ICICI Bank 2006 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2006 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

F58

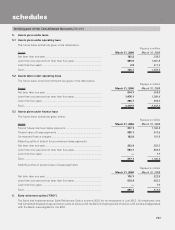

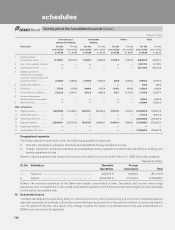

In case of the housing finance subsidiary, loans and other credit facilities are classified as per the NHB guidelines into

performing and non-performing assets. Further, NPAs are classified into sub-standard, doubtful and loss assets based on

criteria stipulated by NHB.

In the case of the Canadian subsidiary, loans are stated net of allowance for credit losses. Loans are classified as impaired

when there is no longer reasonable assurance of the timely collection of the full amount of principal or interest. An allowance

for credit losses is maintained at a level that management considers adequate to absorb identified credit related losses as

well as losses that have been incurred but are not yet identifiable.

15. Transfer and servicing of financial assets

The Company transfers commercial and consumer loans through securitisation transactions. The transferred loans are de-

recognised and gains / losses are recorded only if the Company surrenders the rights to benefits specified in the loan

contract. Recourse and servicing obligations are reduced from proceeds of the sale. Retained beneficial interests in the

loans are measured by allocating the carrying value of the loans between the assets sold and the retained interest, based

on the relative fair value at the date of the securitisation.

During the year, RBI has issued specific guidelines on securitisation of standard assets. Accordingly, with effect from

February 1, 2006, the Bank accounts for any loss arising on securitisation in the profit & loss account immediately at the

time of securitisation. Profit / premium, if any, arising on account of securitisation is amortised over the life of the securities

issued or to be issued by the Special Purpose Vehicle (SPV).

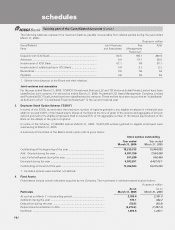

16. Fixed assets and depreciation

Premises and other fixed assets are carried at cost less accumulated depreciation. Depreciation is charged over the estimated

useful life of a fixed asset on a straight-line basis, except for those relating to venture capital, investment banking and asset

management subsidiaries where depreciation is charged on a written down value basis. The rates of depreciation for fixed

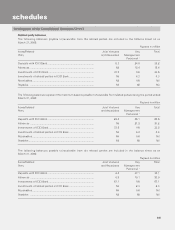

assets, which are not lower than the rates prescribed in Schedule XIV of the Companies Act, 1956, are given below:

Asset Depreciation rate

Premises owned by the Bank ......................................................................................................................................... 1.63%

ATMs ............................................................................................................................................................................. 12.50%

Plant and machinery like air conditioners, xerox machines, etc. ................................................................................. 10.00%

Furniture and fixtures .................................................................................................................................................... 15.00%

Motor vehicles .............................................................................................................................................................. 20.00%

Computers .................................................................................................................................................................... 33.33%

EDC terminals ............................................................................................................................................................... 16.67%

Others (including software and system development expenses) ............................................................................... 25.00%

Cost comprises the purchase price and any cost attributable to bring the asset to working condition for its intended use.

Depreciation on leased assets and improvement to leasehold premises is made on a straight-line basis at the higher of the

rates determined with reference to the primary period of lease and the rates specified in Schedule XIV of the Companies

Act, 1956.

Assets purchased/sold during the year are depreciated on the basis of actual number of days the asset has been put to use.

Items costing less than Rs. 5,000 are depreciated fully over a period of 12 months from the date of purchase.

In case of the venture capital subsidiary depreciation on assets, other than leased assets, is charged on written down value

method at the rates and in the manner prescribed under Schedule XIV to the Companies Act, 1956.

In case of investment banking subsidiary, depreciation on assets, other than improvements to leased property and membership

rights of The Stock Exchange, Mumbai, is charged on written down value method at the rates which are greater than or

equal to the provisions of Schedule XIV of the Companies Act, 1956. A membership right of the stock exchange is treated

as an asset and the value paid to acquire such rights is amortised over a period of 10 years.

schedules

forming part of the Consolidated Accounts (Contd.)