MetLife 2002 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

inherently uncertain. Many of these policies, estimates and related judgments are common in the insurance and financial services industries; others are

specific to the Company’s businesses and operations.

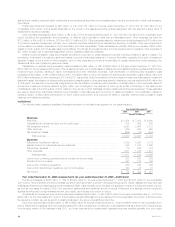

Investments

The Company’s principal investments are in fixed maturities, mortgage loans and real estate, all of which are exposed to three primary sources of

investment risk: credit, interest rate and market valuation. The financial statement risks are those associated with the recognition of impairments and

income, as well as the determination of fair values. The assessment of whether impairments have occurred is based on management’s case-by-case

evaluation of the underlying reasons for the decline in fair value. Management considers a wide range of factors about the security issuer and uses its

best judgment in evaluating the cause of the decline in the estimated fair value of the security and in assessing the prospects for near-term recovery.

Inherent in management’s evaluation of the security are assumptions and estimates about the operations of the issuer and its future earnings potential.

Considerations used by the Company in the impairment evaluation process include, but are not limited to: (i) the length of time and the extent to which the

market value has been below amortized cost; (ii) the potential for impairments of securities when the issuer is experiencing significant financial difficulties;

(iii) the potential for impairments in an entire industry sector or sub-sector; (iv) the potential for impairments in certain economically depressed geographic

locations; (v) the potential for impairments of securities where the issuer, series of issuers or industry has suffered a catastrophic type of loss or has

exhausted natural resources; and (vi) other subjective factors, including concentrations and information obtained from regulators and rating agencies. In

addition, the earnings on certain investments are dependent upon market conditions, which could result in prepayments and changes in amounts to be

earned due to changing interest rates or equity markets. The determination of fair values in the absence of quoted market values is based on valuation

methodologies, securities the Company deems to be comparable and assumptions deemed appropriate given the circumstances. The use of different

methodologies and assumptions may have a material effect on the estimated fair value amounts.

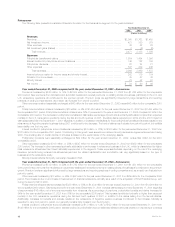

Derivatives

The Company enters into freestanding derivative transactions primarily to manage the risk associated with variability in cash flows related to the

Company’s financial assets and liabilities or to changing fair values. The Company also purchases investment securities and issues certain insurance and

reinsurance policies with embedded derivatives. The associated financial statement risk is the volatility in net income which can result from (i) changes in

fair value of derivatives not qualifying as accounting hedges, and (ii) ineffectiveness of designated hedges in an environment of changing interest rates or

fair values. In addition, accounting for derivatives is complex, as evidenced by significant authoritative interpretations of the primary accounting standards

which continue to evolve, as well as the significant judgments and estimates involved in determining fair value in the absence of quoted market values.

These estimates are based on valuation methodologies and assumptions deemed appropriate in the circumstances. Such assumptions include

estimated market volatility and interest rates used in the determination of fair value where quoted market values are not available. The use of different

assumptions may have a material effect on the estimated fair value amounts.

Deferred Policy Acquisition Costs

The Company incurs significant costs in connection with acquiring new insurance business. These costs, which vary with and are primarily related to

the production of new business, are deferred. The recovery of such costs is dependent upon the future profitability of the related business. The amount

of future profit is dependent principally on investment returns, mortality, morbidity, persistency, expenses to administer the business, creditworthiness of

reinsurance counterparties and certain economic variables, such as inflation. Of these factors, the Company anticipates that investment returns are most

likely to impact the rate of amortization of such costs. The aforementioned factors enter into management’s estimates of gross margins and profits, which

generally are used to amortize such costs. Revisions to estimates result in changes to the amounts expensed in the reporting period in which the

revisions are made and could result in the impairment of the asset and a charge to income if estimated future gross margins and profits are less than

amounts deferred. In addition, the Company utilizes the reversion to the mean assumption, a standard industry practice, in its determination of the

amortization of deferred policy acquisition costs. This practice assumes that the expectation for long-term appreciation in equity markets is not changed

by minor short-term market fluctuations, but that it does change when large interim deviations have occurred.

Future Policy Benefits

The Company establishes liabilities for amounts payable under insurance policies, including traditional life insurance, annuities and disability

insurance. Generally, amounts are payable over an extended period of time and the profitability of the products is dependent on the pricing of the

products. Principal assumptions used in pricing policies and in the establishment of liabilities for future policy benefits are mortality, morbidity, expenses,

persistency, investment returns and inflation.

The Company also establishes liabilities for unpaid claims and claims expenses for property and casualty insurance. Pricing of this insurance takes

into account the expected frequency and severity of losses, the costs of providing coverage, competitive factors, characteristics of the insured and the

property covered, and profit considerations. Liabilities for property and casualty insurance are dependent on estimates of amounts payable for claims

reported but not settled and claims incurred but not reported. These estimates are influenced by historical experience and actuarial assumptions of

current developments, anticipated trends and risk management strategies.

Differences between the actual experience and assumptions used in pricing these policies and in the establishment of liabilities result in variances in

profit and could result in losses.

Reinsurance

The Company enters into reinsurance transactions as both a provider and a purchaser of reinsurance. Accounting for reinsurance requires extensive

use of assumptions and estimates, particularly related to the future performance of the underlying business and the potential impact of counterparty credit

risks. The Company periodically reviews actual and anticipated experience compared to the aforementioned assumptions used to establish policy

benefits and evaluates the financial strength of counterparties to its reinsurance agreements using criteria similar to that evaluated in the security

impairment process discussed above. Additionally, for each of its reinsurance contracts, the Company must determine if the contract provides

indemnification against loss or liability relating to insurance risk, in accordance with applicable accounting standards. The Company must review all

contractual features, particularly those that may limit the amount of insurance risk to which the Company is subject or features that delay the timely

reimbursement of claims. If the Company determines that a contract does not expose it to a reasonable possibility of a significant loss from insurance risk,

the Company records the contract using the deposit method of accounting.

Litigation

The Company is a party to a number of legal actions. Given the inherent unpredictability of litigation, it is difficult to estimate the impact of litigation on

the Company’s consolidated financial position. Liabilities are established when it is probable that a loss has been incurred and the amount of the loss can

MetLife, Inc.

6