ICICI Bank 2006 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2006 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

48

Management’s Discussion & Analysis

The Bank enters into foreign exchange forward contracts, options, swaps and other derivative products

to enable customers to transfer, modify or reduce their foreign exchange and interest rate risk and to

manage its own interest rate and foreign exchange positions. These instruments are used to manage

foreign exchange and interest rate risk relating to specific groups of on-balance sheet assets and liabilities.

The notional principal amount of interest rate swaps, currency options and interest rate futures increased

by 62.7% to Rs. 2,471.92 billion at March 31, 2006 compared to Rs. 1,519.22 billion at March 31, 2005.

This significant increase is primarily due to increased transactions carried out by the Bank on behalf of its

customers and growth in the market for such products. As an active player and market-maker in swap

and forward exchange contract markets and due to the fact that reduction in positions is generally achieved

by entering into offsetting transactions rather than termination / cancellation of existing transactions, the

bank has seen a substantial increase in the notional principal of its swap portfolio during this period.

An interest rate swap does not entail exchange of notional principal and the cash flow arises on account

of the difference between the interest rate pay and receive legs of the swap which is generally much

lower than the notional principal of the swap. A large proportion of the Bank’s interest rate swap, currency

swaps and forward exchange contracts are on account of market making which involves providing regular

two-way prices to customers or inter-bank counter parties. This results in generation of a higher number

of outstanding transactions, and hence a large value of gross notional principal of the portfolio.

Guarantees

As a part of its project financing and commercial banking activities, the Bank has issued guarantees to

enhance the credit standing of its customers. These generally represent irrevocable assurances that the

Bank will make payments in the event that the customer fails to fulfill its financial or performance obligations.

Financial guarantees are obligations to pay a third party beneficiary where a customer fails to make

payment towards a specified financial obligation. Performance guarantees are obligations to pay a third

party beneficiary where a customer fails to perform a non-financial contractual obligation. The guarantees

are generally for a period not exceeding 10years.

The credit risks associated with these products, as well as the operating risks, are similar to those relating

to other types of financial instruments.

The Bank has collateral available to reimburse potential losses on its guarantees. Margins available to

reimburse losses realized under guarantees amounted to Rs. 10.29billion at March 31, 2006 compared

to Rs. 4.06 billion at March 31, 2005. Other property or security may also be available to the Bank to cover

losses under guarantees.

Capital Commitments

The Bank is obligated under a number of capital contracts. Capital contracts are job orders of a capital

nature which have been committed. As of the balance sheet date, work had not been completed to this

extent. Estimated amounts of contracts remaining to be executed on capital account aggregated Rs. 1.13

billion at March 31, 2006 compared to Rs. 0.70billion at March 31, 2005.

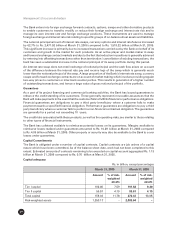

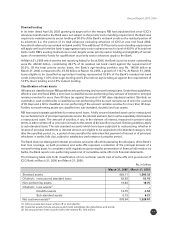

Capital adequacy

Rs. in billion, except percentages

March 31, 2005 March 31, 2006

Amount % of risk- Amount % of risk-

weighted weighted

assets assets

Tier I capital 102.46 7.59 191.82 9.20

Tier II capital 56.57 4.19 86.61 4.15

Total capital 159.03 11.78 278.43 13.35

Risk-weighted assets 1,350.17 – 2,085.94 –