HSBC 2008 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

HSBC HOLDINGS PLC

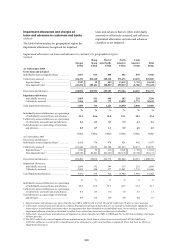

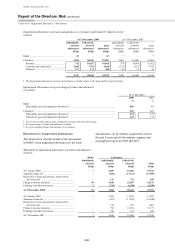

Report of the Directors: Risk (continued)

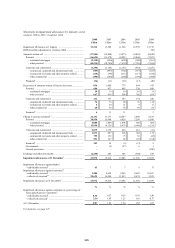

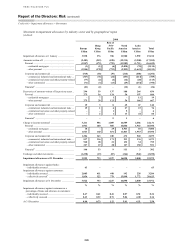

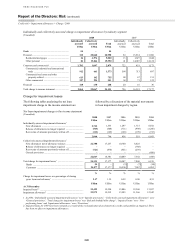

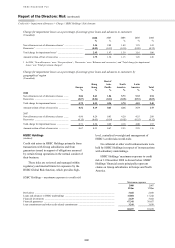

Credit risk > Impairment allowances > Charge > 2008 / 2007

230

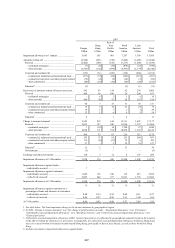

Impairment charges against banks rose in the UK

due to exposures to the Icelandic banks in 2008.

New loan impairment charges rose in Turkey as

delinquency rates rose across credit cards, personal

loans and corporate lending in light of the

deteriorating economic environment. Elsewhere,

impairment charges on the commercial portfolio rose

in the UK, particularly in the final quarter of 2008 as

the weakening property market led to higher

impairment charges against construction companies

and businesses dependent upon the real estate sector.

In France, the impact of declining commercial credit

quality more than offset lower balances. Impairment

allowances against firms in the financial sector rose

due to exposure to a single asset management firm in

the UK. Credit quality in the UK personal lending

portfolio remained broadly stable, reflecting the

strength of HSBC’s loan book in a period of

significant economic uncertainty. Mortgage lending

in the UK remained well secured as risk mitigation

actions taken since 2006 reduced risk exposure to

some of the problems now being uncovered in the

UK residential property market. Credit quality in the

unsecured portfolios of M&S Money, HSBC Bank

and Partnership Cards deteriorated slightly in 2008,

particularly in the second half of the year, due to the

weakening UK economy.

Releases and recoveries in Europe declined by

27 per cent, driven by the deterioration in economic

conditions.

In Hong Kong, new loan impairment charges

more than doubled from a low base, driven by

deterioration in credit quality in the commercial

portfolio in the second half of the year as the

economy and trade flows weakened. Residential

mortgage lending continued to be well-secured, as

regulatory restrictions constrained origination loan-

to-value ratios to below 70 per cent.

In Rest of Asia-Pacific, new loan impairment

charges rose by 59 per cent to US$1.3 billion,

primarily in India and the Middle East. Higher

impairment charges in India were driven by a

combination of rising delinquency rates in consumer

lending, as credit conditions deteriorated, and

increased lending. Increased charges in the Middle

East were due to rising delinquencies as growth rates

declined and the property market retreated as

economic conditions deteriorated on the back of

lower oil and gas prices.

New loan impairment charges in North America

rose by 37 per cent to US$16.8 billion, driven by the

continued deterioration in credit quality in the HSBC

Finance loan portfolio and, to a lesser extent, in

HSBC USA.

US credit quality showed significant

deterioration across the portfolio, driven by the

continued weakness of the US economy. The reasons

behind the deterioration in US credit quality, the

effects on the US personal lending portfolio and

actions taken as a result are discussed in more detail

on page 210. Partly offsetting the effect of the

deterioration was a reduction in overall lending as

HSBC continued to reduce its exposure in the US.

In US card and retail services, impairment

charges rose, driven by portfolio seasoning, higher

levels of personal bankruptcy filings and continued

weakness in the US economy. Delinquency

increased in the geographical regions most affected

by house price falls and rising unemployment.

In Commercial Banking, impairment charges

rose from a low base driven by deterioration in the

commercial real estate loan book in the US, and

higher impairment charges against firms in the

manufacturing, export and commercial real estate

sectors in Canada. Higher impairment charges in

Global Banking and Markets reflected weaker credit

fundamentals in the US in 2008. Impairment

allowances against firms in the financial sector rose

due to rising delinquencies, despite government

intervention.

Releases and recoveries in North America rose

by 55 per cent to US$180 million.

In Latin America, new loan impairment

charges rose by 37 per cent to US$2.8 billion. The

most significant increase was in Mexico, reflecting

higher impairment charges in the credit card

portfolio due to a combination of higher average

balances from organic expansion and growing

delinquency rates driven by a deterioration in credit

quality as the 2006 and 2007 vintages continued to

season and move into later stages of delinquency.

Management action to improve the quality of new

business included tightened underwriting, enhanced

collection strategies and better managed customer

acquisition channels. The commercial portfolio in

Mexico also experienced higher impairment charges

due to credit quality deterioration among small and

medium sized enterprises as the economy weakened.

In Brazil, higher impairment charges were driven by

a combination of balance growth and credit quality

deterioration in the vehicle finance and payroll loan

portfolios.

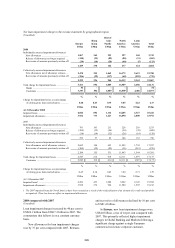

2007 compared with 2006

(Unaudited)

Loan impairment charges rose by 63 per cent to

US$17.2 billion from US$10.5 billion in 2006. The