Capital One 2004 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2004 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

A number of factors could make such financing more difficult, more expensive or unavailable on any terms both

domestically and internationally (where funding transactions may be on terms more or less favorable than in the

United States), including, but not limited to, financial results and losses, changes within our organization,

specific events that adversely impact our reputation, changes in the activities of our business partners, disruptions

in the capital markets, specific events that adversely impact the financial services industry, counter-party

availability, changes affecting our assets, our corporate and regulatory structure, interest rate fluctuations, ratings

agencies actions, general economic conditions and the legal, regulatory, accounting and tax environments

governing our funding transactions. In addition, our ability to raise funds is strongly affected by the general state

of the U.S. and world economies, and may become increasingly difficult due to economic and other factors. Also,

we compete for funding with other banks, savings banks and similar companies, some of which are publicly

traded. Many of these institutions are substantially larger, have more capital and other resources and have better

debt ratings than we do. In addition, as some of these competitors consolidate with other financial institutions,

these advantages may increase. Competition from these institutions may increase our cost of funds.

In addition, we are substantially dependent on the securitization of consumer loans, which involves the legal sale

of beneficial interests in consumer loan balances and is a unique funding market. Despite the size and relative

stability of these markets and our position as a leading issuer, if these markets experience difficulties we may be

unable to securitize our loan receivables or to do so at favorable pricing levels. If we were unable to continue to

securitize our loan receivables at current levels, we would use alternative funding sources to fund increases in

loan receivables and meet our other liquidity needs. If we were unable to find cost-effective and stable

alternatives, it could negatively impact our liquidity and potentially subject us to certain risks. These risks would

include an increase in our cost of funds, an increase in the allowance for loan losses and the provision for

possible credit losses as more loans would remain on our consolidated balance sheet, and lower loan growth.

In addition, the occurrence of certain events may cause the securitization transactions to amortize earlier than

scheduled, which would accelerate the need for additional funding. This early amortization could, among other

things, have a significant effect on the ability of the Bank and the Savings Bank to meet the capital adequacy

requirements as all off-balance sheet loans experiencing such early amortization would have to be recorded on

the balance sheet. See pages 49-51 in Item 7 “Management’s Discussion and Analysis of Financial Condition and

Results of Operations—Liquidity Risk Management” contained in the Corporation’s Annual Report on

Form 10-K for the year ended December 31, 2004.

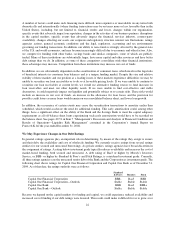

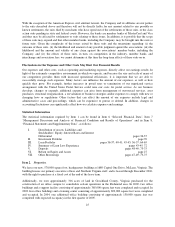

We May Experience Changes in Our Debt Ratings

In general, ratings agencies play an important role in determining, by means of the ratings they assign to issuers

and their debt, the availability and cost of wholesale funding. We currently receive ratings from several ratings

entities for our secured and unsecured borrowings. As private entities, ratings agencies have broad discretion in

the assignment of ratings. A rating below investment grade typically reduces availability and increases the cost of

market-based funding, both secured and unsecured. A debt rating of Baa3 or higher by Moody’s Investors

Service, or BBB- or higher by Standard & Poor’s and Fitch Ratings, is considered investment grade. Currently,

all three ratings agencies rate the unsecured senior debt of the Bank and the Corporation as investment grade. The

following chart shows ratings for Capital One Financial Corporation and Capital One Bank as of December 31,

2004. As of that date, the ratings outlooks were as follows:

Standard

& Poor’s Moody’s Fitch

Capital One Financial Corporation BBB- Baa3 BBB

Capital One Financial Corporation—Outlook Stable Stable Stable

Capital One Bank BBB Baa2 BBB+

Capital One Bank—Outlook Stable Stable Stable

Because we depend on the capital markets for funding and capital, we could experience reduced availability and

increased cost of funding if our debt ratings were lowered. This result could make it difficult for us to grow at or

22