HSBC 2008 Annual Report Download - page 210

Download and view the complete annual report

Please find page 210 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

Report of the Directors: Risk (continued)

Credit risk > Areas of special interest > Personal lending

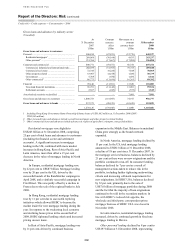

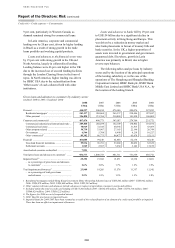

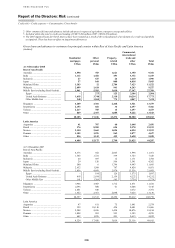

208

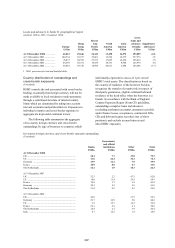

At 31 December 2008, HSBC had in-country

foreign currency and cross-border amounts

outstanding to counterparties in Japan of between

0.75 per cent and 1.0 per cent of total assets; in

aggregate, US$24.4 billion.

At 31 December 2007, HSBC had in-country

foreign currency and cross-border amounts

outstanding to counterparties in Hong Kong,

Belgium and Ireland of between 0.75 per cent and

1.0 per cent of total assets. The aggregate in-

country foreign currency and cross-border amounts

outstanding were Hong Kong, US$19.7 billion,

Belgium, US$19.3 billion and Ireland,

US$19.3 billion.

At 31 December 2006, HSBC had in-country

foreign currency and cross-border amounts

outstanding to counterparties in Australia and Hong

Kong of between 0.75 per cent and 1 per cent of

total assets. The aggregate in-country foreign

currency and cross-border amounts outstanding

were Australia, US$17.1 billion, Hong Kong,

US$13.9 billion.

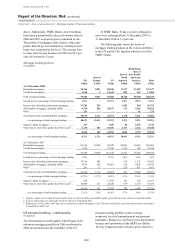

Areas of special interest

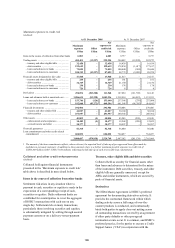

Personal lending

(Unaudited)

HSBC provides a broad range of secured and

unsecured personal lending products to meet

customer needs. Given the diverse nature of the

markets in which HSBC operates, the range is not

standardised across all countries but is tailored to

meet the demands of individual markets while

using appropriate distribution channels and,

wherever possible, common global IT platforms.

Personal lending includes advances to

customers for asset purchase, such as residential

property and motor vehicles, where the loans are

typically secured on the assets being acquired.

HSBC also offers loans secured on existing assets,

such as first and second liens on residential

property; unsecured lending products such as

overdrafts, credit cards and payroll loans; and debt

consolidation loans which may be secured or

unsecured. At the end of February 2009, HSBC

authorised the discontinuation as soon as

practicable of all new receivable originations of all

products by the branch-based consumer lending

business of HSBC Finance in North America (see

page 70).

Various underwriting controls are applied

before a loan is issued, and delinquency is managed

through collection and customer management

procedures. The expected occurrence and degree of

delinquency varies according to the type of loan

and the customer segment. Delinquency levels tend

to increase in the normal course of portfolio ageing.

As a result, loan impairment charges usually relate

to lending originated in earlier accounting periods.

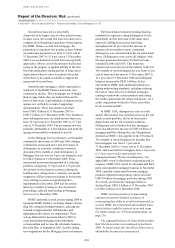

As discussed in ‘Challenges and uncertainties’

on page 12, rising unemployment has been the

major factor in the deterioration in credit quality of

personal lending portfolios in 2008. Further

weakening in consumers’ confidence and capacity

to service financial commitments may result in

deteriorating payment patterns and increased

delinquencies and default rates and, as a

consequence, higher loan impairment allowances

and write-offs. HSBC monitors the effect of these

factors on its personal lending portfolios and keeps

under review a range of measures designed to limit

the Group’s exposure and mitigate the effect on

customers.

Loan impairment allowances are sensitive to

changes in the level of unemployment, particularly

at the current time in North America, which affects

customers’ future ability to repay their loans. For

example, had there been an additional 1 per cent

increase in unemployment in North America, loan

impairment allowances could have been higher by

between US$0.7 billion and US$1.5 billion as at

31 December 2008. The relationship between

changes in unemployment and loan impairment

charges cannot be predicted with any degree of

certainty. For example, sharp increases in

unemployment may not have a linear impact on the

level of increase in loan impairment charges.

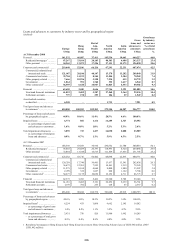

Please refer to page 205 for further analysis of

gross loans and advances by region and pages 34

and 229 for discussion of loan impairment charges

and other credit risk provisions.