HSBC 2008 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

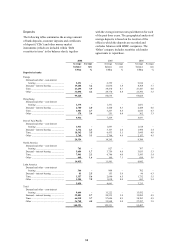

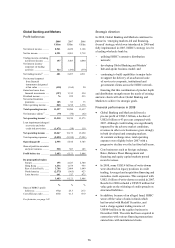

69

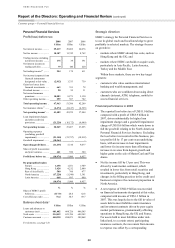

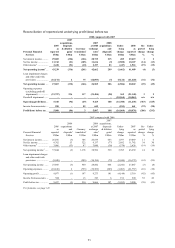

reduction in policyholder liabilities where

investment losses can be passed to

policyholders.

• Loan impairment charges rose by 32 per cent,

primarily due to further deterioration in credit

quality in the North American Personal

Financial Services business. Delinquency rates

increased across all portfolios in HSBC Finance,

particularly consumer lending, and in the real

estate secured portfolios in HSBC USA,

following the sustained downturn in the housing

market and the onset of economic recession.

• A rise in loan impairments in Mexico,

Turkey and India was attributable to higher

delinquencies following growth of the credit

card and personal loan portfolios. Actions taken

to curtail asset growth in these markets focused

on tightening lending criteria and deploying

advanced credit analytics.

• Operating expenses were 48 per cent higher,

largely due to the goodwill impairment charge.

Excluding this, operational costs were slightly

lower, driven by a 12 per cent reduction in

North America following initiatives taken since

2007 to cease originations in mortgage services,

limit new originations in consumer lending and

reduce marketing spend in cards. This benefit

was partially offset by investment in business

expansion in mainland China and Japan and an

increase in restructuring costs and union-agreed

salaries in Latin America.

• Profit before tax increased in Europe, with a

solid performance in the UK partially offset by a

fall in Turkey as an investment in 98 additional

branches was made in order to attain nationwide

coverage. Profits were lower in France.

• In the Middle East, profit rose by 17 per cent on

2007, with strong growth in revenue from cards.

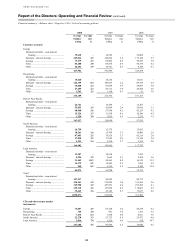

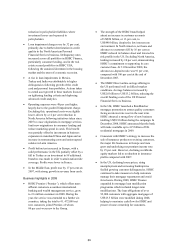

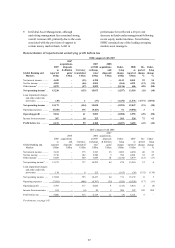

Business highlights in 2008

• HSBC Premier (‘Premier’), which offers mass

affluent customers a seamless international

banking and wealth management service, grew

to 2.6 million customers in 2008. During the

year, the service was extended to a further six

countries, taking the total to 41. 472,000 net

new customers joined Premier, of whom

80 per cent were new to the Group.

• The strength of the HSBC brand helped

attract an increase in customer accounts

of US$50 billion, or 13 per cent, to

US$440 billion, despite the low interest rate

environment. In North America, net loans and

advances to customers fell by 16 per cent as

HSBC reduced its balance sheet and lowered its

risk profile in the US. Excluding North America,

lending increased by 10 per cent, demonstrating

HSBC’s commitment to supporting its core

customer base. At 31 December 2008, the

advances-to-deposits ratio was 91 per cent,

compared with 106 per cent at the end of

December 2007.

• The HSBC Direct online savings offering in

the US performed well in difficult market

conditions. Average balances increased by

US$2.0 billion to US$13.2 billion, reducing the

overall funding costs of the US Personal

Financial Services business.

• In the UK, HSBC launched a RateMatcher

mortgage promotion to attract quality customers

facing an interest rate reset in the near term.

HSBC attracted a strong flow of new business

totalling US$9.9 billion during the campaign. In

December 2008, HSBC announced that the bank

will make available up to £15 billion of UK

residential mortgages in 2009.

• Consistent with HSBC’s strategy to increase the

sale of insurance products to existing customers,

the major life businesses in Europe and Asia

grew and underlying net premium income rose

by 15 per cent. However, declining worldwide

equity markets led to a reduction in insurance

profits compared with 2007.

• In the US, declining house prices, rising

unemployment and increasing bankruptcies

fuelled growing customer delinquencies. HSBC

continued to take measures to help customers

manage their mortgage repayments and avoid

foreclosure. During 2008, HSBC Finance

expanded its mortgage loan modification

programme which included longer-term

modifications. The loan obligations of over

92,000 customers with aggregate mortgages of

US$13.5 billion were modified during 2008,

helping to maximise cash flow for HSBC and

preserve home ownership for customers.