Capital One 2004 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2004 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

and expected reported charge-off and delinquency rates, as well as expected reported loan growth, a higher

growth rate in its diversification businesses than its U.S. Card business, and a continuation of current economic

conditions. This outlook is sensitive to general economic conditions, employment trends, and bankruptcy trends,

in addition to growth of the Company’s reported loans.

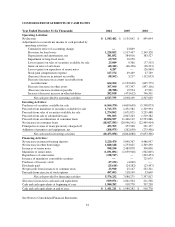

Managed Return on Assets

The Company expects that its managed return on assets will be between 1.7 and 1.8 percent for the full year of

2005, with some quarterly variability.

The Company’s Core Strategy: IBS

The Company’s core strategy has been, and is expected to continue to be, to apply its proprietary IBS to its

consumer lending businesses and other financial products. The Company continues to seek to identify new

product and new market opportunities, and to make investment decisions based on the Company’s intensive

testing and analysis. The Company’s objective is to continue diversifying its consumer finance activities, which

may include expansion into additional geographic markets, other consumer loan products (including home loan

lending and installment lending), small business lending, and/or the branch banking business.

The Company’s lending products and other products are subject to intense competitive pressures that

management anticipates will continue to increase as the lending markets mature, and it could affect the

economics of decisions that the Company has made or will make in the future in ways that it did not anticipate,

test or analyze.

U.S. Card Segment

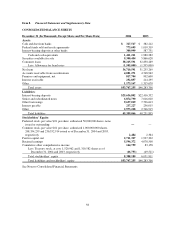

The Company’s U.S. Card segment consisted of $48.6 billion of U.S. consumer credit card loans as of

December 31, 2004, marketed to consumers across the full credit spectrum. The Company’s strategy for its U.S.

Card segment is to offer compelling, value-added products to its customers. The Company expects balanced

growth across the various credit risk segments of its credit card portfolio in 2005.

The competitive environment is currently intense for credit card products. Industry mail volume has increased

substantially in recent years, resulting in declines in response rates to the Company’s new customer solicitations

over time. Additionally, the increase in other consumer loan products, such as home equity loans, has put

pressure on growth throughout the credit card industry. These competitive pressures are continuing to increase

due to, among other things, increasing consolidation within the industry. Despite this intense pressure, the

Company continues to believe that its IBS capabilities will enable it to originate new credit card accounts that

exceed the Company’s return on investment requirements and to generate a loan growth rate in excess of the

industry growth rate.

The Company’s credit card products marketed to consumers with less established or higher risk credit profiles

continue to experience steady mail volume and increased pricing competition from across the industry. These

products generally feature higher annual percentage rates, lower credit lines, and annual membership fees. These

products produce revenues more quickly than higher credit quality loans. Additionally, since these borrowers are

generally viewed as higher risk, they tend to be more likely to pay late or exceed their credit limit, which results

in additional fees assessed to their accounts. The Company’s strategy has been, and is expected to continue to be,

to offer competitive annual percentage rates and annual membership fees on these accounts.

Auto Finance Segment

The Company’s Auto Finance segment consisted of $10.0 billion of U.S. auto loans as of December 31, 2004,

marketed across the full credit spectrum, via direct and dealer marketing channels. The Company sold $901.3

million of auto finance receivables in 2004. The Company plans to continue to sell auto receivables in 2005.

56