HSBC 2008 Annual Report Download - page 258

Download and view the complete annual report

Please find page 258 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

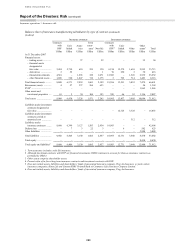

Report of the Directors: Risk (continued)

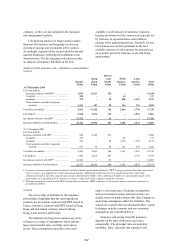

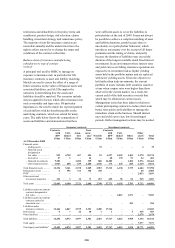

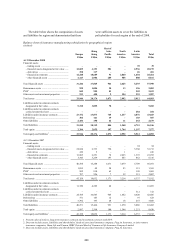

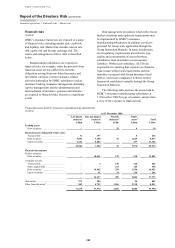

Insurance operations > Non-life business / Insurance risk

256

Non-life insurance business

(Audited)

Non-life insurance contracts include motor, fire and

other damage to property, accident and health,

repayment protection and commercial insurances.

Motor insurance business covers vehicle

damage and liability for personal injury. For fire and

other damage to property, the main focus in most

markets is providing individuals with home and

contents insurance, with cover for selected

commercial customers largely written in Asia and

Latin America.

A very limited portfolio of liability business is

written, other than that included in the motor book.

Credit non-life insurance is concentrated in

North America and Europe, and is originated in

conjunction with the provision of loans. Payment

protection insurance (‘PPI’) products were

suspended in the UK pending a final report from the

Competition Commission on their provision by the

financial services industry. The report was issued in

early 2009. The business is in the process of

assessing the impact of the reported findings on

credit protection products in the UK.

Given the nature of the contracts written by the

Group, the risks to which HSBC’s insurance

operations are exposed fall into two principal

categories: insurance risk and financial risk. The

following section describes the nature and extent of

these risks and HSBC’s approach to managing them.

The majority of the risk in the insurance business

derives from manufacturing activities.

Insurance risk

(Audited)

Insurance risk is a risk, other than financial risk,

transferred from the holder of a contract to the

issuer, in this case HSBC. The principal insurance

risk faced by HSBC is that, over time, the combined

cost of claims, administration and acquisition of the

contract may exceed the aggregate amount of

premiums received and investment income. The cost

of a claim can be influenced by many factors,

including mortality and morbidity experience, lapse

and surrender rates and, if the policy has a savings

element, the performance of the assets held to

support the liabilities. Performance of the underlying

assets is affected by changes in both interest rates

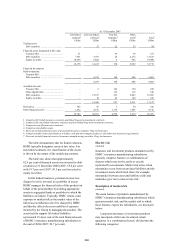

and equity prices (see page 263).

HSBC’s insurance risk appetite is proposed by

local businesses and authorised centrally. The Group

manages its exposure to insurance risk by applying

formal underwriting, reinsurance and claims-

handling procedures designed to ensure compliance

with regulations. This is supplemented with stress

testing.

Insurance contracts sold by HSBC relate, in the

main, to core underlying banking activities, such as

savings and investment products, and credit life

products. The Group’s manufacturing focuses on

personal lines, i.e. contracts written for individuals,

which tend to be of higher volume and lower

individual value than commercial lines. They thus

contribute to diversifying insurance risk.

Life and non-life business insurance risks are

controlled by high-level policies and procedures set

centrally, supplemented as appropriate with

measures which take account of specific local

market conditions and regulatory requirements. For

example, manufacturing entities are required to

obtain authorisation from Group Insurance Head

Office to write certain classes of business, with

restrictions applying to commercial and liability non-

life insurance, in particular.

Local ALCOs and Risk Management

Committees are required to monitor certain risk

exposures, mainly for life business where the focus

is on reviewing the risks associated with the duration

and cash flow matching of insurance assets and

liabilities.

Reinsurance is also used as a means of

mitigating exposure, in particular to aggregations of

catastrophe risk. Specific examples are as follows:

• Accident and health insurance. Potential

exposure to concentrations of claims arising

from isolated events, such as earthquakes or a

pandemic, are mitigated by the purchase of

catastrophe reinsurance.

• Motor insurance. Reinsurance protection is

arranged to avoid excessive exposure to larger

losses, particularly from personal injury claims.

• Fire and other damage to property. Portfolios at

risk from catastrophic losses are protected by

reinsurance in accordance with information

obtained from professional risk-modelling

organisations.

Although reinsurance provides a means of

managing insurance risk, such contracts expose the

Group to counterparty risk, the risk of default by the

reinsurer (see page 267).

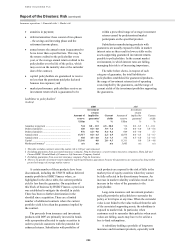

The following tables provide an analysis of

HSBC’s insurance risk exposures by geographical

region and by type of business. By definition, HSBC

is not exposed to insurance risk on investment