MetLife 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

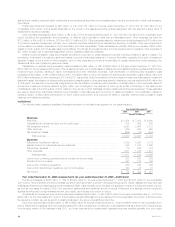

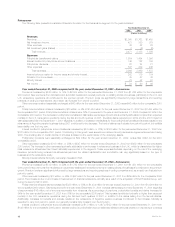

Reinsurance

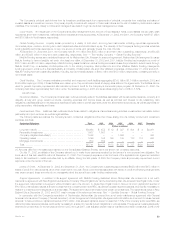

The following table presents consolidated financial information for the Reinsurance segment for the years indicated:

Year Ended December 31,

2002 2001 2000

(Dollars in millions)

Revenues

Premiums ************************************************************************** $2,005 $1,762 $1,450

Net investment income *************************************************************** 421 390 379

Other revenues ********************************************************************* 43 42 29

Net investment gains (losses) ********************************************************* 2 (6) (2)

Total revenues ****************************************************************** 2,471 2,188 1,856

Expenses

Policyholder benefits and claims ******************************************************* 1,554 1,484 1,096

Interest credited to policyholder account balances **************************************** 146 122 109

Policyholder dividends**************************************************************** 22 24 21

Other expenses ********************************************************************* 547 439 446

Total expenses****************************************************************** 2,269 2,069 1,672

Income before provision for income taxes and minority interest****************************** 202 119 184

Provision for income taxes ************************************************************ 43 27 48

Minority interest ********************************************************************* 75 52 67

Net income ************************************************************************ $84$40 $69

Year ended December 31, 2002 compared with the year ended December 31, 2001—Reinsurance

Premiums increased by $243 million, or 14%, to $2,005 million for the year ended December 31, 2002 from $1,762 million for the comparable

2001 period. New premiums from facultative and automatic treaties and renewal premiums on existing blocks of business, particularly in the U.S. and

U.K. reinsurance operations, all contributed to the premium growth. Premium levels are significantly influenced by large transactions and reporting

practices of ceding companies and, as a result, can fluctuate from period to period.

Other revenues remained essentially unchanged at $43 million for the year ended December 31, 2002 versus $42 million for the comparable 2001

period.

Policyholder benefits and claims increased by $70 million, or 5%, to $1,554 million for the year ended December 31, 2002 from $1,484 million for

the comparable 2001 period. Policyholder benefits and claims were 78% of premiums for the year ended December 31, 2002 compared to 84% in the

comparable 2001 period. The decrease in policyholder benefits and claims as a percentage of premiums is primarily attributable to higher than expected

mortality in the U.S. reinsurance operations during the first and fourth quarters of 2001, favorable claims experience in 2002 and the 2001 impact of

claims associated with the September 11, 2001 tragedies. In addition, increases in the liabilities for future policyholder benefits and adverse results on the

reinsurance of Argentine pension business during 2001 contributed to the decrease. The level of claims may fluctuate from period to period, but exhibits

less volatility over the long term.

Interest credited to policyholder account balances increased by $24 million, or 20%, to $146 million for the year ended December 31, 2002 from

$122 million for the comparable 2001 period. Contributing to this growth were several new deferred annuity reinsurance agreements executed during

2002. The crediting rate on certain blocks of annuities is based on the performance of the underlying assets.

Policyholder dividends were essentially unchanged at $22 million for the year ended December 31, 2002, versus $24 million for the 2001

comparable period.

Other expenses increased by $108 million, or 25%, to $547 million for the year ended December 31, 2002 from $439 million for the comparable

2001 period. The increase in other expenses is primarily attributable to an increase in reinsurance business in the U.K., which is characterized by higher

initial reinsurance allowances than those historically experienced in the segment. These expenses fluctuate depending on the mix of the underlying

insurance products being reinsured as allowances paid and the related capitalization and amortization can vary significantly based on the type of

business and the reinsurance treaty.

Minority interest reflects third-party ownership interests in RGA.

Year ended December 31, 2001 compared with the year ended December 31, 2000—Reinsurance

Premiums increased by $312 million, or 22%, to $1,762 million for the year ended December 31, 2001 from $1,450 million for the comparable

2000 period. New premiums from facultative and automatic treaties and renewal premiums on existing blocks of business all contributed to the premium

growth. Premium levels are significantly influenced by large transactions and reporting practices of ceding companies and, as a result, can fluctuate from

period to period.

Other revenues increased by $13 million, or 45%, to $42 million for the year ended December 31, 2001 from $29 million for the comparable 2000

period. The increase is due to an increase in fees earned on financial reinsurance, primarily as a result of the acquisition of RGA Financial Group, LLC

during the second half of 2000.

Policyholder benefits and claims increased by $388 million, or 35%, to $1,484 million for the year ended December 31, 2001 from $1,096 million for

the comparable 2000 period. Claims experience for the year ended December 31, 2001 includes claims arising from the September 11, 2001 tragedies

of approximately $16 million, net of amounts recoverable from reinsurers. As a percentage of premiums, policyholder benefits and claims increased to

84% for the year ended December 31, 2001 from 76% for the comparable 2000 period. This increase is attributed primarily to higher than expected

mortality in the U.S. reinsurance operations during the first and fourth quarters of 2001, in addition to the claims arising from the terrorist attacks.

Additionally, increases for benefits and adverse results on the reinsurance of Argentine pension business contributed to the increase. Mortality is

expected to vary from period to period, but generally remains fairly constant over the long term.

Interest credited to policyholder account balances increased by $13 million, or 12%, to $122 million for the year ended December 31, 2001 from

$109 million for the comparable 2000 period. Interest credited to policyholder account balances relates to amounts credited on deposit-type contracts

MetLife, Inc.

16