Capital One 2004 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2004 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

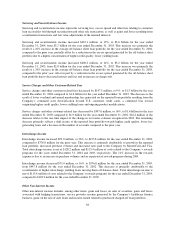

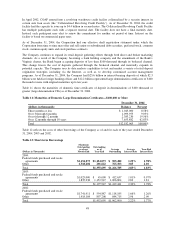

The Global Financial Services segment’s net charge-off rate was 3.39% for 2004, down 44 basis points when

compared with the prior year. Net charge-offs increased $99.1 million, or 19% during 2004 while average Global

Financial Services segment loans grew $4.7 billion, or 34%. The decrease in the net charge-off rate was driven

primarily by a bias toward originating higher credit quality loans within the Global Financial Services segment,

improved collection experience and an overall improvement in economic conditions.

The 30-plus day delinquency rate for the Global Financial Services segment was 2.81% at December 31, 2004,

up 11 basis points from 2.70% at December 31, 2003. Global Financial Services delinquencies increased

primarily as a result of an expansion of the international loan portfolio during 2004.

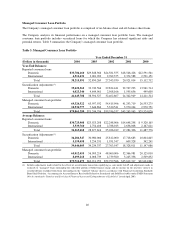

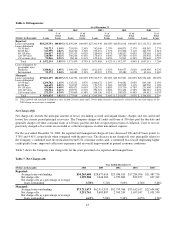

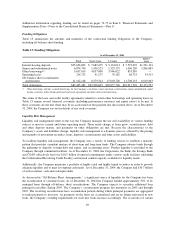

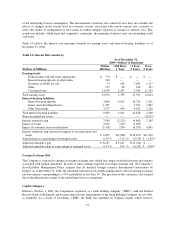

Funding

Funding Availability

The Company has established access to a variety of funding alternatives in addition to securitization of its

consumer loans. Table 10 illustrates the Company’s unsecured funding sources.

Table 10: Funding Availability

(Dollars or dollar equivalents in millions)

Effective/

Issue Date Availability(1)(5) Outstanding

Final

Maturity(4)

Senior and Subordinated Global Bank Note

Program(2) 1/03 $1,800 $4,877 —

Senior Domestic Bank Note Program(3) 4/97 — $ 232 —

Credit Facility 6/04 $ 750 — 6/07

Collateralized Revolving Credit Facility — $4,153 $ 197 —

Corporation shelf registration 7/02 $1,948 N/A —

(1) All funding sources are non-revolving except for the Credit Facility and the Collateralized Revolving Credit Facility. Funding

availability under the credit facilities is subject to compliance with certain representations, warranties and covenants. Funding availability

under all other sources is subject to market conditions.

(2) The notes issued under the Global Senior and Subordinated Bank Note Program may have original terms of thirty days to thirty years

from their date of issuance. This program was updated in April 2004.

(3) The notes issued under the Senior Domestic Bank Note Program have original terms of one to ten years. The Senior Domestic Bank Note

Program is no longer available for issuances.

(4) Maturity date refers to the date the facility terminates, where applicable.

(5) Availability does not include unused conduit capacity related to securitization structures of $5.5 billion at December 31, 2004.

The Senior and Subordinated Global Bank Note Program gives the Bank the ability to issue securities to both

U.S. and non-U.S. lenders and to raise funds in U.S. and foreign currencies. The Senior and Subordinated Global

Bank Note Program had $4.9 billion outstanding at December 31, 2004. During 2004, under the Senior and

Subordinated Global Bank Note Program, the Bank issued $500.0 million of ten-year, 5.125% fixed rate bank

notes in February and $500.0 million of five-year, 5.00% fixed rate bank notes in June. Prior to the establishment

of the Senior and Subordinated Global Bank Note Program, the Bank issued senior unsecured debt through its

$8.0 billion Senior Domestic Bank Note Program, of which $231.6 million was outstanding at December 31,

2004. The Bank did not renew the Senior Domestic Bank Note Program for future issuances following the

establishment of the Senior and Subordinated Global Bank Note Program.

In June 2004, the Company terminated its Domestic Revolving and Multicurrency Credit Facilities and replaced

them with a new revolving credit facility providing for an aggregate of $750.0 million in unsecured borrowings

from various lending institutions to be used for general corporate purposes (the “Credit Facility”). The Credit

Facility is available to the Corporation, the Bank, the Savings Bank and Capital One Bank (Europe) plc. The

Corporation’s availability has been increased to $500.0 million under the Credit Facility. All borrowings under

the Credit Facility are based on varying terms of London InterBank Offering Rate (“LIBOR”).

47