ICICI Bank 2006 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2006 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137

|

|

F76

by Insurance Enterprises for Certain Long-Duration Contracts and for Realized Gains and Losses from the

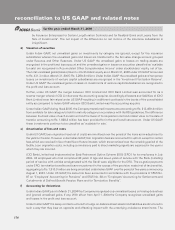

Sale of Investments”. The net impact of the differences on net income of the insurance subsidiaries is

insignificant.

d) Valuation of securities

Under Indian GAAP, net unrealised gains on investments by category are ignored, except for the insurance

subsidiaries wherein the unrealised gains and losses are transferred to the fair value change account grouped

under Revenue and Other Reserves. Under US GAAP the unrealised gains or losses on trading assets are

recognised in the profit and loss account and the unrealised gains or losses on securities classified as ‘available

for sale’ are recognised in ‘Accumulated Other Comprehensive Income’ under stockholders’ equity, net of tax.

The total unrealised gains/(losses) taken to stockholders’ equity as on March 31, 2006 under US GAAP amounted

to Rs. 431.3 million (March 31, 2005: Rs. 3,289.2 million). Under Indian GAAP the unrealised gains and temporary

losses on investments of venture capital subsidiaries are recognised in the ‘Investment Fluctuation Reserve’.

Under US GAAP the unrealised gains or losses on investments of venture capital subsidiaries are recognised in

the profit and loss account.

Further, under US GAAP the merger between ICICI Limited and ICICI Bank Limited was accounted for as a

reverse merger wherein ICICI Limited was the accounting acquirer. Accordingly all assets and liabilities of ICICI

Bank Limited were fair valued under US GAAP resulting in a different cost basis in the books of the consolidated

entity as compared to Indian GAAP wherein ICICI Bank Limited was the accounting acquirer.

Under Indian GAAP, during fiscal 2005, the Company transferred investments amounting to Rs. 213,489.4 million

from available for sale category to held to maturity category in accordance with the RBI guidelines. The difference

between the book value of each investment and the lower of its acquisition cost and market value on the date of

transfer, amounting to Rs. 1,828.2 million has been provided for in the profit and loss account. Under US GAAP,

these investments continue to be classified as ‘available for sale’.

e) Amortisation of fees and costs

Under US GAAP, loan origination fees (net of costs) are amortised over the period of the loans as an adjustment to

the yield on the loan. However under Indian GAAP, loan origination fees are accounted for upfront except for certain

fees which are received in lieu of sacrifice of future interest, which are amortised over the remaining period of the

facility. Loan origination costs, including commissions paid to direct marketing agents are expensed in the year in

which they are incurred.

ICICI Bank Limited had implemented an Early Retirement Option Scheme 2003 (‘ERO’) for its employees in July

2003. All employees who had completed 40 years of age and seven years of service with the Bank (including

period of service with entities amalgamated with the Bank) were eligible for the ERO. The ex-gratia payments

under ERO, termination benefits and leave encashment in the excess of the provision made (net of tax benefits),

aggregating to Rs. 1,910.0 million are being amortised under Indian GAAP over the period of five years commencing

August 1, 2003. Under US GAAP, the same has been accounted in accordance with the provisions of SFAS No.

87 on “Employers’ Accounting for Pensions” and SFAS No. 88 on “Employers’ Accounting for Settlements and

Curtailments of Defined Benefit Pension Plans and for Termination Benefits”.

f) Accounting for derivatives

Under Indian GAAP, prior to March 31, 2004 the Company recognised only unrealised losses on trading derivatives

and ignored unrealised gains, if any. With effect from April 1, 2004 the Company recognises unrealised gains

and losses in the profit and loss account.

Under Indian GAAP the swap contracts entered to hedge on-balance sheet assets and liabilities are structured in

such a way that they bear an opposite and offsetting impact with the underlying on-balance sheet items. The

reconciliation to US GAAP and related notes

for the year ended March 31, 2006