Capital One 2004 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2004 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

Note 20

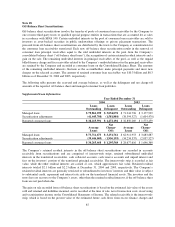

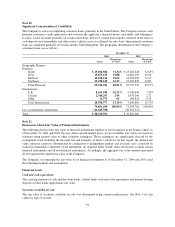

Significant Concentration of Credit Risk

The Company is active in originating consumer loans, primarily in the United States. The Company reviews each

potential customer’s credit application and evaluates the applicant’s financial history and ability and willingness

to repay. Loans are made primarily on an unsecured basis; however, certain loans require collateral in the form of

cash deposits and automobiles and other motor vehicles serve as collateral for auto loans. International consumer

loans are originated primarily in Canada and the United Kingdom. The geographic distribution of the Company’s

consumer loans was as follows:

December 31

2004 2003

Loans

Percentage

of Total Loans

Percentage

of Total

Geographic Region:

Domestic

South $ 25,034,582 31.34% $ 23,262,643 32.65%

West 15,873,159 19.88 14,662,193 20.58

Midwest 15,220,162 19.06 13,643,202 19.15

Northeast 13,198,619 16.53 12,029,894 16.89

Total Domestic 69,326,522 86.81% 63,597,932 89.27%

International

U.K. 8,163,109 10.22% 5,546,644 7.78%

Canada 2,360,297 2.96 1,935,396 2.72

Other 11,371 .01 164,824 0.23

Total International 10,534,777 13.19% 7,646,864 10.73%

79,861,299 100.00% 71,244,796 100.00%

Less securitization adjustments (41,645,708) (38,394,527)

Total $ 38,215,591 $ 32,850,269

Note 21

Disclosures About Fair Value of Financial Instruments

The following discloses the fair value of financial instruments whether or not recognized in the balance sheets as

of December 31, 2004 and 2003. In cases where quoted market prices are not available, fair values are based on

estimates using present value or other valuation techniques. Those techniques are significantly affected by the

assumptions used, including the discount rate and estimates of future cash flows. In that regard, the derived fair

value estimates cannot be substantiated by comparison to independent markets and, in many cases, could not be

realized in immediate settlement of the instrument. As required under GAAP, these disclosures exclude certain

financial instruments and all non-financial instruments. Accordingly, the aggregate fair value amounts presented

do not represent the underlying value of the Company.

The Company, in estimating the fair value of its financial instruments as of December 31, 2004 and 2003, used

the following methods and assumptions:

Financial Assets

Cash and cash equivalents

The carrying amounts of cash and due from banks, federal funds sold and resale agreements and interest-bearing

deposits at other banks approximate fair value.

Securities available for sale

The fair value of securities available for sale was determined using current market prices. See Note 3 for fair

values by type of security.

92