MetLife 2002 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2002 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

|

|

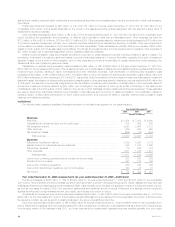

Other sources of the Holding Company’s liquidity include programs for short- and long-term borrowing, as needed, arranged through Metropolitan

Life.

Credit Facilities. The Holding Company maintains approximately $1.25 billion in a committed and unsecured credit facility that it shares with

Metropolitan Life and MetLife Funding, Inc. (‘‘MetLife Funding’’) expiring in 2005. If these facilities were drawn upon, they would bear interest at varying

rates stated in the agreements. This facility is primarily used as back-up lines of credit for its commercial paper program. At December 31, 2002, the

Holding Company, Metropolitan Life or MetLife Funding had not drawn against this credit facility.

Liquidity Uses

The primary uses of liquidity of the Holding Company include cash dividends on common stock, service on debt, contributions to subsidiaries,

payment of general operating expenses and the repurchase of the Holding Company’s common stock.

Dividends. In the fourth quarter of 2002, the Holding Company declared an annual dividend for 2002 of $0.21 per share. The 2002 dividend

represented an increase of $0.01 per share from the 2001 annual dividend of $0.20 per share. Dividends, if any, in any year will be determined by the

Holding Company’s Board of Directors after taking into consideration factors such as the Holding Company’s current earnings, expected medium- and

long-term earnings, financial condition, regulatory capital position, and applicable governmental regulations and policies.

Capital Contributions to Subsidiaries. In 2002, the Holding Company contributed $500 million to Metropolitan Life and in 2001, contributed $770

million to Metropolitan Insurance and Annuity Company (‘‘MIAC’’).

Share Repurchase. On February 19, 2002, the Holding Company’s Board of Directors authorized a $1 billion common stock repurchase program.

This program began after the completion of the March 28, 2001 and June 27, 2000 repurchase programs, each of which authorized the repurchase of

$1 billion of common stock. Under these authorizations, the Holding Company may purchase common stock from the MetLife Policyholder Trust, in the

open market and in privately negotiated transactions. The Holding Company acquired 15,244,492 and 45,242,966 shares of common stock for

$471 million and $1,322 million during the years ended December 31, 2002 and 2001, respectively. At December 31, 2002 the Holding Company had

approximately $806 million remaining on its existing share repurchase authorization. The Company does not anticipate any share repurchases in the first

six months of 2003 and any repurchases in the remainder of 2003 will be dependent upon several factors, including the Company’s capital position, its

financial strength and credit ratings, general market conditions and the price of the Company’s stock.

Support Agreements. In 2002, the Holding Company entered into a net worth maintenance agreement with three of its insurance subsidiaries,

MetLife Investors Insurance Company, First MetLife Investors Insurance Company and MetLife Investors Insurance Company of California. Under the

agreements, the Holding Company agreed, without limitation as to the amount, to cause each of these subsidiaries to have a minimum capital and

surplus of $10 million (or, with respect to MetLife Investors Insurance Company of California, $5 million), total adjusted capital at a level not less than

150% of the company action level RBC, as defined by state insurance statutes, and liquidity necessary to enable it to meet its current obligations on a

timely basis. The capital and surplus of each of these subsidiaries at December 31, 2002 was in excess of the referenced amounts.

The Holding Company has agreed to make capital contributions, in any event not to exceed $120 million, to MIAC in the aggregate amount of the

excess of (i) the debt service payments required to be made, and the capital expenditure payments required to be made or reserved for, in connection

with the affiliated borrowings arranged in December 2001 to fund the purchase by MIAC of certain real estate properties from Metropolitan Life during the

two year period following the date of the borrowings, over (ii) the cash flows generated by these properties.

Based on management’s analysis of its expected cash inflows from the dividends it receives from subsidiaries, including Metropolitan Life, that are

permitted to be paid without prior insurance regulatory approval and its portfolio of liquid assets and other anticipated cash flows, management believes

there will be sufficient liquidity to enable the Holding Company to make payments on debt, make dividend payments on its common stock, pay all

operating expenses and meet other obligations.

The Company

Capital

Risk-Based Capital (‘‘RBC’’). Section 1322 of the New York Insurance Law requires that New York domestic life insurers report their RBC based on

a formula calculated by applying factors to various asset, premium and statutory reserve items, and similar rules apply to each of the Company’s

domestic insurance subsidiaries. The formula takes into account the risk characteristics of the insurer, including asset risk, insurance risk, interest rate risk

and business risk. Section 1322 gives the Superintendent explicit regulatory authority to require various actions by, or take various actions against,

insurers whose total adjusted capital does not exceed certain RBC levels. At December 31, 2002, Metropolitan Life’s and each of the Holding

Company’s domestic insurance subsidiaries’ total adjusted capital was in excess of each of the RBC levels required by each state of domicile.

The National Association of Insurance Commissioners (‘‘NAIC’’) adopted the Codification of Statutory Accounting Principles (the ‘‘Codification’’),

which is intended to standardize regulatory accounting and reporting to state insurance departments and became effective January 1, 2001. However,

statutory accounting principles continue to be established by individual state laws and permitted practices. The Department required adoption of the

Codification with certain modifications for the preparation of statutory financial statements of insurance companies domiciled in New York effective

January 1, 2001. Effective December 31, 2002, the Department adopted a modification to its regulations to be consistent with Codification with respect

to the admissibility of deferred income taxes by New York insurers, subject to certain limitations. The adoption of the Codification as modified by the

Department, did not adversely affect Metropolitan Life’s statutory capital and surplus. Further modifications by state insurance departments may impact

the effect of the Codification on the statutory capital and surplus of Metropolitan Life and the Holding Company’s other insurance subsidiaries.

Liquidity Sources

Cash Flow from Operations. The Company’s principal cash inflows from its insurance activities come from insurance premiums, annuity considera-

tions and deposit funds. A primary liquidity concern with respect to these cash inflows is the risk of early contractholder and policyholder withdrawal. The

Company seeks to include provisions limiting withdrawal rights on many of its products, including general account institutional pension products

(generally group annuities, including guaranteed interest contracts and certain deposit fund liabilities) sold to employee benefit plan sponsors.

MetLife, Inc.

22