MetLife 2002 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

The Company’s principal cash inflows from its investment activities result from repayments of principal, proceeds from maturities and sales of

invested assets and investment income. The primary liquidity concerns with respect to these cash inflows are the risk of default by debtors and market

volatilities. The Company closely monitors and manages these risks through its credit risk management process.

Liquid Assets. An integral part of the Company’s liquidity management is the amount of liquid assets it holds. Liquid assets include cash, cash

equivalents, short-term investments, marketable fixed maturities and equity securities. At December 31, 2002 and 2001, the Company had $127 billion

and $108 billion in liquid assets, respectively.

Global Funding Sources. Liquidity is also provided by a variety of both short- and long-term instruments, including repurchase agreements,

commercial paper, medium- and long-term debt, capital securities and stockholders’ equity. The diversity of the Company’s funding sources enhances

funding flexibility and limits dependence on any one source of funds, and generally lowers the cost of funds.

At December 31, 2002 and 2001, the Company had $1,161 million and $355 million in short-term debt outstanding, respectively, and $4,425

million and $3,628 million in long-term debt outstanding, respectively. See ‘‘— The Holding Company — Global Funding Sources.’’

MetLife Funding serves as a centralized finance unit for Metropolitan Life. Pursuant to a support agreement, Metropolitan Life has agreed to cause

MetLife Funding to have a tangible net worth of at least one dollar. At December 31, 2002 and 2001, MetLife Funding had a tangible net worth of

$10.7 million and $10.6 million, respectively. MetLife Funding raises funds from various funding sources and uses the proceeds to extend loans, through

MetLife Credit Corp., a subsidiary of Metropolitan Life, to the Holding Company, Metropolitan Life and other affiliates. MetLife Funding manages its

funding sources to enhance the financial flexibility and liquidity of Metropolitan Life and other affiliated companies. At December 31, 2002 and 2001,

MetLife Funding had total outstanding liabilities, including accrued interest payable, of $400 million and $133 million, respectively, consisting primarily of

commercial paper.

Credit Facilities. The Company maintains committed and unsecured credit facilities aggregating $2.43 billion ($1.14 billion expiring in 2003 and

$1.29 billion expiring in 2005). If these facilities were drawn upon, they would bear interest at varying rates stated in the agreements. The facilities can be

used for general corporate purposes and also as back-up lines of credit for the Company’s commercial paper program. At December 31, 2002, the

Company had drawn approximately $28 million under the facilities expiring in 2005 at interest rates ranging from 4.39% to 5.57%.

Liquidity Uses

Insurance Liabilities. The Company’s principal cash outflows primarily relate to the liabilities associated with its various life insurance, property and

casualty, annuity and group pension products, operating expenses and income taxes, as well as principal and interest on its outstanding debt

obligations. Liabilities arising from its insurance activities primarily relate to benefit payments under the aforementioned products, as well as payments for

policy surrenders, withdrawals and loans.

Investment and Other. Additional cash outflows include those related to obligations of securities lending activities, investments in real estate, limited

partnership and joint ventures, as well as legal liabilities.

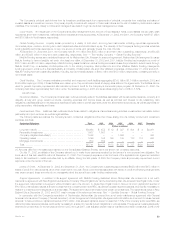

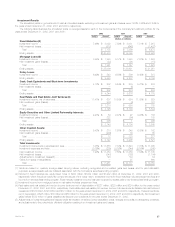

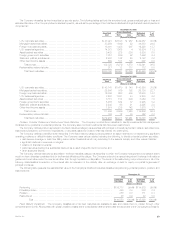

The following table summarizes the Company’s major contractual obligations (other than those arising from its ordinary product and investment

purchase activities):

Contractual Obligations Total 2003 2004 2005 2006 2007 Thereafter

(Dollars in millions)

Long-term debt(1) *************************************** $4,460 $ 452 $ 12 $ 397 $ 604 $ 4 $2,991

Partnership investments ********************************** 1,667 1,667 — — — — —

Company-obligated securities(1) *************************** 1,356 — — 1,006 — — 350

Operating leases **************************************** 1,399 192 166 149 133 116 643

Mortgage commitments ********************************** 859 859 — — — — —

Total*************************************************** $9,741 $3,170 $178 $1,552 $ 737 $120 $3,984

(1) Amounts differ from the balances presented on the Consolidated Balance Sheets, which are shown net of related discounts.

On July 11, 2002, an affiliate of the Company elected not to make future payments required by the terms of a non-recourse loan obligation. The

book value of this loan was $16 million at December 31, 2002. The Company’s exposure under the terms of the applicable loan agreement is limited

solely to its investment in certain securities held by an affiliate. During the first quarter of 2003 the Company made all previously required and current

payments under the terms of the loan.

Letters of Credit. At December 31, 2002 and December 31, 2001, the Company had outstanding approximately $625 million and $473 million in

letters of credit from various banks, all of which expire within one year. Since commitments associated with letters of credit and financing arrangements

may expire unused, these amounts do not necessarily reflect the actual future cash funding requirements.

Support Agreements. In addition to its support agreement with MetLife Funding described above, Metropolitan Life entered into a net worth

maintenance agreement with New England Life Insurance Company (‘‘New England Life’’) at the time Metropolitan Life acquired New England Life. Under

the agreement, Metropolitan Life agreed, without limitation as to the amount, to cause New England Life to have a minimum capital and surplus of

$10 million, total adjusted capital at a level not less than the company action level RBC, as defined by state insurance statutes, and liquidity necessary to

enable it to meet its current obligations on a timely basis. The agreement may be terminated under certain circumstances. The capital and surplus of New

England Life at December 31, 2002 and 2001 was in excess of the referenced amounts. See ‘‘— Liquidity Sources — Global Funding Sources.’’

In connection with the Company’s acquisition of GenAmerica, Metropolitan Life entered into a net worth maintenance agreement with General

American Life Insurance Company (‘‘General American’’). Under the agreement, Metropolitan Life agreed without limitation as to amount to cause General

American to have a minimum capital and surplus of $10 million, total adjusted capital at a level not less than 180% of the company action level RBC, as

defined by state insurance statutes, and liquidity necessary to enable it to meet its current obligations on a timely basis. The agreement was subsequently

amended to provide that, for the five year period from 2003 through 2007, total adjusted capital must be maintained at a level not less than 200% of the

MetLife, Inc. 23