HSBC 2008 Annual Report Download - page 223

Download and view the complete annual report

Please find page 223 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

221

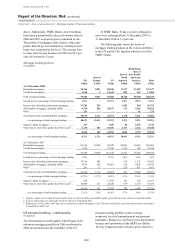

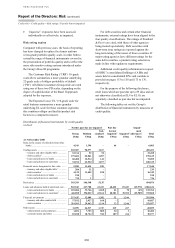

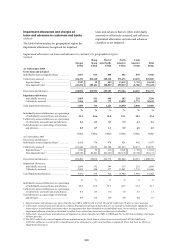

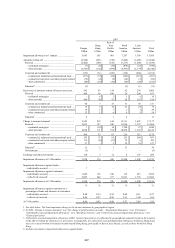

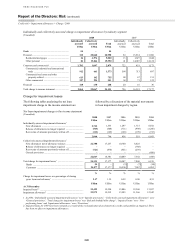

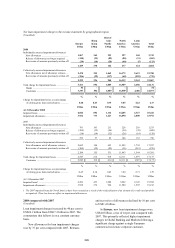

2008 compared with 2007

(Unaudited)

Total impaired loans to customers were

US$25.4 billion at 31 December 2008, an increase

of 29 per cent since the end of 2007 (42 per cent at

constant currency). Impaired loans were 3 per cent

of gross customer loans and advances, a rise from

2 per cent at 31 December 2007.

The commentary that follows compares

balances at 31 December 2008 with those at

31 December 2007, at constant exchange rates.

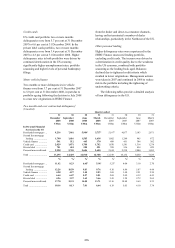

In Europe, impaired loans at US$6.8 billion

were 32 per cent higher than at the end of 2007. The

increase was driven by the UK where credit quality

in the UK commercial portfolio deteriorated sharply

in the final quarter of the year. A small number of

exposures in the commercial real estate sector were

particularly affected by a sharp deterioration in

market conditions in the fourth quarter. UK

mortgage impairments remained broadly stable

despite the substantial increase in balances in the

second half of the year and delinquency levels

increased modestly from a low base. Unsecured

personal lending in the UK also saw a slight increase

in the levels of impaired loans, particularly in the

second half of the year, as the economy weakened.

A single financial sector loan in Europe also affected

results. Impairment levels in France remained low in

the personal sector. However, Commercial Banking

experienced a rising number of small impairments

during the second half of the year and a small

number of larger impairments in the last quarter. In

Turkey, impaired loans rose by 81 per cent due to

increased delinquency in the personal lending

portfolio and, particularly, in credit cards.

In Hong Kong, impaired loans increased from a

previously low level to US$852 million. The

deterioration was concentrated in the commercial

lending portfolio and was attributable to a number of

factors including exporters in Hong Kong being

affected by reduced demand from the US and other

developed countries. The sharp fall in the value of

currencies and commodities left some customers’

balance sheets weakened, coupled with rising fraud

encountered with certain counterparties.

In the Rest of Asia-Pacific impaired loans

increased by 8 per cent to US$1.1 billion, primarily

due to the deterioration in the commercial lending

portfolio. In the last quarter of 2008 the number of

export orders suffered a sharp fall and, together with

a deterioration in credit quality around the region,

caused a rise in impaired loans. Noticeable increases

were recognised in Taiwan, Indonesia and India. In

Taiwan the commercial loan portfolio started to

deteriorate in the second half of the year as the fall

in exports started to affect local businesses. In

Indonesia and India, the increase in impaired loans

was a result of the downgrade of a few individual

customers as economic conditions worsened.

Impaired personal loans rose as increased

unemployment and bankruptcy rates affected the

ability of customers to repay. India continued to

show significant impaired loans as the economic

conditions deteriorated and credit quality weakened.

Active measures are being taken to reduce exposure

in India and manage the personal lending portfolio.

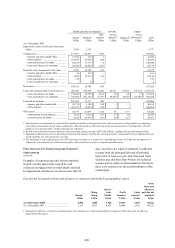

In North America, impaired loans rose

significantly, increasing by 49 per cent to

US$14.3 billion at 31 December 2008. The US

consumer finance business experienced a broad

based deterioration in credit quality due to higher

unemployment as the economy slowed. A full

discussion of these developments and their effect

on credit quality is provided in the ‘Areas of special

interest’ commentary on page 208. In Canada,

impaired loans rose from a low base as credit

conditions weakened, with the loss concentrated

in a single exposure in the commercial real estate

portfolio. In the US, commercial and corporate credit

quality declined due to downgrades as the economic

environment deteriorated.

In Latin America, impaired loans increased

by 37 per cent to US$2.3 billion. Impaired loans in

Mexico rose by 32 per cent, largely in credit cards

driven by portfolio growth in personal lending,

seasoning and higher delinquency rates. In Brazil,

impaired loans rose by 34 per cent due to growth in

personal lending due to deterioration in payroll and

vehicle finance loan portfolios, and weakness in a

number of real estate portfolios and corporates

exposed to the sharp rise in the value of the US

dollar in the second half of the year.