HSBC 2008 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

113

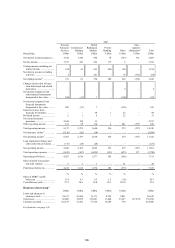

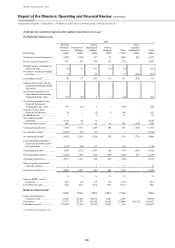

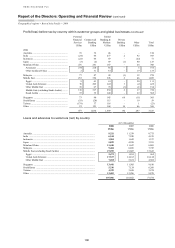

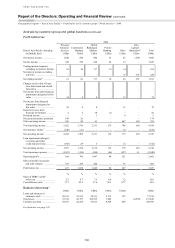

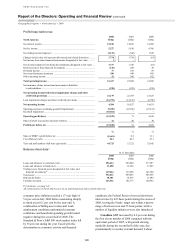

Growth in operating expenses at the Group

Service and Software Development Centres was

driven by increased volumes of activity as HSBC

continued to implement a global resourcing strategy

to minimise costs throughout the Group. All related

costs are recharged to other Group entities and the

income is reported within Other operating income.

Profit from associates and joint ventures in the

region increased by 12 per cent, notwithstanding a

significant impairment recorded in Ping An

Insurance in respect of its stake in Fortis Bank.

Growth was strong across HSBC’s other principal

associates, the Bank of Communications, Industrial

Bank, and the Saudi British Bank.

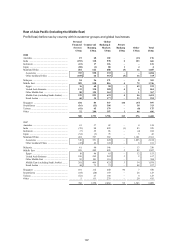

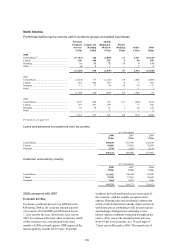

2007 compared with 2006

Economic briefing

Mainland China’s economy continued to grow

strongly, with GDP rising by 11.4 per cent in 2007,

the fifth consecutive year of double-digit growth;

this was despite a combination of measures aimed at

curbing investment, such as increases in interest

rates and reserve ratios required for banks. Economic

performance remained primarily dependent on

investment and exports. Bank loan growth also

remained very strong. Export growth slowed from

very high levels as the year progressed, reflecting the

mild downturn in global trade. Consumer spending

grew steadily in 2007, with retail sales rising by

about 16 per cent. Inflationary pressures increased,

with consumer price inflation exceeding 6 per cent

towards the end of the year, mainly due to higher

food prices. Mainland China’s foreign exchange

reserves rose further, to more than US$1.5 trillion,

while the renminbi appreciated by over 5 per cent

against the US dollar in 2007.

Japan’s economy, the largest in the region,

expanded modestly in 2007. Private capital

investment decelerated after five years of firm

growth but a rise in exports, especially to Asia,

drove overall growth. Private consumption also

made a positive contribution, helped by a gradual

increase in employees’ income. Core consumer price

inflation remained around zero throughout the course

of the year.

In the Middle East, economies continued to

grow, although growth rates slowed slightly on those

recorded in 2006, largely as a result of OPEC-

mandated cuts in oil production. Underlying

economic performance was robust, however, led by

continued non-oil sector growth. The catalyst for

expansion was a fifth consecutive year of rising oil

prices, which facilitated continued growth in public

and private investment. Consumption rose as

employment levels increased and low interest rates

supported an ongoing expansion in credit. Strong

population growth, accelerated in parts of the region

by high levels of immigration, also boosted demand

for credit. High oil revenues resulted in a further

year of fiscal and current account surpluses

throughout the Middle East, boosting reserves and

holdings of overseas assets. Rapid economic growth,

low interest rates and currency weakness increased

inflation, however, fuelling demands in some

quarters for adjustments to the long-standing dollar

pegs. Regional equity markets recovered from their

2005-06 downturns to perform strongly in 2007.

Elsewhere in the region, the Indian economy

expanded by 8.7 per cent in 2007, although there

was evidence that recent interest rate rises and the

strength of the rupee were slowing some areas of the

economy, and inflationary pressures eased in 2007.

The economies of Vietnam and Singapore recorded

strong performances too, expanding by 8.5 per cent

and 7.7 per cent, respectively in 2007. Growth was

approximately 6 per cent in Indonesia and Malaysia.

Domestic demand in all these countries has become

an increasingly important source of GDP growth

with investment, particularly in the construction

sector, expanding rapidly. Inflationary pressures

intensified in 2007, largely as a result of higher oil

and food prices, but remained under control. The

South Korean economy accelerated in 2007 as

exports continued to flourish and household

spending recovered from levels recorded in 2006.

Concerns over liquidity growth prompted the central

bank to increase interest rates by 50 basis points to

5 per cent during the year. A gradual cooling of

demand and concerns over rapid exchange rate

appreciation are expected to limit the scope for

further interest rate rises in 2008. Buoyant exports

supported economic growth in Taiwan, while

domestic demand remained lacklustre due to a lack

of government initiatives which is expected to

continue beyond the presidential and parliamentary

elections scheduled for 2008. Generally robust

economic performances in the Philippines, Thailand,

and Pakistan in 2007 were overshadowed to varying

degrees by political risks.