Chrysler 2004 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2004 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

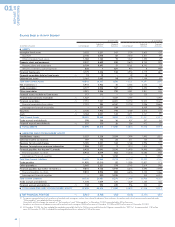

49

the receivables retained by the seller is therefore limited to

the junior securities it has subscribed for.

Factoring transactions may be with or without recourse on

the seller; certain factoring agreements without recourse include

deferred purchase price clauses (i.e. the payment of a minority

portion of the purchase price is conditional upon the full

collection of the receivables), require a first loss guarantee

of the seller up to a limited amount or imply a continuing

significant exposure to the receivables cash flow.

According to Italian GAAP, all receivables sold through either

securitization or factoring transactions (both with and without

recourse) have been derecognized. Furthermore, with specific

reference to the securitization of retail loans and leases

originated by the financial services companies, the net present

value of the interest flow implicit in the installments, net of

related costs, has been recognized in the income statement.

Under IFRS:

■As mentioned above, SIC 12 Special Purpose Entities stated

that an SPE shall be consolidated when the substance of the

relationship between the entity and the SPE indicates that the

SPE is controlled by that entity: all securitization transactions

will be therefore reversed, because the subscription of the

junior asset-backed securities by the seller entails its control

in substance over the SPE.

■IAS 39 allows for the derecognition of a financial asset when,

and only when, the risks and rewards of the ownership of the

assets are substantially transferred: consequently, all portfolios

sold with recourse, and the majority of those sold without

recourse, since risks and rewards have not been substantially

transferred, will be reinstated in the IFRS balance sheet.

The impact of such adjustments on the stockholders’ equity

and on the net income will be not material.

R. ACCOUNTING FOR DEFERRED INCOME TAXES

This adjustment will include the combined effect of the net

deferred tax effects, after allowance, on the above mentioned

IFRS adjustments, as well as other minor differences between

Italian GAAP and IFRS on the recognition of tax assets and

liabilities.

Transition to International Financial Reporting Standards (IAS/IFRS)