MetLife 2002 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The amounts accumulated in other comprehensive loss relating to cash flow hedges were gains of $21 million for both the years ended

December 31, 2002 and 2001. During the year ended December 31, 2002, the Company recognized other comprehensive gains of $4 million relating

to the effective portion of cash flow hedges. Reclassifications are recognized over the life of the hedged item. During the year ended December 31,

2002, $4 million of other comprehensive loss was reclassified into net investment income. Approximately $3 million of the gains reported in accumulated

other comprehensive loss is expected to be reclassified into net investment income during the year ending December 31, 2003, as the underlying

investments mature or expire according to their original terms.

For the years ended December 31, 2002 and 2001, the Company recognized net investment losses of $11 million and net investment gains of

$5 million, respectively, from derivatives not qualifying as accounting hedges. The use of these non-speculative derivatives is permitted by the

Department.

The cumulative effect of the adoption of SFAS 133, as of January 1, 2001, resulted in $11 million of other comprehensive income, net of income

taxes of $6 million.

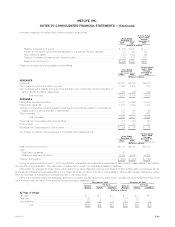

8. Separate Accounts

Separate accounts include two categories of account types: non-guaranteed separate accounts totaling $44,925 million and $48,912 million at

December 31, 2002 and 2001, respectively, for which the policyholder assumes the investment risk, and guaranteed separate accounts totaling

$14,768 million and $13,802 million at December 31, 2002 and 2001, respectively, for which the Company contractually guarantees either a minimum

return or account value to the policyholder.

Fees charged to the separate accounts by the Company (including mortality charges, policy administration fees and surrender charges) are reflected

in the Company’s revenues as universal life and investment-type product policy fees and totaled $544 million, $564 million and $667 million for the years

ended December 31, 2002, 2001 and 2000, respectively. Guaranteed separate accounts consisted primarily of Met Managed Guaranteed Interest

Contracts and participating close out contracts. The average interest rates credited on these contracts were 4.8% and 7.0% at December 31, 2002 and

2001, respectively. The assets that support these liabilities were comprised of $12,536 million and $11,888 million in fixed maturities at December 31,

2002 and 2001, respectively. The portfolios are segregated from other investments and are managed to minimize liquidity and interest rate risk. In order

to minimize the risk of early withdrawals to invest in instruments yielding a higher return, these investment products carry a graded surrender charge as

well as a market value adjustment.

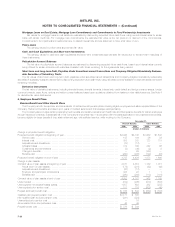

9. Debt

Debt consisted of the following:

December 31,

2002 2001

(Dollars in millions)

Senior notes, interest rates ranging from 5.25% to 7.25%, maturity dates ranging from 2006 to 2032 ****** $2,539 $1,546

Surplus notes, interest rates ranging from 6.30% to 7.88%, maturity dates ranging from 2003 to 2025 ***** 1,632 1,630

Investment related exchangeable debt, interest rate of 4.90%**************************************** — 195

Fixed rate notes, interest rates ranging from 2.97% to 12.00%, maturity dates ranging from 2003 to 2019 ** 83 87

Capital lease obligations *********************************************************************** 21 23

Other notes with varying interest rates *********************************************************** 150 147

Total long-term debt ************************************************************************** 4,425 3,628

Total short-term debt ************************************************************************** 1,161 355

Total ******************************************************************************* $5,586 $3,983

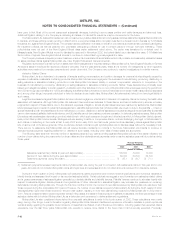

The Company maintains committed and unsecured credit facilities aggregating $2,434 million ($1,140 million expiring in 2003 and $1,294 million

expiring in 2005). If these facilities were drawn upon, they would bear interest at rates stated in the agreements. The facilities can be used for general

corporate purposes and also provide support for the Company’s commercial paper program. At December 31, 2002, the Company had drawn

approximately $28 million under the facilities expiring in 2005 at interest rates ranging from 4.39% to 5.57%. At December 31, 2002, the Company had

approximately $625 million in letters of credit from various banks.

Payments of interest and principal on the surplus notes, subordinated to all other indebtedness, may be made only with the prior approval of the

insurance department of the state of domicile. Subject to the prior approval of the Superintendent, the $300 million 7.45% surplus notes due 2023 may

be redeemed, in whole or in part, at the election of Metropolitan Life at any time on or after November 1, 2003 and, if redeemed prior to November 2013,

would include a premium.

The investment-related exchangeable debt instrument is payable in cash or by delivery of an underlying security owned by the Company. The

amount of the debt payable at maturity is greater than the principal of the debt if the market value of the underlying security appreciates above certain

levels at the date of debt repayment as compared to the market value of the underlying security at the date of debt issuance. At December 31, 2001, the

underlying security pledged as collateral had a market value of $240 million.

The aggregate maturities of long-term debt for the Company are $448 million in 2003, $12 million in 2004, $395 million in 2005, $601 million in

2006, $4 million in 2007 and $2,965 million thereafter.

Short-term debt of the Company consisted of commercial paper with a weighted average interest rate of 1.5% and a weighted average maturity of

74 days at December 31, 2002. Short-term debt of the Company consisted of commercial paper with a weighted average interest rate of 2.1% and a

weighted average maturity of 87 days at December 31, 2001. The Company also has other collateralized borrowings with a weighted average coupon

rate of 5.83% and a weighted average maturity of 34 days at December 31, 2002. Such securities had a weighted average coupon rate of 7.25% and a

weighted average maturity of 30 days at December 31, 2001.

Interest expense related to the Company’s indebtedness included in other expenses was $288 million, $252 million and $377 million for the years

ended December 31, 2002, 2001 and 2000, respectively.

MetLife, Inc.

F-30