders and costs of demutualization recorded in April 2000 which are applicable to the period prior to April 7, 2000.

MetLife, Inc.

F-42