HSBC 2008 Annual Report Download - page 273

Download and view the complete annual report

Please find page 273 of the 2008 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

|

|

271

Liquidity risk

(Audited)

It is an inherent characteristic of almost all insurance

contracts that there is uncertainty over the amount of

claims liabilities that may arise, and the timing of

their settlement and this leads to liquidity risk.

To fund the cash outflows arising from claims

liabilities, HSBC’s insurance manufacturing

subsidiaries primarily utilise liquidity from the

following sources:

• cash inflows arising from premiums from new

business, policy renewals and recurring

premium products;

• cash inflows arising from interest and dividends

on investments and principal repayments of

maturing debt investments;

• cash resources; and

• cash inflows from the sale of investments.

HSBC’s insurance manufacturing subsidiaries

manage liquidity risk by utilising some or all of the

following techniques:

• matching cash inflows with expected cash

outflows using specific cash flow projections or

more general asset and liability matching

techniques such as duration matching;

• maintaining sufficient cash resources;

• investing in good credit-quality investments

with deep and liquid markets to the degree to

which they exist;

• monitoring investment concentrations and

restricting them where appropriate, for example,

by debt issues or issuers; and

• establishing committed contingency borrowing

facilities.

Every quarter, HSBC’s insurance manufacturing

subsidiaries are required to complete and submit

liquidity risk reports to Group Insurance Head Office

for collation and review by the Group Insurance

Market and Liquidity Risk Meeting. Liquidity risk is

assessed in these reports by measuring changes in

expected cumulative net cash flows under a series of

stress scenarios designed to determine the effect of

reducing expected available liquidity and

accelerating cash outflows. This is achieved by, for

example, assuming new business or renewals are

lower, and surrenders or lapses are greater, than

expected.

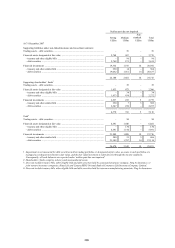

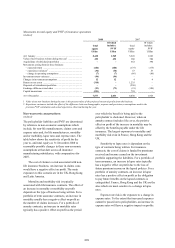

The following tables show the expected

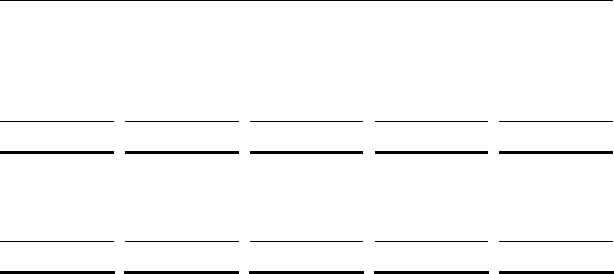

undiscounted cash flows for insurance contract

liabilities and the remaining contractual maturity of

investment contract liabilities at 31 December 2008.

As indicated in the analyses of life and non-life

insurance risks on pages 257 to 258, a significant

proportion of the Group’s non-life insurance

business is viewed as short term, with the settlement

of liabilities expected to occur within one year of the

period of risk. There is a greater spread of expected

maturities for the life business where, in a large

proportion of cases, the liquidity risk is borne in

conjunction with policyholders (wholly in the case

of unit-linked business).

The profile of the expected maturity of the

insurance contracts as at 31 December 2008

remained comparable with 2007.

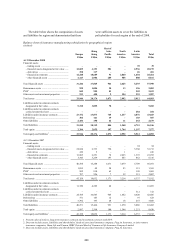

Expected maturity of insurance contract liabilities

(Audited)

Expected cash flows (undiscounted)

Within 1 year 1-5 years 5-15 years Over 15 years Total

US$m US$m US$m US$m US$m

At 31 December 2008

Non-life insurance .................................... 1,178 1,186 115 1 2,480

Life insurance (non-linked) ...................... 2,527 7,789 16,695 14,432 41,443

Life insurance (linked) ............................. 1,295 1,251 3,269 5,390 11,205

Total1 ......................................................... 5,000 10,226 20,079 19,823 55,128

At 31 December 2007

Non-life insurance .................................... 1,337 1,352 164 1 2,854

Life insurance (non-linked) ...................... 1,887 5,310 15,986 13,269 36,452

Life insurance (linked) ............................. 507 1,894 3,644 5,014 11,059

Total2 ......................................................... 3,731 8,556 19,794 18,284 50,365

1 Does not include insurance contracts issued by associated insurance company, Ping An Insurance, or joint venture insurance

companies, Hana Life and Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited.

2 Does not include insurance contracts issued by insurance manufacturing associate, Ping An Insurance.