Kodak 2010 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2010 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

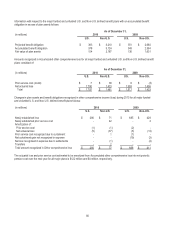

86

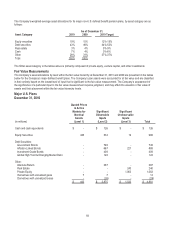

Major Non-U.S. Plans

December 31, 2009

(in millions)

Quoted Prices

in Active

Markets for

Identical

Assets

(Level 1)

Significant

Observable

Inputs

(Level 2)

Significant

Unobservable

Inputs

(Level 3)

Total

Cash and cash equivalents

$ -

$ 98

$ -

$ 98

Equity securities

71

312

-

383

Debt securities:

Government Bonds

-

526

-

526

Inflation-Linked Bonds

-

290

57

347

Investment Grade Bonds

-

107

-

107

Global High Yield & Emerging Market Debt

-

180

-

180

Other:

Absolute Return

-

78

-

78

Real Estate

-

4

99

103

Private Equity

-

2

242

244

Insurance Contracts

-

448

-

448

Derivatives with unrealized gains

-

3

-

3

Derivatives with unrealized losses

-

(15)

-

(15)

$ 71

$ 2,033

$ 398

$ 2,502

For the Company’s major non-U.S. defined benefit pension plans, equity investments are invested broadly in local equity, developed

international and emerging markets. Fixed income investments are comprised primarily of long duration government and corporate

bonds with some emerging market debt. Real estate investments include investments in primarily office, industrial, and retail

properties. Other investments include private equity, hedge funds, and insurance contracts. Private equity investments are

comprised of limited partnerships and fund-of-fund investments that invest in distressed investments, venture capital and leveraged

buyout funds. Absolute return investments are comprised of hedge funds that use equity long-short strategies.

Cash and cash equivalents are valued utilizing cost approach valuation techniques. Equity securities and debt securities are valued

using a market approach based on the closing price on the last business day of the year (if the securities are traded on an active

market), or based on the proportionate share of the estimated fair value of the underlying assets (net asset value). Other

investments are valued using a combination of market, income, and cost approaches, based on the nature of the investment.

Absolute return investments are primarily valued based on net asset value derived from observable market inputs. Real estate

investments are valued primarily based on independent appraisals and discounted cash flow models, taking into consideration

discount rates and local market conditions. Private equity investments are valued primarily based on independent appraisals,

discounted cash flow models, cost, and comparable market transactions, which include inputs such as discount rates and pricing

data from the most recent equity financing. Insurance contracts are primarily valued based on contract values, which approximate

fair value.

Some of the plans’ assets, primarily absolute return, real estate, and private equity, do not have readily determinable market values

due to the nature of these investments. For these investments, fund manager or general partner estimates were used where

available. The estimates for the absolute return assets are derived from observable inputs, based on the fair value of the underlying

positions, which have readily available market prices. For investments with lagged pricing, the Company used the available net asset

values, and also considered expected return, subsequent cash flows and material events.

For all of the Company’s major defined benefit pension plans, investment managers are selected that are expected to provide best-

in-class asset management for their particular asset class, and expected returns greater than those expected from existing salable

assets, especially if this would maintain the aggregate volatility desired for each plan’s portfolio. Investment managers are retained

for the purpose of managing specific investment strategies within contractual investment guidelines. Certain investment managers

are authorized to invest in derivatives such as futures, swaps, and currency forward contracts. Investments in futures and swaps are

used to obtain targeted exposure to a particular asset, index or bond duration and only require a portion of the cash to gain exposure