HSBC 2008 Annual Report Download - page 407

Download and view the complete annual report

Please find page 407 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

405

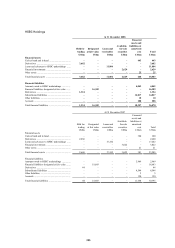

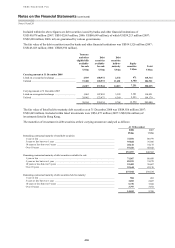

The following table provides an analysis of contractual maturities and weighted average yields of investment debt

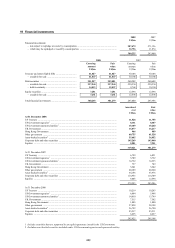

securities as at 31 December 2008:

Within one year

After one year but

within five years

After five years but

within ten years After ten years

Amount Yield Amount Yield Amount Yield Amount Yield

US$m % US$m % US$m % US$m %

Available-for-sale

US Treasury ................................... 41 2.44 1,049 1.14 225 1.89 985 4.52

US Government agencies .............. – – 15 6.67 298 5.03 7,324 3.74

US Government-sponsored

agencies ..................................... 760 4.61

569 6.68

1,398 3.15

10,466 4.70

UK Government ............................. – – 446 2.47

– –

1,385 3.25

Hong Kong Government ............... 136 2.21 15 2.84 186 4.84

– –

Other governments ......................... 20,604 3.30 17,182 6.00 3,609 4.56 2,493 3.38

Asset-backed securities .................. 1,088 1.57 2,626 1.87 6,021 2.34 45,765 2.04

Corporate debt and other

securities .................................... 49,065 4.28

68,760 3.53

12,460 3.76

3,648 4.22

Total amortised cost ....................... 71,694 90,662 24,197 72,066

Total carrying value ....................... 71,967 89,931 22,402 53,644

Held-to-maturity

US Treasury ................................... – – 30 3.45 42 4.76 44 4.55

US Government agencies .............. – – – – 6 8.81 487 6.37

US Government-sponsored

agencies ..................................... – –

44 4.76

38 7.89

1,845 5.88

Hong Kong Government ............... 19 5.26 – – – –

– –

Other governments ......................... 148 4.73 149 4.70 301 4.32 532 6.58

Asset-backed securities .................. – – – – – – 185 5.95

Corporate debt and other

securities .................................... 417 3.84

3,670 4.28

5,352 4.58

704 4.83

Total amortised cost ....................... 584 3,893 5,739 3,797

Total carrying value ....................... 584 3,893 5,739 3,797

The maturity distributions of asset-backed securities are presented in the above table based upon contractual maturity

dates. The weighted average yield for each range of maturities in the above table is calculated by dividing the

annualised interest income for the year ended 31 December 2008 by the book amount of available-for-sale debt

securities at that date. The yields do not include the effect of related derivatives.

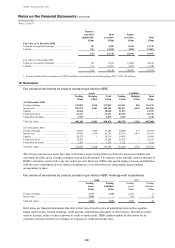

20 Transfers of financial assets not qualifying for de-recognition

HSBC enters into transactions in the normal course of business by which it transfers recognised financial assets

directly to third parties or to SPEs. These transfers may give rise to the full or partial derecognition of the financial

assets concerned.

– Full derecognition occurs when HSBC transfers its contractual right to receive cash flows from the financial

assets, or retains the right but assumes an obligation to pass on the cash flows from the asset, and transfers

substantially all the risks and rewards of ownership. The risks include credit, interest rate, currency, prepayment

and other price risks.

– Partial derecognition occurs when HSBC sells or otherwise transfers financial assets in such a way that some but

not substantially all of the risks and rewards of ownership are transferred but control is retained. These financial

assets are recognised on the balance sheet to the extent of HSBC’s continuing involvement.

The majority of financial assets that do not qualify for derecognition are (i) debt securities held by counterparties as

collateral under repurchase agreements or (ii) equity securities lent under securities lending agreements. The

following table analyses the carrying amount of financial assets that did not qualify for derecognition and their

associated financial liabilities: