APS 2012 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2012 APS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

PINNACLE WEST CAPITAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

117

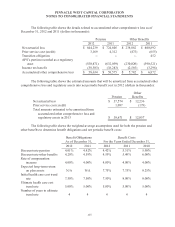

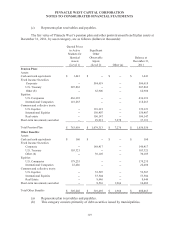

Based on the IPS, and given the pension plan’s funded status at year-end 2012, the long-term

fixed income assets and the return generating assets each had a target allocation of 50%. The return-

generating assets have additional target allocations, as a percent of total plan assets, of 30% equities in

U.S. and other developed markets, 6% equities in emerging markets, and 14% in alternative

investments. The pension plan IPS does not provide for a specific mix of long-term fixed income

assets, but does expect the average credit quality of such assets to be investment grade. As of

December 31, 2012, long-term fixed income assets represented 44% of total pension plan assets, and

return-generating assets represented 56% of total pension plan assets.

The asset allocation for other postretirement benefit plan assets is governed by the IPS for those

plans, which provides for an asset allocation target mix of at least 25% of fixed income assets and 55%

or less of non-fixed income assets. This asset allocation target mix does not vary with the plan’s funded

status. As of December 31, 2012, investment in fixed income assets represented 45% of the other

postretirement benefit plan total assets, and non-fixed income assets represent 55% of the other

postretirement benefit plan’s assets. Fixed income assets are primarily invested in corporate bonds of

investment-grade U.S. issuers, and U.S. Treasuries. Non-fixed income assets are primarily invested in

large cap U.S. equities in diverse industries, and international equities in both emerging and developed

markets.

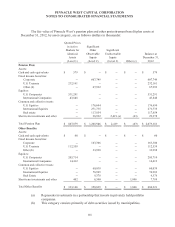

See Note 14 for a discussion on the fair value hierarchy and how fair value methodologies are

applied. The plans invest directly in fixed income and equity securities, in addition to investing

indirectly in equity securities and real estate through the use of common and collective trusts. Equity

securities held directly by the plans are valued using quoted active market prices from the published

exchange on which the equity security trades, and are classified as Level 1. Fixed income securities

issued by the U.S. Treasury held directly by the plans are valued using quoted active market prices, and

are classified as Level 1. Fixed income securities issued by corporations, municipalities, and other

agencies are primarily valued using quoted inactive market prices, or quoted active market prices for

similar securities, or by utilizing calculations which incorporate observable inputs such as yield,

maturity and credit quality. These instruments are classified as Level 2.

The common and collective trusts, which are similar to mutual funds, are maintained by banks

or investment companies and hold certain investments in accordance with a stated set of objectives

(such as tracking the performance of the S&P 500 index). The common and collective equity trusts are

valued using the concept of net asset value (“NAV”), which is a value derived from the quoted active

market prices of the underlying securities. The plans’ common and collective real estate trust is valued

using NAV, which is derived from the appraised values of the trust’s underlying real estate assets. As

of December 31, 2012 the plans were able to transact in the common and collective trusts at NAV and

accordingly classify these investments as Level 2. Because the trust’s shares are offered to a limited

group of investors, they are not considered to be traded in an active market.

The plans’ trustee provides valuation of our plan assets by using pricing services that utilize

methodologies described to determine fair market value. We have internal control procedures to ensure

this information is consistent with fair value accounting guidance. These procedures include assessing

valuations using an independent pricing source, verifying that pricing can be supported by actual recent

market transactions, assessing hierarchy classifications, comparing investment returns with benchmarks,

and obtaining and reviewing independent audit reports on the trustee’s internal operating controls and

valuation processes.